US equity sentiment was bolstered by strong tech earnings, though price action was more mixed across Europe and Asia. Rate hikes will be forthcoming from the Fed and the ECB next week, but softer inflation data in Australia should keep the RBA on hold. The Bank of Japan left all settings unchanged as Governor Ueda at his first meeting at the helm announced a wide-ranging policy review would be conducted.

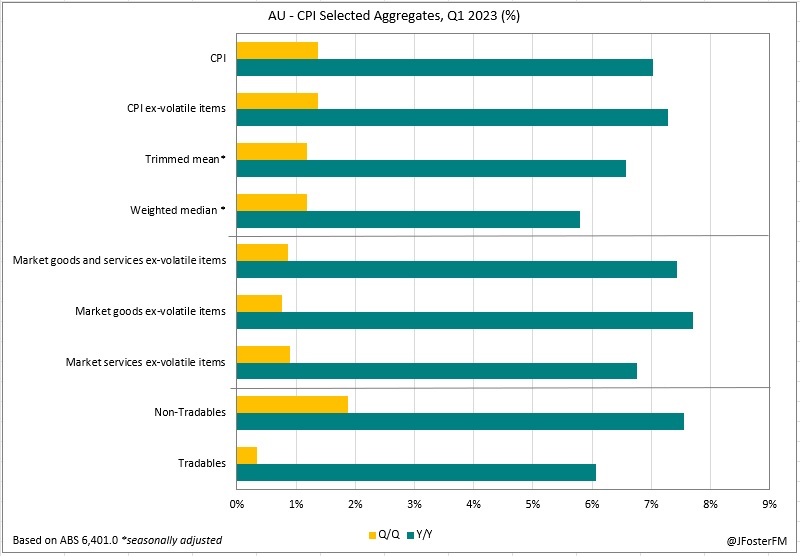

Domestically, Q1's CPI data reported a disinflationary process is now underway in Australia, which likely confirms the RBA's hiking pause will now be an extended one ahead of next week's meeting. Quarterly inflation for both headline (1.4%) and core (1.2%) printed at their slowest rates since Q4 2021, with annual inflation falling from 7.8% to 7% on a headline basis (vs 6.9% exp) and from 6.9% to 6.6% (vs 6.7%) on the core rate (full review here).

Easing global inflationary pressures are flowing through to Australia. Inflation in traded goods and services slowed sharply from 8.7% to 6.1%Y/Y on the back of falling prices for fuel and durable goods, reflecting eased supply constraints and softer demand. Separate data showed import prices fell by 4.2% in Q1, their largest decline in more than a decade. The domestic inflation pulse - driven by areas such as health, education and energy costs - is yet to peak, though wages growth in Australia has been less responsive to these cost-of-living pressures than in many other countries, even with very strong labour market conditions.

Overall, the Q1 CPI data validates the RBA's April pause. As highlighted in last week's review, the key for policy would be how the CPI reshaped the RBA's inflation outlook, most notably the 2025 timeline for a return to the 2-3% target band, which the Board highlighted was a window relevant to its mandate. Decelerating inflation is consistent with that outlook and indicates monetary policy is appropriately calibrated at a restrictive level.

Over in the US, the Fed is widely expected to hike rates by 25bps to 5-5.25% next week. That expectation firmed after signs of resilience in the economy and ongoing wage and inflation pressures. While Q1 GDP growth slowed to 0.3%q/q (from 0.6%), there remains underlying strength in the US economy. Domestic demand picked up to rise by 0.8%q/q, its strongest lift since Q2 2021, driven by resilient household spending. Meanwhile, inflation remains stubbornly high with the Fed's preferred core PCE deflator printing in line with estimates, leaving the annual pace unchanged at 4.6%. Meanwhile, a tight labour market is keeping wage pressures elevated, with the Employment Cost Index rising by 1.2% in Q1 to 4.9% over the year (from 5.1%).

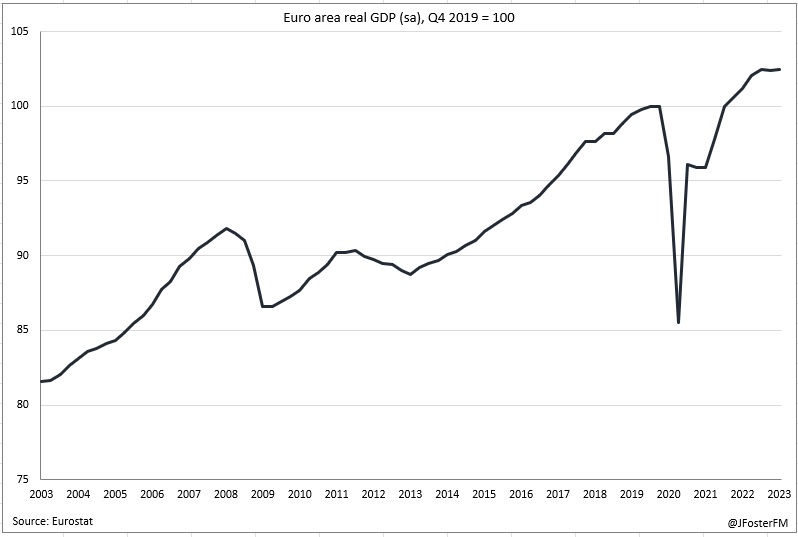

In Europe, the ECB's meeting next week continues to look like a line-ball call between a 25 or 50bps rate hike. Inflation and bank lending data due on the eve of the meeting could sway things one way or the other. What is clear is that the ECB is hiking into an economy that has stalled, as Q1 GDP growth came in at 0.1% after a flat Q4.