In the US this week, the 2nd estimate of GDP growth in Q2 was revised down from 2.1% to 2.0% annualised, as expected. Once again, it highlighted the strength of the US consumer, with personal spending revised up from an already rapid pace of 4.3% to 4.7% annualised. A robust labour market has been key to this, as has resilient sentiment despite rising trade tensions and increased gyrations in equity markets. However, there were signs that sentiment may be beginning to fray with the University of Michigan's consumer sentiment index falling by its most in 6½ years to a reading of 89.8 -- its lowest since October 2016. One in three consumers cited concerns around the impact of tariffs, notably on the $300bn tranche of consumer-related products originating from China due to start September 1. Weaker sentiment has the potential to slow consumer spending, which would be problematic from the US economic outlook given that business investment contracted in Q2 and is at risk of a further slowdown, while net exports were also weighed by uncertainty over trade policy.

Political developments were the main focus in Europe this week. The recent collapse of Italy's government appears to set to reach a quick resolution after President Mattarella asked Giuseppe Conte, leader of the 5-Star movement, to form a coalition with the opposition Democratic Party. This development relegates Matteo Salvini's League party from office, despite polls indicating it is the most popular with voters in Italy. Markets interpreted the news favourably on the basis that it improves the prospects of a more fiscally prudent government as well as limiting potential conflict with the EU. Over in the UK, the prospect of a no-deal Brexit increased after PM Boris Johnson's request to the Queen to prorogue parliament was granted. As such, parliament will now be suspended between September 12 and October 14. Parliament is due to return on September 3, which leaves a little over a week before the suspension starts for the 'Remainers' to gather support. The suspension finishes just before the EU Summit on October 17, with the withdrawal date then occurring on October 31.

—

The weakness in Q2 was predominantly driven by a 5.5% decline in private sector residential activity -- its weakest quarter in 8 years -- as the downturn in the construction cycle gathered pace to an annual contraction of -9.5% (shown as chart of the week, below). The weakness was broad based in Q2, with new residential construction falling by 5.3% to -9.9% over the year, and alterations down by 3.3% to -5.8% on a year earlier. Given that dwelling approvals data on Friday showed renewed weakness with a 9.7% fall in July to be -28.5% over the year (see our review here), residential construction is likely to remain a headwind for the domestic economy well into next year. Non-residential activity also fell by a notable 6.6% in Q2 as the annual pace swung from 4.6% to -3.3%. Engineering work also fell by 1.1% in the quarter to be down by 15.9% through the year, which reflects the wind-down from the completion of major projects in the resources sector and slower growth in public infrastructure work.

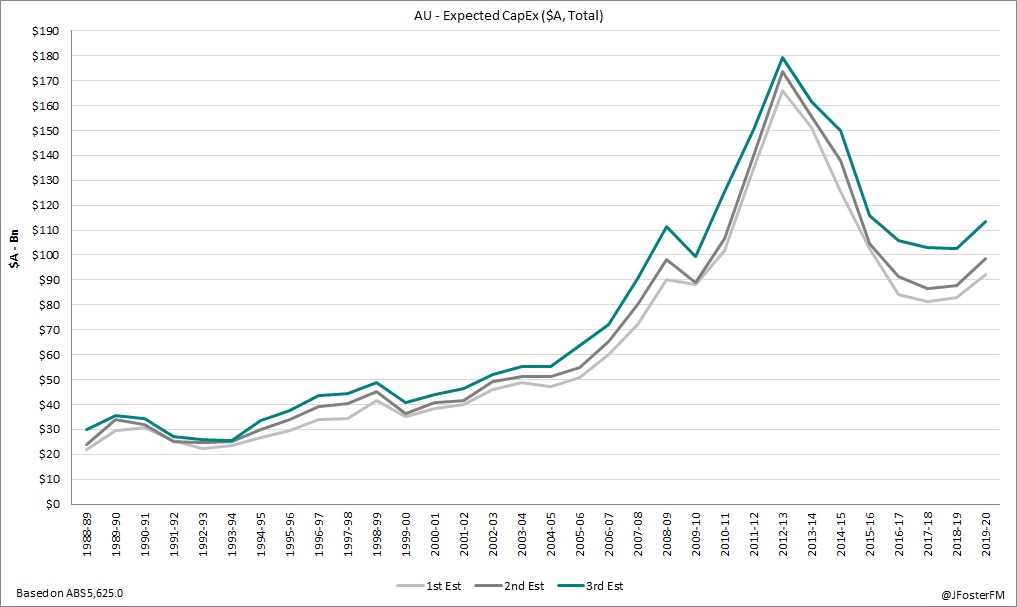

Chart of the week

GDP growth in the June quarter National Accounts is expected to print at 0.5% in Q2 next Wednesday, with the annual pace slowing to 1.4% from 1.8%. As outlined in our preview (see here), the key dynamics are a weaker global economy and slowing domestic demand conditions, driven by soft growth in household consumption and weakness in residential construction, with subdued business investment and a rebound in resource exports. The other main highlight next week is the Reserve Bank of Australia's September policy meeting, in which the Board is expected to remain on hold at 1.0%. August's meeting minutes highlighted an increased focus on developments in the global economy given escalating trade tensions and geopolitical uncertainties, with the Bank's commentary here likely to be instructive to its policy outlook.