The damage from the Delta lockdowns over the winter was smaller than expected with the Australian economy contracting by 1.9% in the September quarter against the market consensus for a 2.7% fall. Output growth was up 3.9% through the year, though that is a sharp slowdown from the 9.5% pace seen in Q2. The decline in output compares with a larger 5.4% fall in hours worked across the economy in the quarter.

Going into Q3, the Australian economy was in the expansion phase and full of running after earlier recovering from the 2020 Covid recession. But with Delta outbreaks sending around half of the population into lockdown for much of the quarter, GDP fell back to be 0.2% below its pre-pandemic level, temporarily setting back the expansion and delaying the return to its pre-pandemic path.

High-frequency data indicates a robust recovery is now underway and the economy should easily regain the lost output in Q4. A key reason for this is the elevation in accumulated household savings in the quarter, from 11.8% to 19.8%. This was driven by a rise in real household disposable income (4.3%q/q) as the federal government ramped up its Covid-19 Disaster Payments to levels approaching the JobKeeper wage subsidy of 2020. Savings were also running up due to falling household consumption (-4.8%q/q) during the lockdowns. However, there are also headwinds to the recovery building from uncertainty relating to the new variant, the withdrawal of fiscal and monetary stimulus and capacity constraints in some sectors.

Looking more broadly at Q3's outcome, it was the decline in household consumption that drove the overall contraction in GDP.

Household consumption was close to returning to pre-pandemic levels in Q2, but it has now slid back to be 5.2% lower than at the end of 2019. The largest falls were in services (-9.5%q/q) and discretionary (-11.3%q/q) areas as these categories dropped back to be around 10-15% below pre-pandemic volumes respectively. In particular, the lockdowns drove significant falls in consumption for transport services (-40.9%q/q), hotels, cafes and restaurants (-21.3%q/q) and recreation and culture services (-11.8%q/q). Conversely, both goods (2.3%) and essential (1.1%) consumption remain above end 2019 levels. However, goods consumption overall was down in Q3 (-3.3%) on the back of falls in vehicle (-8.7%q/q) and fuel sales (-13.1%q/q), furniture and furnishings (-4.6%q/q) and clothing and footwear (-22%q/q).

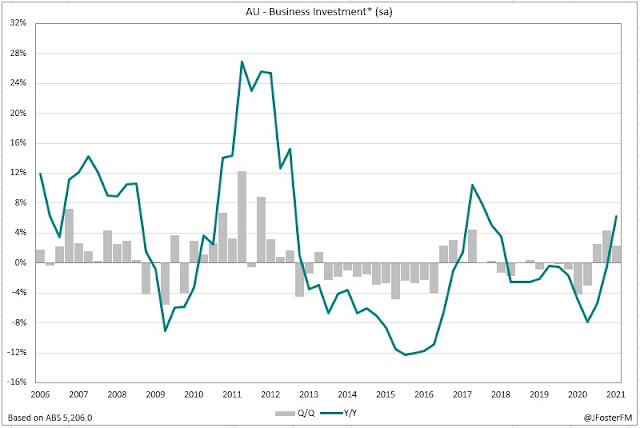

Inventories were a large drag on activity in the quarter (-1.3ppt), mainly on a sharp fall in wholesale inventories with the cuts seen in global motor vehicle production due to input shortages lowering the inventories of domestic motor vehicle dealerships. Business investment contracted by 1.1%q/q as the upswing in equipment spending (-3.1%) was paused during the lockdowns and potentially slowed by the global supply chain pressures. Public demand lifted sharply (3.3%) to add to growth as governments stepped up the rollout of the Covid-19 vaccines. Net exports (+1ppt) reversed their decline from the previous quarter as resources exports rebounded and imports contracted in line with weak domestic demand conditions.

Link to the full review here