Labour Force Survey — February | By the numbers

- Employment increased by a net 4,600 in seasonally-adjusted terms, which was well below the meadian forecast for +15,000. January's intially reported 39,100 increase was revised down to +38,300.

- The nation's unemployment rate declined to 4.9% from 5.0% (exp: 5.0%, prior: 5.0%).

- The underutilisation rate fell by 0.2ppt to 13.1%, while the underemployment rate held at 8.1%.

- The participation rate declined by 0.1ppt to 65.6% (exp: 65.7%)

- Hours worked lifted by 0.2% in the month to 1.77bn and by 2.2% through the year (prior: +0.4%m/m, +3.3%Y/Y)

Labour Force Survey — February | The details

To the details, labour force participation declined from 65.7% to 65.6% in February on a seasonally-adjusted basis. That equated to 7,100 fewer people either in work or actively looking for work. With employment increasing by a net 4,600, that meant the total number of unemployed fell by 11,700, which explains the decline in the headline unemployment rate from 5.0% to 4.9% (at 2 decimal places from 5.03% to 4.95%). On a trend basis, the participation rate held at 65.7% for the 8th consecutive month and the unemployment rate at 5.0% has been unchanged for the past 3 months.

The increase in employment of 4,600 was the net result of full-time work falling by 7,300 and part-time rising by 11,900. Through the year, employment growth lifted to 2.3% from 2.2%, though that was driven by a base effect (employment fell by 3,300 in February 2018). Employment growth slowed across the second half of 2018 from a very strong level, possibly in response to notably weaker activity in the economy, but still remains solid and comfortably outpaces growth in the labour force at around 1.7 to 1.8%.

Total hours worked lifted by 0.2% in the month and by 2.2% for the year, with growth looking to be on a mildly upward trend. When adjusted for the increase in employment, average hours worked per employee in the month was little changed in February (+0.1%) and over the year (-0.1%) at 138.7 hours.

The underemployment rate remained at 8.1% but is still historically elevated indicating that there are many workers wanting more hours than they are currently receiving. The broader underutilisation measure (including the unemployed and underemployed) drifted down to 13.0% — its lowest since mid-2013.

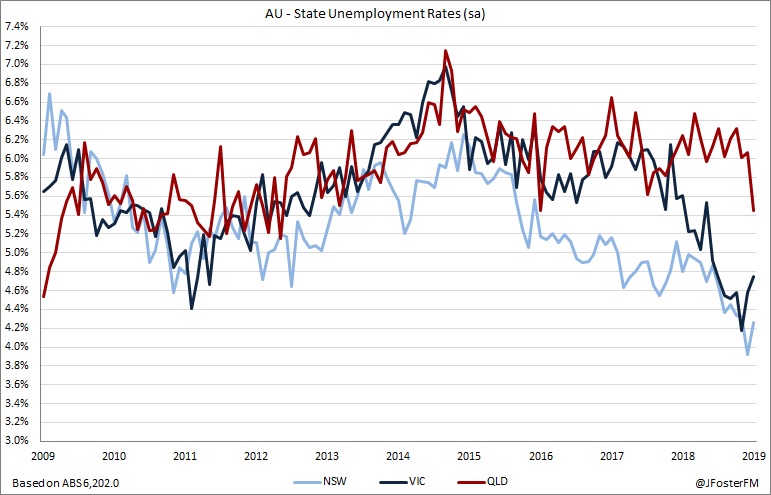

Turning to the state detail, there were some sizeable moves in unemployment rates but different from what has been reported over recent months. Unemployment in the 'major 2' increased; New South Wales +0.4ppt to 4.3% and Victoria +0.2ppt to 4.8%. That would be significant if that continued because those two states have driven national employment growth over the past year or so (see below).

Unemployment, however, declined in the other states; Queensland -0.7ppt to 5.4%, South Australia -0.6ppt to 5.7%, Western Australia -1ppt to 5.9% and Tasmania -0.5ppt to 6.5%. Though pleasing, single-month moves at the state level tend to be volatile so caution would be advisable.

Labour Force Survey — February | Insights

This was a highly anticipated release given the RBA's minutes from its March meeting highlighted that "(Board) members agreed that developments in the labour market were particularly important" in terms of its economic outlook. For the time being, there is little to suggest a deterioration in conditions has occurred, more like a softening, though the counter-argument is that labour market data are a measure that lags activity in the economy. Forward-looking indicators present risks to the employment outlook. The key consideration for markets is whether the RBA will wait for the data to confirm a potential weakening in the labour market before considering easing, or possibly look to take a more proactive stance. Given Tuesday's RBA minutes gave attention to 'tension' in the data — referring to resilient labour market conditions despite slowing economic growth that has also been experienced globally — it may lean towards the former.