The Australian National Accounts for the December quarter are due to be published by the ABS this morning (11:30am AEDT). Real GDP growth is expected to have been subdued at around 0.2% in the quarter, reflecting similar outcomes in other advanced economies. The RBA's assessment of excess demand in the economy is set to face a key test. Much of the focus is on the household sector amid the various crosscurrents to consumption, but other components of demand that have been providing offsetting strength look to have softened in the quarter.

A recap: Growth slowed further in Q3 as consumption stalled

The Australian economy slowed further in the September quarter as cost-of-living pressures and interest rate rises continued to weigh on household spending. Real GDP expanded by 0.2% in the quarter and 2.1% through the year, down sharply from a 5.8% pace a year earlier. Aside from real GDP slowing, the past year had also been characterised by weakness in per capita growth and productivity outcomes.

Household consumption growth stalled in the most recent quarter, effectively flatlining over the past year (0.4%). The post-pandemic rebound in spending had largely run its course by late 2022, leaving consumption increasingly exposed to high inflation, rising interest rates and an increased tax burden. Reflecting this, discretionary-related consumption weakened over the past year (-0.8%) as the consumption of essential goods and services - what households have to purchase - increased (1.2%). Meanwhile, the household saving ratio declined to 1.1%, its lowest since Q4 2007.

Higher interest rates and ongoing capacity pressures have driven weakness in residential construction activity (-0.3%Y/Y). By contrast, activity in the non-residential construction sector has risen at a solid pace, underpinning growth in business investment (8%Y/Y) and public demand (4.2%). Exports (6.8%Y/Y) have also supported growth, driven by the recovery in the tourism and education sectors.

A preview: Headwinds to growth persisted into year-end

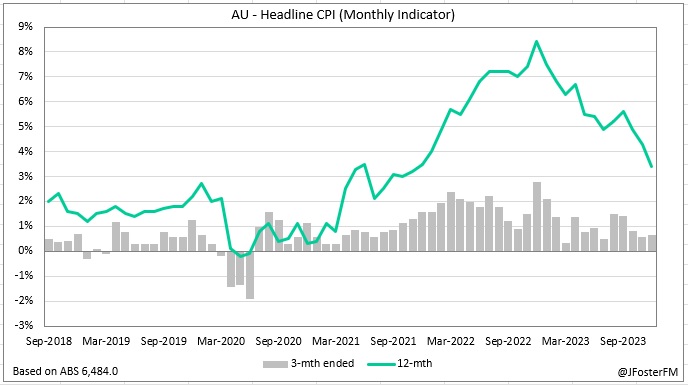

Outside of the US, growth in most advanced economies was modest in the final quarter of 2023, pointing to a similar outcome in Australia. Incoming data indicate that household consumption was subdued, while the resumption of the RBA's tightening cycle in November resulted in a decline in consumer sentiment readings. However, the dynamic around real household incomes improved as inflation declined sharply towards the end of the year.

Leading indicators point to subdued growth in household consumption in Q4. The seasonal rise in spending in the lead-up to Christmas may have been less pronounced than in recent years. Discretionary spending was partly boosted by Black Friday sales, an event of increasing prominence amongst Australian households.

A robust labour market continued to support household consumption. The earlier acceleration in wages growth followed by the subsequent fall in inflation saw real wages growth turning marginally positive in Q4. A slowing economy has, however, seen labour market conditions ease over the course of 2023. The unemployment rate averaged 3.8% over the back half of the year, rising from an average of 3.6% in the first half and up from the 3.4% cycle lows in late 2022. Hours worked declined by 0.7% in the December quarter, a sign of adjustment to softening demand conditions.

Capital city housing price gains have slowed over recent months but still lifted by 9-10% on a nationwide basis in 2023. Strong population growth and ongoing constraints limiting the completion of new homes have contributed to rising housing prices, despite the effects of the RBA's hiking cycle.

PropTrack chart

Summary of key dynamics in Q4

Household consumption — An improved dynamic around real incomes may have provided support to households. Retail sales volumes lifted by 0.3%, a modest rise but its strongest increase since mid-2022 nonetheless.

Dwelling investment — New home building and alterations activity weakened sharply in Q4. Higher interest rates and supply and labour constraints remain strong headwinds in the sector.

Business investment — Capital expenditure by private sector firms lifted modestly, led by buildings and structures investment. Equipment spending stabilised following a strong increase over the first half of the year.

Public demand — Increased by 0.5% in Q4, moderating from stronger growth in prior quarters. Public spending (0.6%) was the main driver as momentum in investment (0.1%) slowed.

Inventories — Expected to deduct 0.5ppt from quarterly growth. Mining inventory levels declined after shipments were disrupted in Q3, but this was moderated by an increase in public sector inventories.

Net exports — Will add 0.6ppt to Q4 growth, a reversal of Q3's negative contribution. Export volumes were soft falling 0.3%, though imports saw a much larger 3.4% decline.