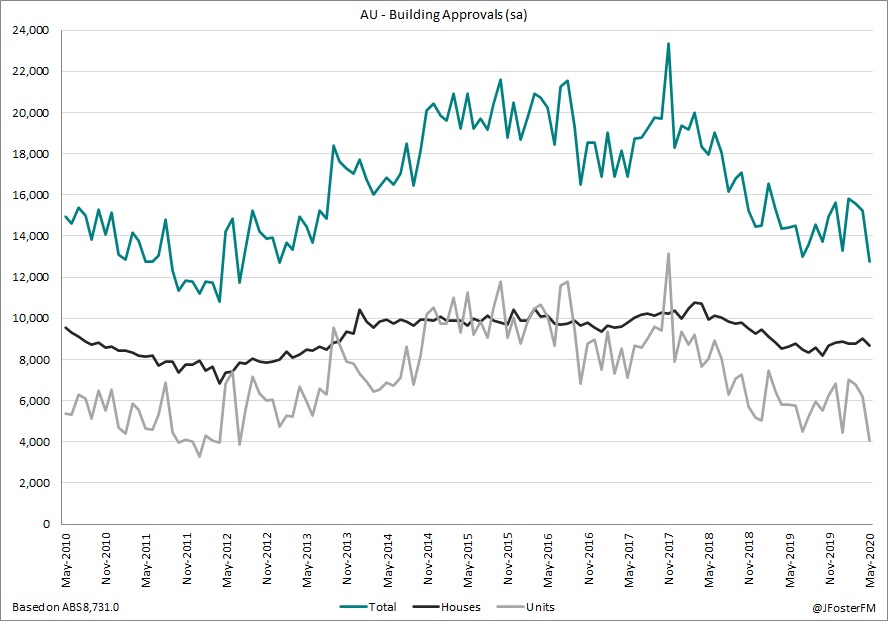

Building Approvals — May | By the numbers

- Dwelling approvals (including the private and public sectors) fell by 16.4% (vs median forecast of -7.8%) in May (seasonally adjusted) to 12,736 — its lowest monthly total since January 2013. In April, approvals contracted by 2.1% (revised from -1.8%).

- Approvals are down by 11.6% on a year ago compared to +6.1% as of April.

- Unit approvals plunged by 34.5% on the month to 4,065 to their lowest level since June 2012, swinging the annual pace to -29.9% from +6.8%.

- House approvals posted their worst result since last October falling by 4.1% to 8,670, which slowed the annual pace of growth to 0.6% from +5.6%.

Building Approvals — May | The details

May's 16.4% decline on dwelling approvals was its sharpest monthly fall since December 2017, while the level at 12,736 was its lowest outturn going back to January 2013. The median forecast was for a smaller fall of 7.8% in May, though it should be noted that approvals had significantly surprised in March (-1.6% vs -15.0% expected) and April (-2.1% vs -10.7% expected). All of this speaks to the complexities of trying to gain a handle on the timing and scale of impact on residential demand from the pandemic. As the ABS noted in today's release; "Due to the lag between changes in demand, and the submission and determination of a building approval, the May data likely reflects applications and levels of demand prior to the introduction of major restrictions".

The weakness in today's report was concentrated on unit approvals (34.5%mth), with the underlying detail pointing to a very sharp decline in the high-rise segment. However, it was also a notably weak outcome on house approvals (-4.1%) derailing the progress that segment had made so far in 2020.

In terms of alterations, the value of work approved to be made to existing residential properties flatlined in May at around $634m (-8.4%yr) after falling by 12.0% in the month prior. The value of non-residential work approved extended its weakness from the earlier months of 2020 falling by a further 7.1% to $3.32bn (-19.7%yr) to its lowest level since August 2018.

Broad-based weakness came through from all states in May. Approvals in New South Wales and Victoria have fallen to their levels from around Q3 of last year, with much of these declines being driven by falling unit approvals. Queensland has seen an acceleration in the decline of approvals recently. South Australia is the only state to have seen approvals advance over the past year, though both Western Australia and Tasmania were also up over the year until that was reversed by weak outcomes in May.

Building Approvals — May | Insights

The outlook for approvals is highly uncertain due to the impact of border closures on net overseas migration — a key driver of population growth and demand for housing. As the ABS pointed out, today's numbers are likely to have reflected submissions from before the introduction of social distancing restrictions, so approvals appear to be lagging what is occurring in the broader economy at the moment.

The outlook for approvals is highly uncertain due to the impact of border closures on net overseas migration — a key driver of population growth and demand for housing. As the ABS pointed out, today's numbers are likely to have reflected submissions from before the introduction of social distancing restrictions, so approvals appear to be lagging what is occurring in the broader economy at the moment.