Australia's National Accounts showed the domestic economy grew by +0.9% in the June quarter (Q2) lifting annual growth to its strongest level in nearly six years at +3.4%. The result was stronger than the market forecast for +0.7%q/q and +2.9%Y/Y.

Economic growth in the March quarter (Q1) was upwardly revised by the Australian Bureau of Statistics (ABS) in this update to +1.1%q/q and +3.2%Y/Y.

With potential growth in Australia estimated at around 2.75% to 3% in annual terms, the domestic economy has been running at an above-trend pace through the first half of 2018. This was broadly in line with Reserve Bank of Australia forecasts, which expect growth to remain above-trend over the next year.

Headline growth has been boosted by a strong rate of population growth, estimated at around +1.6%Y/Y. Adjusting for that impact, GDP growth on a per capita basis was a more moderate +0.5% in Q2 and +1.8%Y/Y. Though subdued, the annual rate lifted to its highest level since Q2, 2012.

GDP — Q2 | Expenditure: GDP (E) +0.7%q/q, +3.4%Y/Y

Household consumption (+0.7%q/q, +3.0%Y/Y) — The household sector drove growth in Q2 adding +0.4ppt to the headline figure. The lift in spending was broadly-based across the discretionary and non-discretionary areas. For context, the annual rate of +3% is around average in the post-financial crisis decade.

The key issue of persistently weak income growth remains. Growth in real household income is tracking at +1.7%Y/Y, which is unchanged year to date — meaning that households have had to direct more of their disposable income towards consumption. As a result, the household saving ratio fell to 1%, which is the lowest since Q4, 2007. Gaining increased focus recently has been the decline in national property prices. This could be the catalyst for households to rebuild savings.

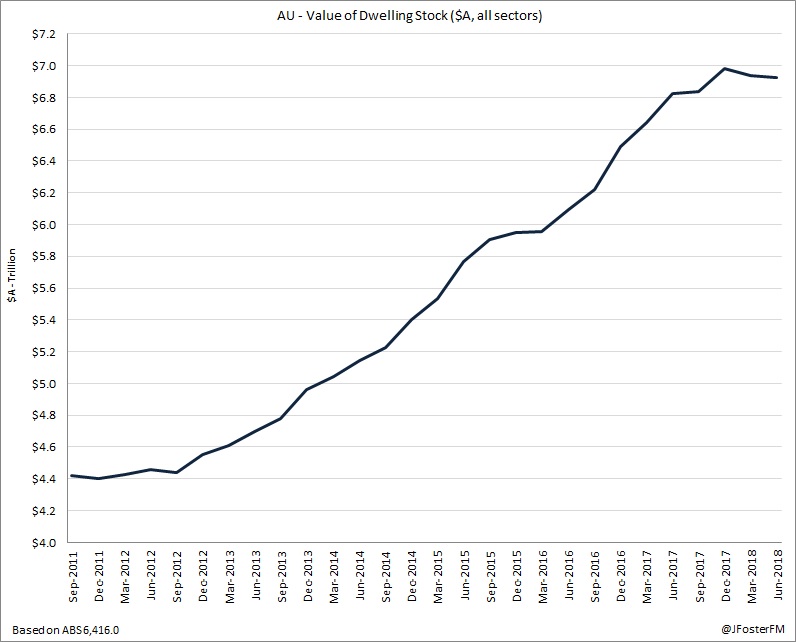

Dwelling Investment (+1.7%q/q, +3.8%Y/Y) — Residential construction drove this result overcoming weakness from renovations to add modestly to growth (+0.1ppt) in the quarter. The pipeline of work is strong, particularly in NSW and Victoria, but activity is likely to ease matching the moderation in building approvals from historic levels while financing conditions have tightened.

Business Investment (-0.2%q/q, +4.1%Y/Y) — Business investment has supported activity over the past year. Non-mining investment is trending up and the drag from the unwind in mining investment from the peak reached around 4-5 years ago has almost reached the end of the line. Q2’s result was impacted by weakness in equipment spending (-1.7%) and mining sector infrastructure (-0.8%).

Public Demand (+0.6%q/q, +4.8%Y/Y) — The public sector has greatly supported activity in recent years, which has been powered by consumption and a ramp-up in investment. Spending has been boosted by the rollout of the National Disability Insurance Scheme — a major policy initiative in the health sector — and investment, particularly in transport infrastructure, has been hastened with the nation responding to the needs emanating from strong population growth.

Net Exports (+0.1ppt in Q2, -0.7pptY/Y) — International trade added to growth in Q2 but subtracted over the year. In Q2, export volumes increased +1.1% while imports lifted a smaller 0.4%. The export performance has been supported by the resources sectors, while imports have been lifting in line with improving business investment.

GDP — Q2 | Incomes: GDP (I) +0.9%q/q, +3.7%Y/Y

Nominal GDP growth was +1.0% in Q2 — a more modest outcome than recorded in Q1 at +2.4%. Annual growth lifted from +4% to +5.5%, though this reflected a base effect as the decline of -0.4% from Q2 last year fell out of the calculation. The recent peak came in Q1, 2017 where annual growth was +7.7%, which then fell back to +3.6% in Q4.

Australia’s Terms of Trade fell -1.3% in the quarter, with commodity prices easing after a stronger outcome in Q1 that drove an increase of +3.5%. However, the Terms of Trade are still ahead over the past year (+2.1%), which has provided a lift to national income.

The distribution of that income has, however, been unbalanced. Total corporate gross profits increased +1.0% in Q2 to +8.8%Y/Y. Within this, profit growth for private non-financial companies is running at +9.7%Y/Y and +6.2%Y/Y for financial companies. Total corporate profit growth is still strong even after moderating from an average pace of +17.5%Y/Y between Q4, 2016 and Q3, 2017.

Wages and salaries paid to employees lifted by +0.7% in Q2, while annual growth eased slightly to +4.8%. This, however, remains around the level from the previous three quarters and well above the low of +1.4% that prevailed between Q4, 2016 and Q1, 2017. Over the past few years, low rates of wages growth have been persistent and this has restricted growth in employee’s income. Hours worked increased +1.1% in Q2 to +2.3%Y/Y.

GDP — Q2 | Production: GDP (P) +1.0%q/q, +3.1%Y/Y

Output growth rates across the industries for the quarter and year are broken down in the chart, below.

The strength in healthcare related services is notable and fits with the needs of a growing population. The sector is also the nation’s largest employer and employment growth has been strong over the past couple of years.

Drought conditions impacting the eastern states is an emergent risk, which could have flow-on implications for agricultural exports.

GDP — Q2 | Prices

Price levels remain subdued in line with the more narrowly-focused ABS inflation data. The GDP implicit price deflator — the broadest measure of inflation across the economy — lifted +0.2% in Q2 to +2.0%Y/Y. Though the lift in annual growth was sharp; from +0.8% to +2.0%, that was base effect impacted.

The GDP implicit price deflator typically tracks changes in the Terms of Trade. With the Terms of Trade moderating over the past few quarters after a spike in 2016-2017, economy-wide inflation has pulled back.

The household consumption deflator — the closest proxy to the ABS’ Consumer Price Index (CPI) — reflects dynamic changes in purchasing patterns over time as consumers switch towards cheaper goods and services. This measure was soft in Q2 at +0.2% easing annual growth from +1.6% to +1.5%. The CPI in Q2 was +0.4% and +2.1%Y/Y. This points to downside risks to the CPI measurement in the quarters ahead.

GDP — Q2 | Productivity

Productivity growth in Australia has been weak in recent years matching with the experiences of several other major advanced global economies. This shows little sign of improving.

While total hours worked across the economy increased by +1.1% in Q2 (+2.3%Y/Y), this was faster than output growth at +0.9%. As a result, GDP per hour worked fell in Q2 by -0.2%, though annual growth held at a subdued +1%.

In the market sector, real GDP per hour worked also declined by -0.2% in Q2, with annual growth easing to just +0.4%.

Analysing the inflationary pulse, the forward-looking indicators point to a soft outlook. Non-farm nominal unit labour costs — reflecting the cost of labour per unit of output — declined a further -0.4% in Q2 to drag the annual growth rate down to +0.4%, continuing their decline since the recent peak of +2.2%Y/Y in Q4, 2017.

In real-terms, non-farm unit labour costs fell -0.5% in Q2, which saw the annual rate go in reverse to -1.6%. This followed a contraction in Q1 of -2.0%, while annual growth was +0.8%. Annual growth has also been in decline since the peak from Q4 last year.

GDP — Q2 | States

Victoria remains the strongest performing state economy in the nation. Strong population growth is boosting residential construction and driving an upswing in public demand led by infrastructure investment. This has facilitated a positive spillover impact for private sector business investment. Reflecting retail sales data, household consumption is a strong +3.8%Y/Y and is running ahead of the other states.

In New South Wales, demand was soft in Q2 with declines in public demand and business investment. There are varying outlooks here; investment in public infrastructure will continue, however details around business investment are patchy. Activity in residential construction will be required to accommodate population growth. Household consumption is supported by strong employment growth, though income growth is subdued.

Demand conditions in Queensland, South Australia and Tasmania were at or around the pace of national domestic demand growth (+3.4%Y/Y).

Conditions in Western Australia are no longer in decline, but unwinding mining sector investment remains a drag as does residential construction. Public demand is providing some offset.