Both the US and euro area economies this week reported strong rebounds in activity in the September quarter as shutdown orders were lifted, though this progress is now at risk of faltering due to the ever-present threat of the virus as the northern winter draws near. At the centre of these concerns is Europe where surging case numbers have led to a broadening and tightening of restrictions across the continent, with France and Germany — the two largest economies in the bloc — entering national shutdowns of differing magnitudes, though not as stringent as was implemented during the first wave. The deterioration in the situation has had an immediate impact on the data to hand for October, as seen last week by the euro area PMI reading falling into contractionary territory (49.4), while this week the recent recovery in the European Commission's economic sentiment index stalled (90.9) and the employment expectations measure was starting to turn over (89.8). Just a short while ago, conditions were looking very different on the back of a strong rebound in economic activity through the initial phase of the reopening. After a 15.1% decline in output over the first half of the year, euro area real GDP was reported this week to have rebounded by a much stronger than forecast 12.7% in the September quarter (-4.3%Y/Y). While this still left the level of GDP in the euro area 4.3% lower than its pre-pandemic level, the momentum was heading in the right direction (see chart, below).

Where things stand now, however, was best summed up by the message from European Central Bank President Christine Lagarde at this week's post-policy meeting press conference that "the economic recovery is losing momentum more rapidly than expected". While the Governing Council left its policy settings unchanged at this meeting, the decision statement effectively gave the pre-commitment that more stimulus will be forthcoming in December by noting it "will recalibrate its instruments" to coincide with the release of an updated set of economic forecasts that factor in these latest virus-related developments. With the economic outlook deteriorating in response to more restrictions on activity, President Lagarde outlined that preparatory work is already underway in determining what its next steps will be but the message was that it will be examining all of its instruments, including its various asset purchase programs and term funding schemes. Also at the ECB this week, its latest bank lending survey was released for the September quarter that reported banks' credit standards had tightened over the period as businesses deal with the fallout from the pandemic.

Chart of the week

As there were further signs this week of the strength in the recovery of the US economy, markets were left to consider its durability amid an acceleration in virus cases to their highest daily level of the pandemic so far on Thursday (88.5k) and uncertainty around the policy outlook, in particular on prospects for fiscal stimulus, on the doorstep of the presidential election. There may have been some sense of fragility to these concerns evident in the latest University of Michigan consumer sentiment data with the current economic conditions index declining by 2.2% in the month of October. This uncertainty follows the strongest rise in quarterly GDP on record in the US as the reopening effort led to output printing at an above consensus pace of 7.4%q/q (-2.9%Y/Y). Coming after Q2's 9.0% contraction, this left the level of GDP still 3.5% below where it was before the pandemic hit (see chart, above). On the underlying details, after falling by 9.6%q/q in Q2, household consumption rebounded by 8.9%q/q with spending on goods accelerating (9.8%q/q) helped by earlier stimulus measures as services demand made an incomplete recovery (8.5%q/q). Perhaps of most surprise was the strength that came through in business investment, with equipment spending surging by 14.2%q/q, though this was moderated by weakness in non-residential construction (-3.9%q/q). Highlighted in last week's review was the robustness that has been evident in the US housing market since the reopening and this was underscored in the GDP report with new residential construction advancing by 12.3% in Q3 to stand 5.1% above the level that prevailed at the end of 2019.

— — —

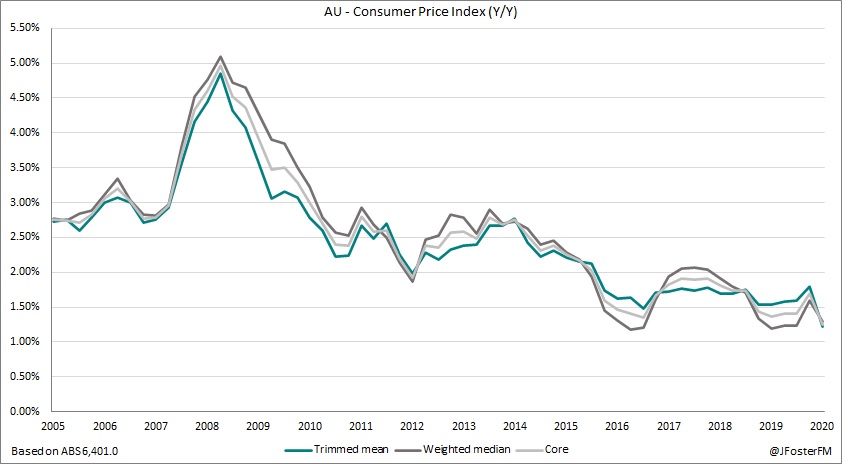

Turning to the domestic perspective, the main focus of the past week was the September quarter Consumer Price Index (CPI) data. After recording its sharpest quarterly fall on record of -1.9% in the shutdown-impacted June quarter, headline CPI rebounded by 1.6% in the September quarter, coming in slightly above the median estimate of 1.5% (full review here). Driving the reversal was the end of the period of free childcare services as one of the Federal Government's pandemic response measures amid the shutdown and higher petrol prices in response to a lift in demand as restrictions eased. On this result, annual CPI lifted off its 23-year low of -0.3% to 0.7%, which compares with its 2.2% pace in the March quarter ahead of the onset of the pandemic. Outside the impact of childcare fees returning and petrol prices recovering the inflationary pulse was very weak. Housing inflation was flat in Q3 as rents declined for a second consecutive quarter on the effects of rent reduction mechanisms and higher vacancy rates, utilities prices went backwards on support measures from state governments and new dwelling costs were capped to a modest rise in response to the Federal Government's HomeBuilder scheme. The report this week reiterated that government policy decisions were behind the disinflationary shock that hit the economy in the June quarter and while has partially reversed, inflation on an underlying basis remains a long way below the Reserve Bank of Australia's 2-3% target range.

The Bank's preferred trimmed mean measure came in at 0.4% on the quarter to more than offset Q2's 0.2% fall, though the annual pace held steady at 1.2%. Inflation is currently a secondary consideration for the RBA relative to its full employment objective, but this outcome only adds weight to the widespread expectation in the markets that the Board will announce a significant easing in its monetary policy stance on Tuesday. The expecation is the the Board will cut its rates structure by 15 basis points to 0.1% across the targets for the cash rate and 3-year Australian Government bond yield and on the Term Funding Facility. In addition, given the recent speech from Governor Philip Lowe that highlighted the importance of balance sheet expansion, it is likely that the Board will announce its intention to buy government bonds in the 5 to 10-year maturity range. Markets have been speculating about the possibility of a target of $100bn for these purchases, though my read on the situation is that it is unlikely to go down the path of a defined target, with the focus instead to be on retaining maximum flexibility to adjust purchases across the curve in these uncertain times as required, dictated either by economic conditions or market functioning and more on this will be covered in next week's preview.