Australia's national accounts for the September quarter are scheduled to be released by the ABS today at 11:30am (AEDT). Conditions in the Australian economy deteriorated significantly in Q3 as the expansion phase gave way to the return of lockdowns following outbreaks of the Delta variant of Covid-19. Lockdowns were in place for around half of the Australian population for much of the quarter, leading the public health authorities to accelerate the rollout of the vaccine to meet state and national targets. Consensus is for GDP to have contracted by 2.7% in Q3; an outcome that would see GDP fall back below pre-pandemic levels. Prior to the Delta outbreaks, momentum in the Australian economy was strong; GDP had expanded by 0.7% in the June quarter and was up by 9.6% from the depths of the COVID recession a year earlier.

Late in Q2, the Delta variant emerged in Australia resulting in an acceleration in daily caseloads to their highest levels of the pandemic over the winter. Extended lockdowns were seen in the capital cities of the states of New South Wales and Victoria and in the Australian Capital Territory. Shorter periods of restrictions were in place at various stages in Queensland, South Australia and in the Northern Territory.

Mobility indicators in Sydney (NSW) and Melbourne (Vic) fell sharply to around the lows of earlier lockdowns but, on average, remained much more elevated across the other capitals.

Lockdowns and their associated disruptions upended the recovery in the labour market. This led to significant declines in employment levels, hours worked and in the rate of workforce participation. In response, income support through the Federal Government's Covid Disaster Payments was increased to similar levels to last year's JobKeeper wage subsidy, boosting accumulated household savings.

Household consumption was severely affected by the lockdowns as spending opportunities in retail and discretionary services were restricted. The categories of retail sales that were hardest hit during the quarter were cafes and restaurants, clothing and footwear and department stores, consistent with earlier lockdowns. However, there was a degree of substitution in spending patterns as online retail sales soared to new record highs in Q3. Retail volumes contracted by almost 9% in the quarter across NSW, Victoria and the ACT, attenuated only slightly by a 1.6% rise across the rest of the nation.

Due in part to restrictions on property inspections, activity in the key Sydney and Melbourne housing markets slowed. However, housing prices continued to rise with the increase in the national median price pressing 5% in the quarter. Different from earlier lockdowns, tighter restrictions were placed on construction activity. Work on sites was temporarily suspended in Sydney and its surrounding areas and statewide in Victoria late in the quarter. Capacity constraints were an increasing headwind for residential construction. The lockdowns also disrupted the upswing in business investment as non-residential construction activity was restricted and equipment spending weakened. Net exports appeared to have rebounded in the quarter after subtracting heavily from GDP in Q2 when adverse weather conditions affected resources exports. During Q3, pressures in global supply chains and energy shortages pushed up prices for the nation's coal and LNG exports, though iron prices fell from elevated levels.

As it stands | National Accounts — GDP

Ahead of the Delta lockdowns momentum in the Australian economy was strong. Real GDP expanded by a stronger-than-expected 0.7% in Q2, taking growth over the first half of the year to 2.6%. Household consumption was the main driver of growth in Q2 as spending on discretionary services continued to recover. Australian GDP had rebounded by 9.6% from the depths of the national lockdown a year earlier and was 1.6% above its pre-Covid level.

Offshore, accelerating vaccine rollouts enabled restrictions to be eased, in turn supporting a pick-up in economic growth and keeping demand for Australia's key commodity exports elevated. Across OECD economies, GDP increased by 1.7% in Q2 from growth of 0.7% in Q1. The wider availability of consumption opportunities for households, particularly in services, drove sharp rebounds in the UK (5.5% from -1.4%) and in the euro area (2.2% from -0.3%) after lockdowns had been lifted early in the summer. In the US, output expanded at a solid pace of 1.6% in Q2, leading to GDP retracing its pandemic-induced decline. Meanwhile, the expansion in China continued with output rising by 1.2% in the quarter after a soft start to the year.

In Australia, household consumption lifted by 1.1%q/q and was now only just below its pre-pandemic level. Strong sentiment, accumulated savings and eased restrictions were continuing to rebalance the profile of household spending, with discretionary (1.6%q/q) and services consumption (1.3%q/q) recovering further. This was also supported by the recovery in the labour market through the boost to labour incomes. However; on aggregate, real household disposable income contracted in the quarter (-1.0%), mainly reflecting the withdrawal of the JobKeeper wage subsidy. Rising consumption against a fall in real income drove a decline in the household saving ratio, but it remained elevated at 9.7%.

Private investment lifted by 2.8% in the quarter, continuing its expansion on the back of stimulus measures and the strength of domestic demand conditions. However, there was a sharp slowing in residential construction activity (1.7%) compared to the previous two quarters. This reflected capacity constraints in the sector following the strong run-up in demand generated by the HomeBuilder scheme, rising housing prices and low interest rates. Business investment recovered to pre-pandemic levels following a 2.3% rise in the quarter. This had been driven by a strong rebound in equipment spending, supported by tax incentives and as a response to meet the strength in consumer demand.

These factors had contributed to a substantial rise in imports over recent quarters. Exports, however, contracted sharply in Q2 (-3.2%) due to adverse weather conditions hampering resource shipments. As a result, net exports weighed heavily on activity in Q2 (-1ppt).

Key dynamics in Q3 | National Accounts — GDP

Household consumption — Spending opportunities were heavily restricted by lockdowns across large parts of the nation in Q3. Retail sales volumes contracted by 4.4% in the quarter, their largest fall on record with the non-essential and discretionary services categories hardest hit. However, online sales surged to new peaks. Accumulated household savings were likely boosted by enhanced income support measures as the labour market recovery was disrupted by the lockdowns. Consumer sentiment declined from elevated levels but showed more resilience than in 2020.

Dwelling investment — Dual headwinds from the lockdowns and capacity constraints arising from materials and labour shortages paused the upswing in the residential construction cycle. In Q3, private sector residential work came in flat for the second quarter in succession. New home building went backwards for the first time in a year in Q3 (-0.8%) but was attenuated by a re-acceleration in alteration work (6%).

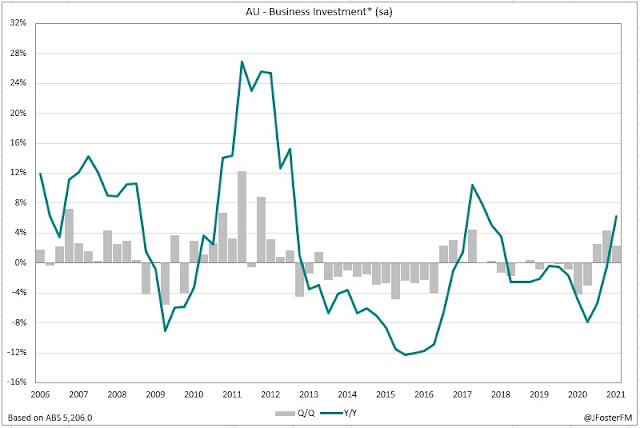

Business investment — The rebound in the capex cycle from the COVID recession was setback by the Delta lockdowns. Capex contracted by 2.2% in Q3, its first quarter-on-quarter decline in a year. The weakness was centred in equipment capex (-4.1%q/q) as the lockdowns delayed spending, with the outturn potentially accentuated by the global supply chain pressures.

Public demand — Spending by governments at the federal and state levels accelerated in Q3 (3.6%q/q) as the rollout of Covid-19 vaccines was stepped up.

Inventories — Inventory levels fell in the quarter amid the constraints in global supply chains and the weakness in demand conditions associated with the domestic lockdowns.

Net exports — A sizeable contribution to Q3 GDP of 1ppt will come from net exports. Export volumes were up 1.2%q/q supported by a rebound in resources exports. Pressures in global supply chains and the lockdowns drove a 4%q/q contraction in imports.