It was a quieter week for markets due to holidays across Asia and a relatively limited data flow. Markets also are firmly focused on the week ahead, where the docket includes policy meetings from the Federal Reserve, European Central Bank and the Bank of England and many key data points. In Australia, markets moved to price in more RBA tightening as the latest inflation data came in above expectations; the local currency also supported by upbeat US equity sentiment.

US data consistent with a slowing economy

Further signs of the slowing in the US economy came to hand this week, leaving intact the markets' view that Fed rate cuts later on in the year remain in prospect. December quarter GDP growth was stronger than expected expanding by 0.7% quarter-on-quarter, though that outcome was boosted by net trade and inventories. Underlying domestic demand was a soft 0.2%q/q, while January's flash PMI reading at 46.6 indicated activity was slowing. Data on personal consumption showed that momentum in household spending has softened. Both nominal (-0.2%m/m) and real (-0.3%m/m) consumption growth declined for the second month running. The saving rate has risen over the past couple of months from 2.5% to 3.4% in December, suggesting households were moderating their spending into year-end. However, spending still remains well above pre-pandemic levels, supported by a strong labour market in which weekly jobless claims fell to their lowest level since April last year.

The Fed has achieved progress on the inflation front going into next week's meeting. In December, its preferred core PCE deflator gauge slowed from 4.7% to 4.4%yr, a pace below the 4.8% projected by the FOMC. The momentum in underlying inflation pressures eased notably over the final quarter of the year. The 3-month annualised pace in the core PCE deflator was 2.9% in December, its slowest pace since January 2021 and down from 4.5% at the end of the previous quarter.

Australian inflation rises to new 30-year highs

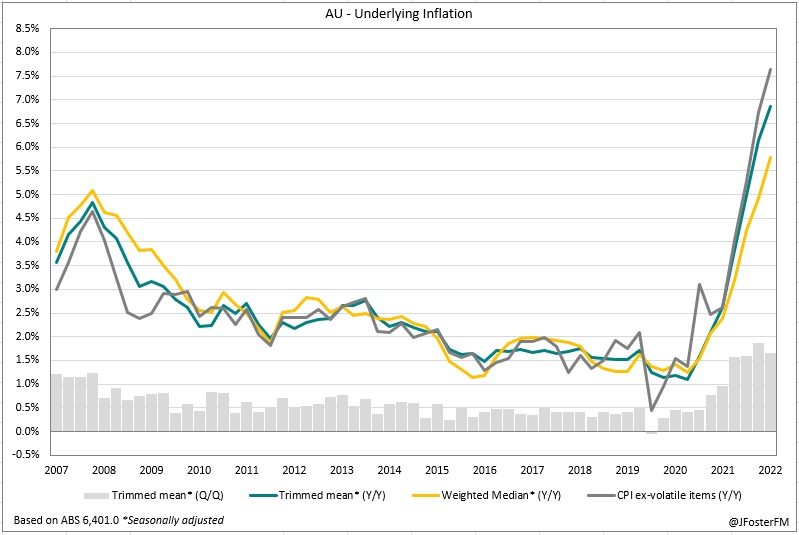

An elevation in both headline (7.8%Y/Y) and core inflation (6.9%Y/Y) to new 30-year highs saw markets moving to price in the continuation of the RBA's rate hiking cycle at the February meeting. These outcomes were close to RBA forecasts (8% headline and 6.5% trimmed mean) but above market expectations on the day. Despite easing pressures in home building costs and grocery prices, headline inflation was 1.9% in the December quarter (up from 1.8% in Q3) as travel costs surged during the peak summer holiday period (10.9%), and electricity prices spiked (8.6%) as government rebates faded (my full Q4 CPI review is available here).

This looks likely to be the peak for inflation in Australia. The 3-month and 6-month annualised rates at 7.7% and 7.6% respectively are around the year-ended CPI rate (7.8%), while price pressures coming through the pipeline for producers (0.7%) and from imports (4.3%) moderated to their slowest quarterly increases in more than a year. That is also consistent with the signals from the December NAB Business Survey, with growth in firms' input and selling prices all slowing.

Looking ahead to the next RBA meeting, the inflation forecasts are due to be refreshed and this will ultimately be key for the hiking cycle. Currently, the RBA forecasts headline inflation to slow to 4.7% by the end of the year (3.8% core) and then to 3.2% in 2024. Broadly speaking, the main driver of inflation is switching from goods to services, similar to many other comparable economies. Throughout this year, the disinflationary pulse from goods will increase, though prices in the service sector are still on the rise. The balance of those competing forces will largely shape the path back to 2-3% inflation.

Growth pulse improving in Europe

The reappraisal of recession calls for the euro area has been somewhat validated by January's flash reading of the PMI gauge returning to growth territory. The composite PMI lifted from 49.3 to 50.2, a 7-month high, on the back of rising services (50.7) and manufacturing activity (48.8). Improving sentiment in the euro area has come as an energy crisis looks to have been avoided, with energy prices falling due to milder winter temperatures, while China's more accelerated exit from its Covid zero has also helped. Next week sees the ECB returning for its first policy meeting of the year where the Governing Council is expected to hike its key rates by 50bps.

Source: S&P Global

Bank of Canada to hit the pause button

A 25bps rate hike from the Bank of Canada this week looks to be the last for its tightening cycle. With rates now at 4.5%, up 425bps since the start of last year, the BoC's guidance is that it "... expects to hold the policy rate at its current level" while it assesses the cumulative effects of monetary tightening on the economy. In the BoC's latest Monetary Policy Report, it was noted that while there is still an excess of demand, the early effects of its tightening cycle are showing in the housing market and on household spending. These headwinds are expected to lead to a stalling of growth by the middle of the year. Disinflationary pulses from falling energy prices and easing supply chain pressures are forecast to slow inflation from 6.7% to 3% in mid-2023, before returning to the 2% target in 2024.

Source: Bank of Canada