Australia's Federal Budget for 2020/21 extends the response from the nation's fiscal authorities to the COVID-19 pandemic, providing a further $41.4bn of new measures in the current financial year since the July Economic and Fiscal Update, with the focus around providing incentives for firms to hire and invest and boosting household income through the earlier introduction of personal income tax cuts. The Government's economic support measures now total $257bn (13% of GDP) over the forward estimates, with around $145bn of this front-loaded into 2020/21.

Federal Budget 2020/21 | Budget Position

The budget deficit for 2020/21 is projected to be wider than earlier expected at $213.7bn (11% of GDP) compared to the $184.5bn (9.7% of GDP) estimate in the July Economic and Fiscal Update. The profile of the deficit is projected to narrow over the out-years to $112bn in 2021/22, $87.9bn in 2022/23 and to $66.9bn in 2023/24.

The deterioration in the budget position reflects the focus of the Government to provide the economy with emergency support as it deals with the most severe crisis it has faced in the post-war period. For 2020/21, policy decisions taken by the Government since December are estimated to provide support to the effect of $159.8bn. Within this figure, Budget 2020/21 contains $41.4bn of additional measures following on from the $118.4bn of announcements already reflected in the Treasurer's July update. The nature of the Government's response switches in 2021/22 through a hand-off from the payments side of its budget as temporary support programs (JobKeeper and enhanced JobSeeker payments) are withdrawn to the revenue side as economic activity rebounds in response to earlier stimulus and a further easing of restrictions, while the role of automatic stabilisers through the tax system and safety nets will remain prevalent for some years beyond this, which is highlighted by the size of the parameter changes (see table above) over the remainder of the forward estimates period.

The forecast profile for the budget deficit results in Government net debt expanding from its pre-pandemic level of 19.2% of GDP to a forecast 36.1% of GDP by 2020/21 aligning with the full scale of the fiscal response. A declining profile in the deficit onwards from 2021/22 sees growth in net debt moderate to 43.8% of GDP by 2023/24. The interest cost on this debt has lowered in response to the downward shift in global bond yields as central banks cut policy rates aggressively and expanded asset purchases following the onset of the pandemic. Net interest payments are forecast at 0.7% of GDP in 2020/21 and 2021/22 and 0.6% of GDP over the period out to 2023/24. The AOFM has since indicated in their Issuance Program statement that total issuance for 2020/21 is estimated at around $240bn, with around $117bn of this already completed.

Federal Budget 2020/21 | Payments and Receipts

Government payments as a share of GDP are forecast to surge to a peak of 34.8% in 2020/21, which compares with a pre-pandemic long-run average of around 25%. The level then declines over the out-years to 26.9% of GDP in 2023/24, reflecting the withdrawal of the temporary support programs.

Receipts as a share of GDP before the pandemic were at 24.9% but the shock to the economy caused by its onset and the measures to contain the virus sees the Government's revenues roll over and maintain a downward trajectory through to 2021/22 at 22.5% of GDP. This is eventually forecast to begin turning higher from 2022/23, well past the time when the level of Australian GDP has recovered its pandemic-induced decline.

Federal Budget 2020/21 | Policy Measures

The major policy initiatives included in Budget 2020/21 are summarised in the table, below, with the focus on measures that are targeted towards incentivising firms to hire and invest, while bringing forward tax relief to households.

On the payments side, the largest item is the extension to the JobKeeper scheme through to the end of March 2021 that costs $15.6bn. The Government's JobMaker plan includes an incentive for businesses to hire young workers as the demographic hardest hit by the upheaval in the labour market. A hiring credit of between $100-$200 a week will be available to employers who take on previously unemployed young workers (aged between 16-35) payable for 12 months for new jobs (minimum 20 hours/wk) created over the period up to 6 October next year. Additionally, there is an expansion of the existing wage subsidy scheme for new apprentices and trainees. Infrastructure is also a key focus with $6.7bn in funding available to the states and territories over the next 4 years to roll out new projects on an accelerated basis. More support payments will be forthcoming, with pensioners and other welfare recipients to receive two additional payments of $250.

Receipts measures are focused on boosting business investment and providing tax relief. On business investment, firms with turnover of up to $5bn (covering 99% of businesses) will be able to fully write-off the cost of depreciable assets (with no limit on the value of the asset) in the year of installation through to June 2022. This is expected to support around $200bn of investment, costing the Budget $26.7bn over the forward estimates. Firms will also be allowed to temporarily carry-back losses incurred over the period up to 2021/22 to offset tax paid since 2018/19. This will generate an estimated $31.6bn of tax refunds for firms that will become available as they lodge their tax returns in either 2020/21 or 2021/22. As was widely expected, the Government has elected to bring forward the stage 2 personal income tax cuts from its scheduled July 2022 start date to apply retrospectively from July 2020. This sees the lower threshold of the 32.5% band rise from $37k to $45k, while the lower band for the 37% threshold lifts from $90k to $120k. Meanwhile, the low- and middle-income tax offset (that was due to be removed at the commencement of the stage 2 tax cuts) will continue in 2020/21 providing tax relief of up to $1.08k for individuals and $2.16k for couples/families. The combined effect of these tax changes is estimated to lift household income by $12.5bn in 2020/21.

Federal Budget 2020/21 | Economic Outlook

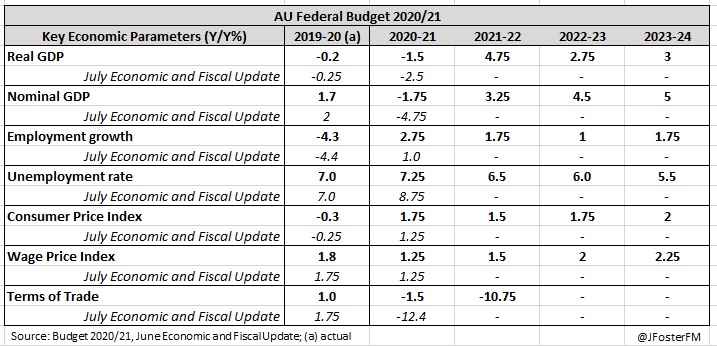

The Government's near-term outlook for the domestic economy has been upgraded since July's update. The expected contraction in GDP growth in 2020/21 has been reduced from -2.5% to -1.5%, which largely reflects a stronger starting point following positive signs in the recovery towards the end of the first half of this year. It is, however, a time of significant adjustment as net overseas migration as a long-running support of economic growth falls away contracting by 72k in 2020/21 due to the impact of the international travel restrictions. On the assumption that Victoria's shutdown eases in line with its roadmap for reopening, conditions across all states and territories are seen to converge allowing most of the current border restrictions to be rolled back by the end of this year, except for a delayed easing in Western Australia.

Assisted by improving dynamics offshore as the recovery in the global economy gains traction - China notably advancing by 8% next year - a rebound of 4.75% in Australian GDP is projected to come through in 2020/21. The major assumptions around the virus here are that a national vaccine program is available by the end of 2021 and that outbreaks remain localised and contained. As to the detail of this rebound, it is very much led by domestic demand. Household consumption growth swings from -1.5% in 2020/21 to 7% in 2021/22 assisted by stimulus measures and an improving labour market, while business investment turns from a 9.5% drag in 2020/21 to growth of 6% in 2021/22 in response to the asset write-off expansion and loss carry-backs announced in this budget. Despite weaker population growth dynamics, residential construction activity is also forecast to pick in 2021/22 rising by 7% on the back of measures such as the HomeBuilder scheme and monetary stimulus from an 11% fall in 2020/21. The Australian economy is then assumed to normalise from 2022/23 onwards with GDP growth advancing at an around trend pace.

With the focus of this budget being on repairing the labour market, the peak in the unemployment rate is expected to be 8% in Q4 of this year ahead of improving over the forward estimates period to reflect the projected growth profile of the economy. This improvement is only expected to be gradual with the unemployment rate expected to take until mid-2022 to ease to 6.5% and decline modestly thereafter. The labour market faces headwinds from the tapering of income support measures ahead of the March 2021 end date for JobKeeper and more Australians returning to the labour force as restrictions are eased further.

Federal Budget 2020/21 | Summary

The Federal Government's 2020/21 Budget extends on earlier policy announcements to provide significant fiscal support following the COVID-19 shock. The focus is around providing incentives for businesses to hire and invest and in boosting household incomes by bringing previously legislated tax cuts through 2 years earlier than planned. The Budget made no changes to the proposed end dates for the JobKeeper policy (March 28, 2021) and enhanced JobSeeker payments (31 December 2020), though these programs are highly dependent on how the economy evolves and the Government has previously shown a willingness to make adjustments as necessary. A clear risk is that these measures, after recently being tapered, do not get extended and if that were to be the case, that would likely have implications for the pace of the recovery. For the economic outlook more generally, the key factor remains the path of the virus. Maintaining effective testing and track and trace measures are key to containing outbreaks that would otherwise restrict the ability of the economy to reopen further.

Link to Budget 2020/21 here