The most widely followed curve by markets — the spread between the US 3-month and 10-year yields — has inverted, as shown in our chart of the week (below). Historically, inversion of the 3-month 10-year spread has been a reliable predictor of an upcoming recession in the US, with a lead time of roughly 12 to 18 months. Only time will tell if things turn out differently on this occasion — and there are sound arguments as to why signals from the yield curve may not be as predictive as they have been in the past — though markets are clearly wary of signs of late cycle weakness given the US is fast approaching its longest period of economic expansion on record. Meanwhile, the third and final estimate of US GDP growth in Q4 was this week trimmed to an annualised pace of 2.2%, down from 2.6% in Q3. Forward-looking PMI data indicates that GDP growth in Q1 is likely to come in around 2% on an annualised basis.

Chart of the week

Brexit's state of bedlam showed few signs of abating this week. Firstly, MP's voted in favour of seizing control of the Brexit process for a day in an attempt to try and find a way out of the impasse. However, a series of non-binding indicative votes held on Wednesday only resulted in MP's voting against all 8 options put forward as alternatives to PM Theresa May's Brexit deal. PM May announced during the week that she would resign if her existing deal was passed by the parliament. On Friday (UK time), a parliamentary vote took place on the withdrawal agreement aspect (relating to the terms of the UK's exit from the EU and the Irish backstop) of the PM's Brexit proposal, which was defeated by a margin of 286 to 344 placing further uncertainty over the path forward.

In Europe, European Central Bank (ECB) President Mario Draghi maintained that the policy stance would remain supportive, including "if necessary" possible measures aimed at preserving "the favourable implications of negative rates for the economy, while mitigating the side effects, if any". This is in relation to the ECB's deposit facility rate which is presently set at -0.4%. While this is aimed at incentivising lending to the real economy, 'side effects' refer to the potential impact on the profitability of the euro area's banks, as they effectively pay to maintain excess liquidity with the ECB on an overnight basis. Media reports had indicated that there had been discussions within the ECB around introducing a tiered deposit rate that would be aimed at reducing some of that cost faced by the banks amid a broader slowing in economic activity in the region. Such a move could be interpreted as indicating that negative rates were likely to remain part of the policy mix for a more extended period of time.

Closer to home, the Reserve Bank of New Zealand was the latest central bank to move to a dovish stance by noting in its latest policy decision statement that "the more likely direction of our next (rates) move is down" with risks to the outlook having "shifted to the downside" in response to a weaker forecast for global growth and slowing domestic demand.

—

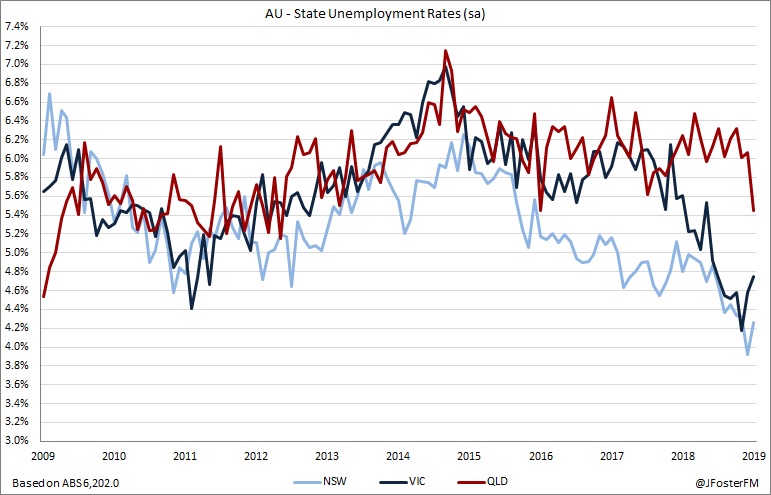

Staying with the RBA theme, Assistant Governor (Economic) Luci Ellis delivered a speech titled: What's Up (and Down) With Households? that provided a highly insightful perspective on the Bank's thinking around the household sector. It is very clear that the Bank has gained confidence from the strengthening in labour market conditions over the past year or so and highlighted the broad-based nature of employment growth. It has noted a gradual rise in wages growth — particularly in the private sector — citing tightening conditions, removal of wage freezes and increases to awards, though the unemployment rate was still some way off being consistent with a more material pick-up.

The impact of slow income growth and expectations for that to persist has weighed on household consumption. The overall growth in households' income has been impacted by softness in labour income (wages and bonuses) as well as from non-labour sources (social assistance and income derived from rent, other investments and businesses). However, the key takeaway was that growth in taxes paid by households has over recent years been increasing by an above-average margin relative to the rate of growth in their gross income, with that situation becoming more pronounced over the past year. That analysis sets the scene ahead of next week's Federal Budget (April 2), in which fiscal policy through tax relief and infrastructure investment is likely to feature prominently.

In terms of data, the ABS' Job Vacancies series showed a 1.4% rise over the quarter to February and by 9.9% through the year. While the pace of growth is slowing, it remains relatively solid and the total number of vacancies is at a record high, all of which appears to indicate that a near-term deterioration in labour market conditions is unlikely.

Private sector credit growth lifted by 0.3% in February, a slightly stronger-than-anticipated outcome, though the annual pace eased to 4.2% from 4.3%. Total credit growth for housing slowed to a 4.2% annual rate — its lowest on record dating back to 1977 — reflecting the impact of tight lending assessment criteria following the banking royal commission. Growth to the owner-occupier segment was 5.9%Y/Y and just 0.9%Y/Y to investors marking a new record low.