Building Approvals — February | By the numbers

- Dwelling approvals (private and public sectors) in seasonally adjusted terms lifted by 19.9% in February to 15,698; well ahead of the median forecast for a 4.0% rise. In January, approvals fell by 15.1% (revised from -15.3%).

- In year on year terms, approvals fell by 5.8% from -11.1% in the previous month (revised from -11.3%).

- House approvals softened by 1.7% in the month to 8,623 (prior rev: 0.7%mth) for a decline of 5.1% over the year (prior rev: -7.4%yr).

- Unit approvals surged by 63.7% to 7,075 — after gapping down by 35.6% in January — reducing the annual decline from -17.8% to -6.7%.

Building Approvals — February | The details

Dwelling approvals continued their volatile start to 2020 with February's 19.9% rise (+2,602) more than offseting January's 15.1% fall (-2,330). The ABS reported no significant impact from either the summer bushfires or covid-19 so these results probably reflect seasonality more than anything. The surge in unit approvals of 63.7% (+2,752) after the pullback in January of -35.6% (-2,387) appears consistent with that assessment. The more stable house segment saw approvals easing modestly by 1.7% (-150) following January's 0.7% increase (+57).

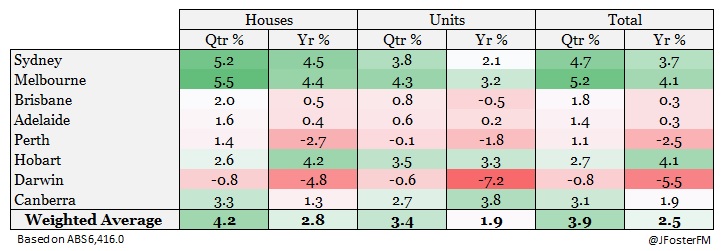

The state outcomes are summarised in the table, below. Aside from Queensland (-5.2%mth), the other states saw approvals increase in February, which was largely a reverse of what occurred in January. Approvals snapped back in Victoria (-33.9% to +55.7%), South Australia (-9.6% to 11.1%) and Western Australia (-6.0% to 6.2%). New South Wales strengthened (4.1% to 12.7%) as did Tasmania (1.3% to 12.8%). Against the run of play, Queensland rolled over in February after rising strongly (8.9%) in the month prior.

The value of alteration work approved to existing residential properties pulled back by 7.7% in February to $687.9m to mostly offset January's 9.9% rise. Approvals in the non-residential segment also declined in the month (-6.1%) to $4.359 after lifting by 4.5% in January.

Building Approvals — February | Insights

The headline increase in dwelling approvals (19.9%) was flattered by the surge in unit approvals (63.7%) that was likely associated with seasonal factors. In March, concerns around the covid-19 outbreak escalated in Australia resulting in widespread social distancing measures coming on before the end of the month. With those restrictions seeming set to remain in place for at least the next few months, dwelling approvals are likely to weaken and intensify the headwinds impacting the residential construction sector that as of Q4 2019 was mired in its steepest downturn since 2012.

The headline increase in dwelling approvals (19.9%) was flattered by the surge in unit approvals (63.7%) that was likely associated with seasonal factors. In March, concerns around the covid-19 outbreak escalated in Australia resulting in widespread social distancing measures coming on before the end of the month. With those restrictions seeming set to remain in place for at least the next few months, dwelling approvals are likely to weaken and intensify the headwinds impacting the residential construction sector that as of Q4 2019 was mired in its steepest downturn since 2012.