Australian inflation is on the way down after peaking at the end of 2022. The disinflationary pulse from offshore, particularly in goods markets, is flowing through to Australia. Underlying inflation pressures eased and will be welcomed by the RBA following its pause in April.

Consumer Price Index — Q1 | By the numbers

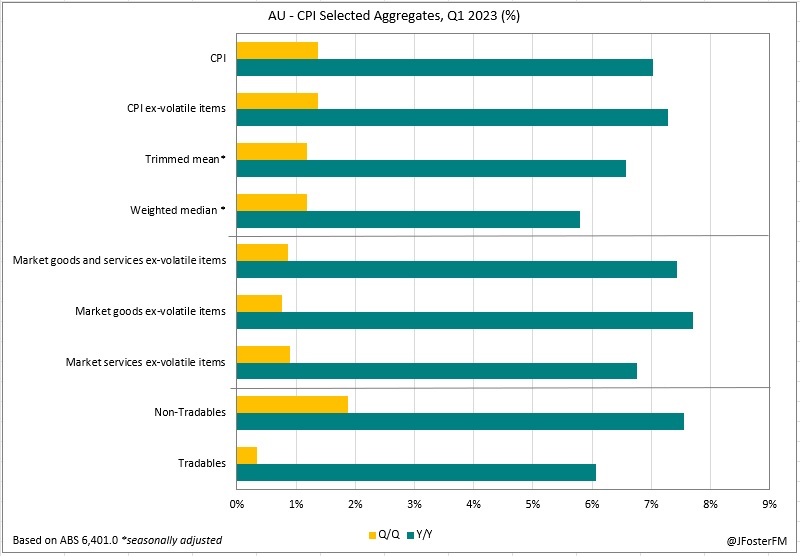

- Headline CPI was 1.4% in the March quarter, well down from 1.9% in the previous quarter but printing slightly above consensus (1.3%). Annual inflation moderated from 7.8% to 7% (vs 6.9% expected).

- The average of the three underlying CPI measures was 1.3%q/q, down from 1.8% in Q4, leaving the annual pace softer at 6.6% from 6.7%.

- The key trimmed mean measure was 1.2%q/q — softer than expected (1.4%) — from 1.7% in Q4. The annual pace declined to 6.6% from 6.9% (vs 6.7%).

Consumer Price Index — Q1 | The details

Australian inflation moderated from 30-year highs in the March quarter, confirming inflation peaked at the back end of 2022. Both headline (1.4%) and trimmed mean (or core) inflation (1.2%) posted their slowest quarterly rises since Q4 2021. In year-ended terms, headline inflation came down from 7.8% to 7% and the core rate eased to 6.6% from 6.9%.

In many countries around the world, inflation is slowing after peaking in 2022. An easing of the inflationary pressures generated offshore - a major reason for the surge in inflation in Australia over the past year - is starting to flow through to domestic prices.

This is evident in tradables inflation - prices for goods and services bought into the country - slowing sharply to a 0.3% rise in Q1 (its weakest outturn since Q4 2020), cutting the annual pace from 8.7% to 6.1%. This reflects falls in fuel prices from the highs seen following the war in Ukraine and further improvements to the disruptions that had hampered global supply chains through the pandemic. Softer demand for goods has also played a role, with spending rotating to services post the pandemic.

As a result, goods inflation in Australia slowed to 1.2% in Q1 and 7.6% over the year (down from a peak of 9.6%). This disinflationary impulse means the drivers of inflation are shifting towards services (and to more domestically generated sources). Services inflation was softer in Q1 at 1.7% than in Q4 (2.1%), though the annual pace has yet to top out, ticking up from 5.5% to 6.1%.

At a more granular level, the major drivers of inflation were from domestic sources, and in services-related areas. This included rises in utilities on the back of surging household energy prices (14.3%q/q) and secondary education costs (4.9%q/q) reflecting rises in school fees.

Consumer Price Index — Q1 | Insights

In my view, the key aspect of today's report was the easing in core inflation. While still far above the 2-3% target band, this will be taken as a welcome development by the RBA. The quarterly rate of 1.2% was down from an average pace of 1.7% in 2022. Ahead of next week's meeting, the RBA will be updating its inflation outlook. The current outlook is for core inflation to decline to 4.3% by year-end. And based on today's report, I think that outlook remains on track, which validates the Board's decision in April to pause rate hikes.