Consumer Price Index — Q4 | By the numbers

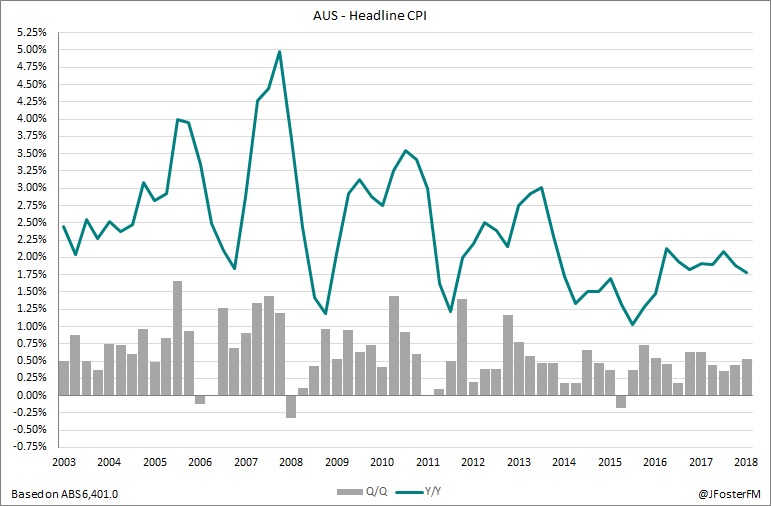

- Headline inflation was 0.5% in Q4, ahead of the market forecast for 0.4% and the first upside result in 2 years (prior: 0.4%).

- Annual headline inflation at 1.8% was also ahead of the median forecast for 1.7%, but down from the 1.9% pace in Q3.

- Core inflation (average of the trimmed mean and weighted median measures) was 0.4% in Q4, compared to the market forecast for 0.45% (prior rev 0.37% from 0.32%)

- Annual core inflation was 1.77%, in line with expectations for 1.75% (prior rev 1.8% from 1.75%)

Consumer Price Index — Q4 | The details

Looking across the categories, the quarterly and annual price changes are shown in the chart, below (click to expand). The alcohol and tobacco group saw a 3.2% rise in the quarter (6.8%Y/Y), with tobacco prices up by a sharp 9.4% in Q4, following a 12.5% increase in the federal excise tax.

Recreation and culture lifted by 1.1% (1.7%Y/Y) following a 6.2% increase in the cost of domestic holiday travel, which as the ABS highlighted coincided with the October school holiday period and the lead up to the peak season over summer.

Food and non-alcoholic beverages posted a 0.9% rise in Q4 (1.5%Y/Y), which incorporated seasonal impacts in fruit prices (+5%q/q), while meat prices (+1.6%q/q) lifted in response in drought conditions.

In the key housing category, the quarterly rise of 0.2% was another soft outcome (1.5%Y/Y). There were subdued increases for both rents (+0.2%) and new dwelling purchases by owner-occupiers (+0.4%).

The main drag on prices in Q4 was from a 0.7% fall from the transport group (2.8%Y/Y), which mostly reflected weaker global oil prices flowing through to petrol prices declining by 2.5% in the quarter.

Cyclical effects reducing out-of-pocket expenses for pharmaceuticals under the Federal government's Pharmaceutical Benefits Scheme saw the health group decline by 0.4% in the quarter (3.3%Y/Y).

Clothing and footwear eased by 0.2% (-0.7%Y/Y), which followed increases in the previous two quarters are a lengthy period of 6 consecutively quarterly declines. The intensity of retail competition and widespread discounting have been key factors in pricing weakness. This has also impacted furnishings and household equipment, though prices in these areas were firmer in Q4.

The contributions of the groups to the quarterly headline CPI result are shown in the chart, below.

Overall, inflation continues to be driven by areas in which prices are impacted by aspects of government policy such as alcohol and tobacco, utilities, health, education, and property rates. The chart, below, highlights that inflationary sources from the private sector as measured by market goods and services ex-volatile items continue to lag the broader CPI index. However, market-based sources jumped by 0.7% Q4 to 1.5%Y/Y — its fastest annual pace in 3 years — after being stuck at 1.1%Y/Y for the past 4 quarters.

Inflation also continues to be driven largely by domestic-based factors. Non-tradables lifted by 0.9% in Q4 (2.4%Y/Y) reflecting the increases in tobacco costs and in domestic holiday travel. Tradables — goods and services where prices are determined on global markets — fell by 0.3% in the quarter (0.6%Y/Y) following the weakness in petrol prices and also in audio, visual and computer equipment.

Consumer Price Index — Q4 | Insights

Today's data continued to show a soft inflationary pulse in the domestic economy and in that sense it was broadly consistent with the CPI reports from recent quarters. Inflation continues to be driven mostly by areas impacted by government policy, and in particular, tobacco remains a key driver. Sources of inflation remain subdued in housing and in clothing and footwear, though household goods have firmed as a possible response to a weaker Australian dollar. Household services have also been weakened by changes to child care subsidies. The RBA forecasts a gradual lift in inflation over the next couple of years in response to a tightening in the labour market and given that Q4's data was broadly in line with their expectations, next week's updated forecasts are not likely to be revised too significantly from an inflationary perspective.