Most notably, however, following outturns of 13.3k in September and -24.8k in October, employment growth has shifted down a gear as the annual pace was unchanged at around 2.0% in November compared to a pace of a little above 2.2% through Q1 and Q2 and then 2.5% in Q3 (see chart of the week, below). While employment growth at 2.0% is still robust relative to growth in the workforce of around 1.6% in annual terms, this dynamic has become less constructive for an RBA Board that is intent on lowering spare capacity, particularly so given the Bank anticipates GDP growth to remain below trend through the first half of 2020.

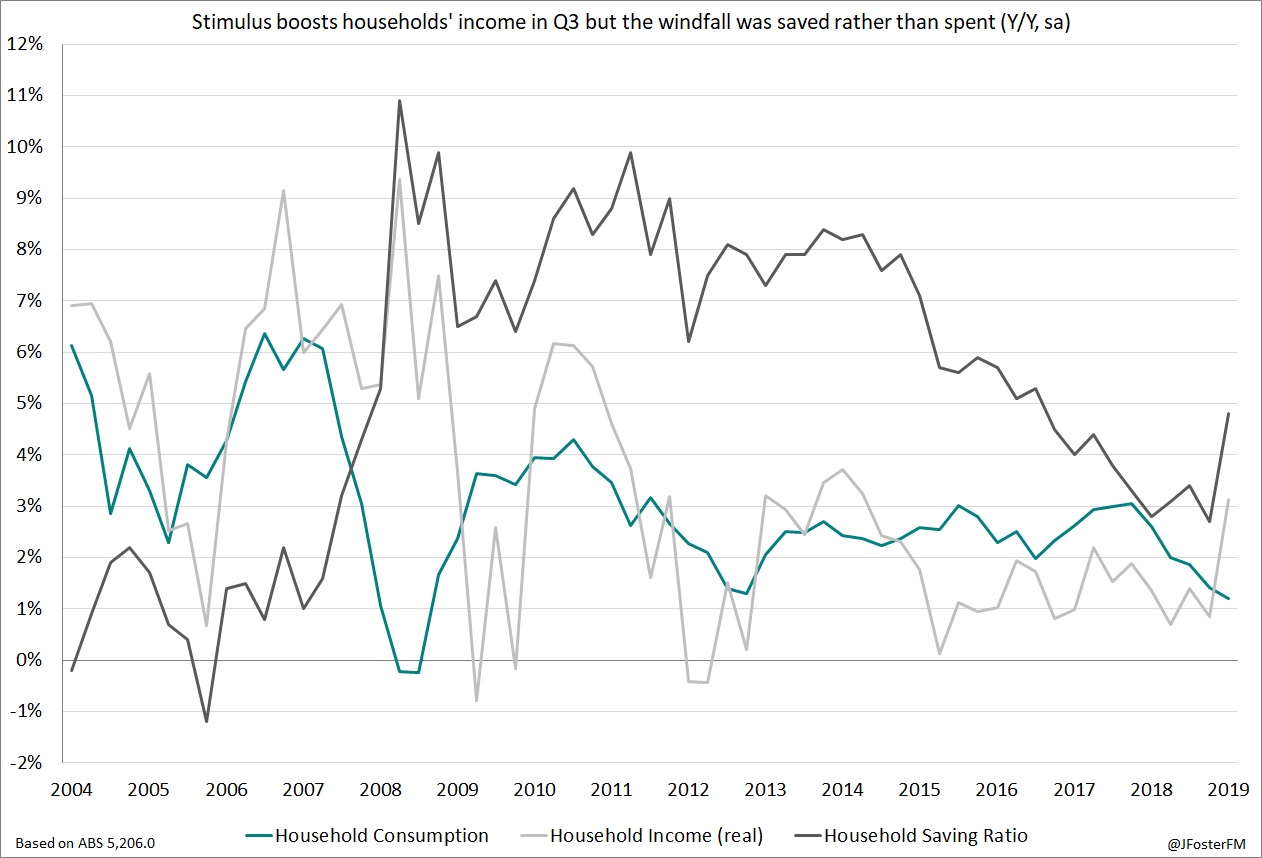

Chart of the week

The minutes from the RBA's policy meeting held earlier this month, released this week, reiterated that the Board is in wait-and-see mode, continuing to assess the impact from its 3 earlier rate cuts in 2019, but noted it "had the ability to provide further stimulus to the economy, if required". The Board remains constructive on the stimulatory impulse that will flow from an improving established housing market and this week's housing finance update for October was consistent with that theme as commitments increased by 2.0% in the month to continue the recent uptrend (more details here).

Throughout 2019, the Bank has been public in calling on fiscal authorities to contribute to a more balanced policy response to counter soft domestic demand conditions, which made this week's Mid-Year Economic and Fiscal Outlook (MYEFO) from the Federal government of key interest. Federal Treasurer Josh Frydenberg presented a downgraded update to April's Budget, with the forecast surplus for 2019/20 lowered from $7.1bn to $5.0bn. As a result of weaker-than-anticipated economic conditions and the expectation for commodity prices to retrace from elevated levels, the budget position was downgraded by a total of $21.5bn over the 4 years out to 2022/23, lowering the projected aggregate surplus from $45.0bn to $23.5bn (more analysis here). Fiscal stimulus was modest, with a net $8.1bn in new spending to come through over the next 4 years, headlined by the previously announced accelerated roll-out of infrastructure projects, drought assistance measures, and aged care services. Overall, the downgraded outlook together with the government's approach of returning the budget to surplus indicates that stimulus will remain weighted towards responses from the monetary side, with further RBA rate cuts likely in 2020.

— — —

Turning to the developments offshore, while the impeachment of US President Trump by Congress gained headlines worldwide and is a historically rare event occurring only twice previously, it had no impact on markets given it is highly unlikely to gain enough support in the Senate where the Republicans hold a comfortable majority. However, US political developments shape as key to market sentiment in 2020 in the lead up to November's presidential election (see our outlook section). Data out late in the week confirmed the US economy expanded at a 2.1% annualised pace in the September quarter, with the household sector continuing to drive activity supported by a strong labour market and positive sentiment. However, the US economy has slowed noticeably over the past year with trade tensions and weakness offshore combining to weigh on net exports, business investment and inventories. The slowdown appears to have further to run, with Markit's 'flash' reading of its composite Purchasing Managers' Index (PMI) coming in at a reading of 52.2 in December, indicating that the growth pulse had softened to an annualised pace of around 1.5% in the current quarter. Activity in the services sector firmed to a 5-month high at a reading of 52.2 boosted by a stronger order book and employment but remains moderate overall. Meanwhile, conditions in the manufacturing sector remained broadly unchanged at 52.5 (prior: 52.6), though this is in contrast to the more closely followed ISM survey conveying a sector in contraction driven by weakness in new orders and external demand.

Over in Europe, Markit's PMI readings continued to paint a bleak assessment of conditions in the bloc. The composite index was steady in December at 50.6, indicating that the euro area economy had essentially stalled in Q4 and was around its weakest in 6 years. While activity in the services sector firmed in the month, this was offset by renewed weakness in a manufacturing sector that is currently in its deepest downturn in 7 years, buffeted by headwinds from trade and geopolitical uncertainty and weakness in the global economy. Also of interest in Europe this week, Sweden's central bank, the Riksbank, announced an increase to its benchmark interest rate from -0.25% to 0.0%, exiting from a 5-year period of negative rates. In the UK, despite the result in last week's general election, it became clear a hard Brexit scenario can not be completely ruled out, with PM Johnson to pursue legislation to prevent any extension to withdrawal from the EU past December 2020. With Brexit-related uncertainty set to persist, the Bank of England's (BoE) Monetary Policy Committee voted on Thursday to maintain its existing settings in a 7-2 decision, with members Haskel and Saunders again the dissenting voices. The BoE also announced Andrew Bailey, the current chief executive of the UK's Financial Conduct Authority, as its new governor taking over from incumbent Mark Carney at the completion of his term in mid-March next year.

Closer to home, key data from China this week was generally constructive as industrial production outperformed expectations rising by 6.2% through the year to November, while retail sales (8.0%Y/Y) and fixed asset investment (5.2%ytd) were in line with consensus. Meanwhile, the Bank of Japan's Policy Board left its monetary policy stance unchanged at its meeting this week but continues to note that if downside risks in the global economy were to materialise it "will not hesitate to take additional easing measures".

Over in Europe, Markit's PMI readings continued to paint a bleak assessment of conditions in the bloc. The composite index was steady in December at 50.6, indicating that the euro area economy had essentially stalled in Q4 and was around its weakest in 6 years. While activity in the services sector firmed in the month, this was offset by renewed weakness in a manufacturing sector that is currently in its deepest downturn in 7 years, buffeted by headwinds from trade and geopolitical uncertainty and weakness in the global economy. Also of interest in Europe this week, Sweden's central bank, the Riksbank, announced an increase to its benchmark interest rate from -0.25% to 0.0%, exiting from a 5-year period of negative rates. In the UK, despite the result in last week's general election, it became clear a hard Brexit scenario can not be completely ruled out, with PM Johnson to pursue legislation to prevent any extension to withdrawal from the EU past December 2020. With Brexit-related uncertainty set to persist, the Bank of England's (BoE) Monetary Policy Committee voted on Thursday to maintain its existing settings in a 7-2 decision, with members Haskel and Saunders again the dissenting voices. The BoE also announced Andrew Bailey, the current chief executive of the UK's Financial Conduct Authority, as its new governor taking over from incumbent Mark Carney at the completion of his term in mid-March next year.

Closer to home, key data from China this week was generally constructive as industrial production outperformed expectations rising by 6.2% through the year to November, while retail sales (8.0%Y/Y) and fixed asset investment (5.2%ytd) were in line with consensus. Meanwhile, the Bank of Japan's Policy Board left its monetary policy stance unchanged at its meeting this week but continues to note that if downside risks in the global economy were to materialise it "will not hesitate to take additional easing measures".

— — —

The 2020 outlook: Uncertainty an enduring headwind

As year-end approaches, the familiar theme of uncertainty appears set to remain present through 2020, and with growth in the advanced economies languishing around or below potential, central banks are likely to remain prominent. In response to a synchronised global growth slowdown driven by trade and geopolitical uncertainty and more medium-term structural factors, central banks pivoted proactively to more accommodative policy stances from mid-year. However, before this tide of easing gains traction, the growth slowdown is likely to extend into 2020 given that the interest rate sensitive manufacturing sector has only recently shown signs of stabilising at weak levels.

Risks to an eventual stabilisation of growth in the advanced economies appear to remain tilted to the downside as uncertainty is likely to persist around US-China trade negotiations and the nature of the UK's withdrawal from the EU, while the US presidential election has the potential to weaken firms' investment plans further and slow employment growth that would, in turn, threaten currently robust consumer spending. Meanwhile, China's economy will continue to adjust to a slower and more sustainable pace of growth. Given these dynamics and in the event that fiscal responses remain limited, central banks will likely be left in the position of having to test the limits of conventional monetary policy in 2020.

In the US, the Federal Reserve still has ample conventional policy space, but in Europe any further easing to the ECB's already ultra-easy settings would likely be seen as having only a marginal impact and would probably be resisted by the Governing Council in any case, particularly with new President Christine Lagarde overseeing a complete review of the Bank's monetary policy strategy. In Australia, the RBA has signaled that its effective lower bound is 50bps away, at which point efforts will turn to the unconventional through quantitative easing, if required.

With this, my final piece for the year, I thank everyone for reading in 2019 and wish you all the best for Christmas and in the new year.

As year-end approaches, the familiar theme of uncertainty appears set to remain present through 2020, and with growth in the advanced economies languishing around or below potential, central banks are likely to remain prominent. In response to a synchronised global growth slowdown driven by trade and geopolitical uncertainty and more medium-term structural factors, central banks pivoted proactively to more accommodative policy stances from mid-year. However, before this tide of easing gains traction, the growth slowdown is likely to extend into 2020 given that the interest rate sensitive manufacturing sector has only recently shown signs of stabilising at weak levels.

Risks to an eventual stabilisation of growth in the advanced economies appear to remain tilted to the downside as uncertainty is likely to persist around US-China trade negotiations and the nature of the UK's withdrawal from the EU, while the US presidential election has the potential to weaken firms' investment plans further and slow employment growth that would, in turn, threaten currently robust consumer spending. Meanwhile, China's economy will continue to adjust to a slower and more sustainable pace of growth. Given these dynamics and in the event that fiscal responses remain limited, central banks will likely be left in the position of having to test the limits of conventional monetary policy in 2020.

In the US, the Federal Reserve still has ample conventional policy space, but in Europe any further easing to the ECB's already ultra-easy settings would likely be seen as having only a marginal impact and would probably be resisted by the Governing Council in any case, particularly with new President Christine Lagarde overseeing a complete review of the Bank's monetary policy strategy. In Australia, the RBA has signaled that its effective lower bound is 50bps away, at which point efforts will turn to the unconventional through quantitative easing, if required.

— — —

With this, my final piece for the year, I thank everyone for reading in 2019 and wish you all the best for Christmas and in the new year.