Australia's National accounts for the June quarter are due to be published today at 11:30am (AEST). Growth in the Australian economy has slowed over the past year as the effects of falling real incomes and rising interest rates have weighed on household consumption. Expectations are for modest growth of around 0.4% in the June quarter.

A recap: Australian economic growth slowed sharply in the March quarter...

Real GDP slowed to 0.2% in the March quarter. Excluding quarters that were impacted by Covid lockdowns, this was the weakest quarterly growth rate since the December quarter of 2018. Year-ended growth eased to 2.3%, underpinned by post-pandemic population growth on reopened borders, with GDP per capita up 0.3% through the year.

Output growth continued to be exceeded by hours worked (7.1%Y/Y), describing productivity weakness. Weak growth in per capita terms and declining productivity pose challenges for the nation's policymakers, the latter currently putting upward pressure on unit labour costs, a key consideration for the RBA in its assessment of the inflation outlook.

... as household consumption continued to moderate

A weakening international economic backdrop and domestic headwinds from cost-of-living pressures and rising interest rates have contributed to slower growth in Australia. Reflecting this, household consumption was soft in Q1 (0.2%q/q) and has added little to output growth over the past couple of quarters. Residential construction activity (-1.2%q/q) has also been weighed by higher interest rates.

Exports advanced further in the March quarter and have contributed substantially to economic growth over the past year. Reopened borders have facilitated a strong recovery in domestic tourism as well as in the education sector. Business investment has been another positive, defying the broader economic slowdown and tighter financing conditions.

June quarter overview: Headwinds to economic growth persisted

Incoming data have been consistent with Australian economic growth remaining subdued in the June quarter. A range of crosscurrents continued to influence household consumption. Inflation declined further in the quarter after peaking at around 8% in late 2022, but concerns over elevated services prices prompted the RBA to hike rates at the May and June meetings, lifting the cash rate to 4.1%.

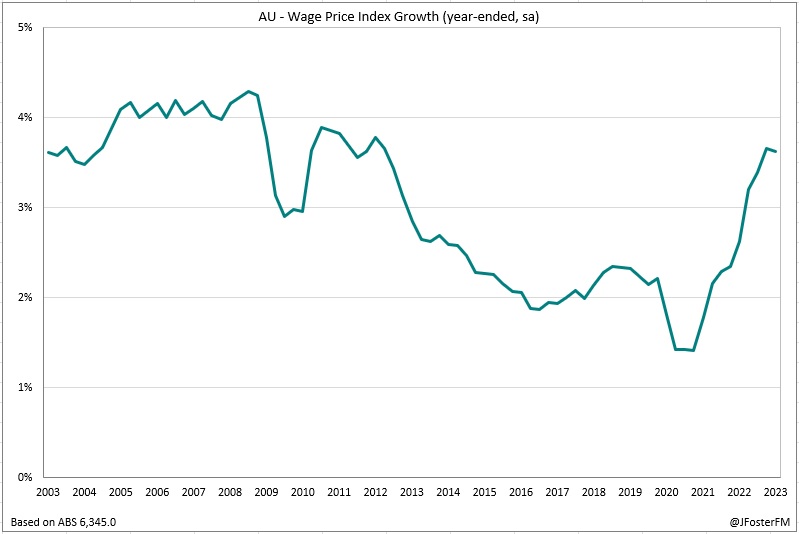

Falling inflation has eased cost-of-living pressures slightly; however, household budgets remain pressured by declining real incomes, keeping consumer sentiment stuck at very weak levels. Inflation continued to outpace wages growth (3.6%Y/Y), though a boost from larger-than-usual increases to award rates and the national minimum wage announced by the Fair Work Commission will start flowing through in the September quarter. Some targeted cost-of-living support measures included in the May budget are also on the way. These measures stem from a windfall in federal government revenues from elevated commodity prices and strong labour market conditions.

The pace of population growth is having broad effects across the economy. Population growth is boosting demand, in turn supporting employment and adding to the labour supply.

Employment lifted at a solid pace in the quarter (103.2k), keeping the unemployment rate around 3.5% at half-century lows, alongside record-high levels of labour force participation.

In the June quarter, retail sales volumes contracted by a further 0.5% to be 1.7% below their peak in Q3 2022. But much larger falls are evident in per capita terms - these volumes fell by 1.1% in Q2 and have contracted by 3.7% from the cycle high reached a year earlier - highlighting the support to consumption from population growth.

Declining retail volumes have been driven by a weakening in discretionary-related areas of goods consumption; however, services consumption has remained more resilient. Strong labour market conditions, savings accumulated during the pandemic, and an upturn in housing prices are providing a supportive impulse to consumption.

The rate of population growth continued to put pressure on the nation's housing stock. Despite a very substantial housing pipeline, supply remains tight as headwinds faced by homebuilders have held back completions. This has outweighed the effect of rising interest rates, reflected in capital housing prices rising by 6% since flooring in February, largely reversing their 9.7% peak-to-trough decline.

Summary of key dynamics in Q2

Household consumption — Pressures associated with falls in real incomes and rising interest rates continued a discretionary-driven slowdown in consumption growth. Non-food retail sales volumes contracted by 0.4% in the quarter, with the weakness mainly in household goods (-1.5%) and department stores (-1.4%). Services-related consumption appears to be remaining more resilient.

Dwelling investment — Private sector home building came close to stalling over the first half of the year as rising interest rates and headwinds from capacity constraints and margin pressures weighed on activity. Alterations continued to unwind from their pandemic highs.

Business investment — Capex advanced by 2.8% in the quarter, extending its upturn to a 10.8% rise through the year. Remains resilient to slowing economic growth and rising interest rates.

Public demand — Boosted output by around 0.5ppt in the quarter. Driven largely by expanding investment in public infrastructure projects.

Inventories — Saw a large drawdown in the June quarter (-1.9%) amid a backdrop of soft domestic demand. Expected to subtract around 1ppt from Q2 GDP.

Net exports — To add a substantial 0.8ppt to GDP growth in the quarter. Export volumes lifted 4.3% on the back of the ongoing recovery in the domestic services sector, outpacing a tepid rise in imports (0.7%).