CapEx — Q2 | By the numbers

- Capex spending in Q2 fell by 0.5% (-$156m) to $29.228bn, which was a sizeable disappointment on the median forecast for a 0.4% increase. The intially reported 1.7% decline in Q1 was revised to -1.3%. Over the year, capex spending declined by 1.0% compared to -1.7% in Q1.

- Equipment, plant and machinery investment increased by 2.5% in the quarter (prior rev: -0.5%q/q), or by $351m to $14.16bn. As a result, the annual pace accelerated to 5.7% from 1.9%.

- Investment in building and structures declined by 3.3%q/q (prior rev -1.9% from -2.8%), or by -$508m to $15.068bn, which further increased the annual decline from -4.7% to -6.6%.

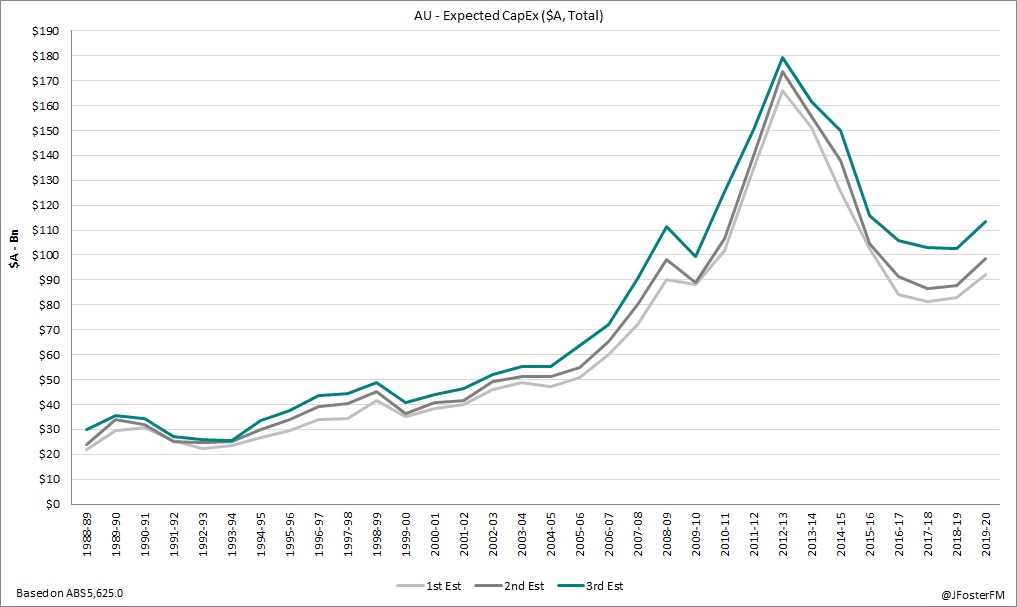

- Estimate 3 for capex in the 2019/20 financial year was nominated at $113.4bn, which was a touch higher than the median forecast for $113.0bn. This was an upgrade of 14.9% on estimate 2 for 2019/20 and a 10.7% increase on estimate 3 from the previous financial year.

- Total capex spending in 2018/19 according to estimate 7 was $122.119bn -- a slight decrease of 0.1% on estimate 6.

CapEx — Q2 | The details

Total capex spending fell by 0.5% (-$156m) in the quarter to be down by 1.0% over the year. Looking into the details, the weakness was attributable to the non-mining sector, which in aggregate fell by 1.3% (-$287m) to $21.206bn, though it is still positive through the year at 1.4%. In particular, the decline was driven by a 2.4% contraction (-$472m) from 'other selected industries' (mainly services) in the quarter to $18.845bn, with the annual pace decelerating from 4.2% to 1.6%. The decline in Q2 was driven by buildings and structures at -5.1%, though equipment investment lifted by 1.5%. The manufacturing sector saw capex rising by 8.5% in Q2 (+$185m) to $2.361bn to be broadly flat over the year (-0.4%). Q2's increase was driven by broad-based gains from buildings and structures (+17.5%q/q) and equipment (+7.0%q/q).

In the mining sector, capex posted its strongest quarterly outturn in 5 years at +1.7% (+$131m) to $8.022bn, with the annual decline slowing sharply from -12.2% to -6.8%. However, buildings and structures were still a drag -- albeit very modest -- at -0.4%, with equipment spending up by 10.0%.

Capex spending in Q2 was led by New Wales (+4.2%q/q, +8.7%Y/Y) and Western Australia (+4.8%q/q, -6.1%Y/Y), the latter posting its strongest quarterly rise in 6 years, and the Northern Territory (+10.0%q/q, -55.7%Y/Y), which, together with the asset and sector data, suggests the drag from completing resources projects may now be in the past. However, those gains were surpassed by declines from Victoria (-2.7%q/q, +11.9%Y/Y), Queensland (-5.9%q/q, -9.8%Y/Y), South Australia (-3.7%q/q, -2.9%Y/Y) and Tasmania (-9.8%q/q, -5.4%Y/Y).

Investment intentions by firms for the full 2019/20 financial year as per the 3rd estimate was nominated at $133.4bn, with markets anticipating a figure of $113.0bn. This implies that capex intentions are 10.7% above the level they were from a year ago, and have also increased by 14.9% compared to 3 months ago.

While appearing upbeat, the 10.7% year-to-year rise is less constructive than the 12.3% year-to-year increase implied by estimate 2 for 2019/20. In addition, the 14.9% rise from estimate 2 is only slightly stronger than the average rate of increase between estimates 2 and 3 over the past 5 years.

The implied 10.7% year-to-year increase in capex in 2019/20 is expected to be broad based, with mining investment intentions pointing to a rise of 20.7% to $38.08bn. Non-mining investment intentions are pointing to a 6.2% rise to $75.322bn, with services industries up by 5.8% to $65.987bn and manufacturing lifting by 8.6% to $9.335bn.

CapEx — Q2 | Insights

The fall in capex in Q2 was driven by weakness in buildings and structures, which is consistent with yesterday's weak Construction Work Done update. The details for equipment spending were more upbeat at +2.5% in the quarter, and this component will help to offset some of the weakness from the construction activity. Overall, it looks to have been another patchy quarter for business investment, likely making only a subdued contribution to GDP growth in Q2.

Investment plans for 2019/20 appear slighly less constructive than they were 3 months ago, likely weighed by increased uncertainty in global and domestic economic conditions, which is despite the passage of the federal election and the Reserve Bank of Australia twice cutting the cash rate in June and July. Notwithstanding, investment in the mining sector remains on track to end 6 consecutive years of decline in 2019/20, while the outlook for non-mining investment is still positive. Both of these factors are supporting the growth outlook over the medium term.