A key speech from RBA Governor Philip Lowe at the AFR Business Summit was the highlight of events in Australia this week. With the domestic economic recovery continuing to gather pace and the outlook globally strengthening, Governor Lowe was clear in emphasising that the RBA does not share the expectation that has been building in markets that policy tightening is on the horizon. For the RBA, something much more than a recovery will be required to justify withdrawing support from its policy settings. At the centre of its thinking is a labour market that remains a long way from where it needs to be to drive faster rates of wages growth that will be able to sustain a pace of inflation that is consistent with the 2-3% target band.

In the RBA's assessment, a tight labour market consistent with its full employment objective could well require the unemployment rate to fall towards the low 4% range, which in turn would help drive wages growth above a 3% annual pace. As it currently stands, the RBA does not expect such conditions to materialise before the year 2024. While inflation is expected to spike above the upper 3% band in the June quarter, it is clear that the RBA will be interpreting this as transitory and will not prompt a shift in policy settings. The main conjecture remains around the future of the 3-year yield target and specifically whether or not the current April 2024 bond that is the focus of the policy shifts further out to the November 2024 bond later this year. Governor Lowe reiterated previous communications in noting that this decision will be informed as more data come to hand on the economic recovery and the labour market.

While the consensus in the market appears to be that the shift to the November 2024 will not occur, there continues to be reason to think that it will. Consider that the RBA's forecasts have its full employment and inflation objectives remaining elusive out to at least mid-2023, while the RBA has also been more dovish than markets have been expecting since it launched its quantitive easing program last November. Aside from a tighter labour market and stronger wages growth, Governor Lowe also emphasised the importance of business investment picking up to support a more durable economic recovery. There was a bright spot in the December quarter with business investment rising by 2.6% on the back of strong equipment spending, though a period of sustained and broad-based strength is needed to boost the nation's productive capacity in a post-pandemic economy.

But there were signs of optimism on this front in this week's NAB Business Survey with the confidence (+16 from +12) and conditions (+15 from +9) readings advancing to multi-year highs in February. Additionally, capacity utilisation lifted from 81.1% to 81.8% to surpass its pre-pandemic level having recovered by 9.7ppts from its April nadir. With the measure now sitting above its long-run average, the outlook for business investment is looking more positive than it has for some time. The Westpac-Melbourne Institute index in March showed consumer sentiment had strengthened by a further 2.5%, returning it to its level from December at around decade highs. In a robust report, forward-looking assessments of economic conditions on a 12 month (3.7%) and 5-year outlook (2.3%) improved and expectations for unemployment eased (-2.1%). On the housing market, there were signs that the strong conditions were having varying effects with house price expectations continuing to advance (3.1%) as views on whether it was a good time to purchase a dwelling were pulling back (-3.6%).

— — —

Moving offshore, the mood in markets around optimism for the global economy was summarised in the OECD's latest Economic Outlook report which showed marked upgrades to growth estimates for 2021. Compared with its forecast from December, global growth this year has been revised up by 1.4ppts to an expected 5.6%, driven largely by a stunning 3.3ppt boost expected to come through in the US that would see growth there accelerate by 6.5% through the year. The key factors behind the much stronger outlook in the US are the vaccine rollout that is gathering pace and the tailwinds of the $1.9tn fiscal stimulus package that was signed into law by President Biden this week. With the package now finalised, US households are in line to receive stimulus cheques of $1.4k, which will be available to individuals with incomes up to $75k before phasing out to zero for incomes above $80k, while for couples the tapering occurs between the $150-160k band. This adds to the $600 cheques received by households at the start of the year and will be key in driving consumption spending when the economy is able to open up more widely.

The Federal Reserve's policy-setting committee will outline its updated assessment of the outlook at next week's meeting; back in December, the median estimate was for GDP growth of 4.2% in 2021, so a sizeable upgrade is likely to be unveiled. There will be a continued focus in the markets on the Committee's views on inflation, with its preferred core PCE measure currently not seen returning to its 2% goal until 2023, while it has then expressed it will tolerate a period of overshoot to make up for a run of earlier misses before the pandemic had emerged. Many market participants foresee a faster lift in inflation given the reopening story and the fiscal boost and expect the Fed's guidance will be tested earlier. However, for the time being, inflation is yet to show up in the data with headline CPI this week coming in as expected at 1.7%yr in February and the underlying rate (excluding food and energy) easing below consensus to 1.3%yr (see chart below). There is little debate that inflation measures will spike from March as the base of comparison in the annual calculation shifts to when the pandemic was just emerging, which coincided with large price level declines, but it's the durability of the increase that is at the centre of the debate with the Fed inclined to view this as transitory on the basis of the damage that has occurred in the labour market.

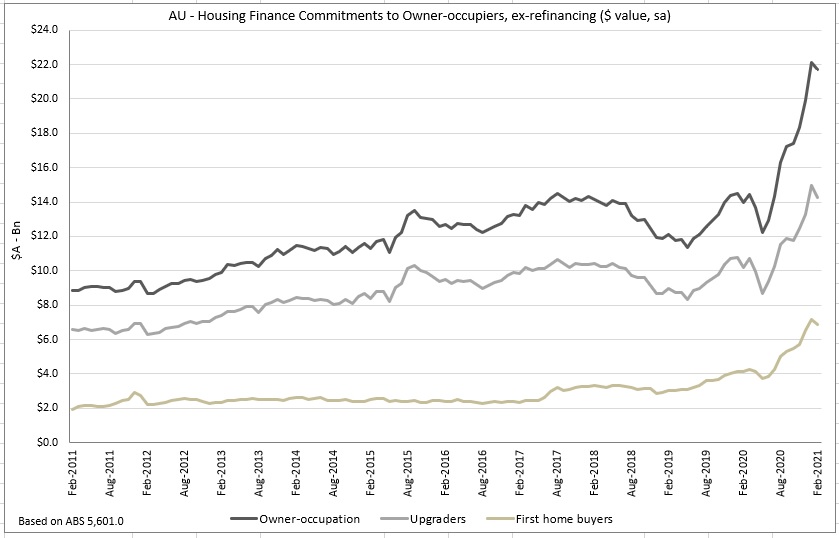

Chart of the week

The optimism around the US is in broad contrast to Europe where the vaccine rollout has been slower leading to containment measures remaining in place for longer, while the €750bn EU fiscal recovery package has yet to come into operation. For 2021, the OECD anticipates GDP growth in the euro area of 3.9%, which is an upgrade of only 0.3ppt from December. Meanwhile, the updated ECB staff projections released this week showed a similar expectation, with growth for 2021 nudged up 0.1ppt to 4.0% for 2021. At its meeting on Thursday, the ECB's Governing Council left monetary policy settings unchanged but signaled that purchases under its PEPP program would be frontloaded next quarter "at a significantly higher pace than during the first months of this year". The decision comes after the recent rise in global bond yields and strength in the single currency, both of which pose risks to the Governing Council's desire to "preserve favourable financing conditions". The precise reaction function as to what constitutes those conditions becoming unfavourable appears to have been made nebulous by design to ensure the ECB retains the flexibility to make interventions as it deems necessary, but President Christine Lagarde in the post-meeting press conference reiterated these assessments will take into consideration "risk-free interest rates and sovereign yields to corporate bond yields and bank credit conditions". It has also been left unclear just how much PEPP purchases could rise, the weekly average for 2021 has been around $13.9bn, though all the ECB would have been interested in was the reaction in the bond markets, and it was unambiguously positive with yields across the continent declining in response.

Also of interest out of this latest ECB meeting was the shift in the Governing Council's assessment of the risks to its growth outlook, which it now generally sees as "more balanced" as opposed to "tilted to the downside but less pronounced" previously, though it did concede that for the near term at least "downside risks remain". Meanwhile, in terms of inflation, much like the indications from the Fed and RBA, President Lagarde said that the ECB will be looking through any upcoming spikes in CPI readings due to the presence of pandemic-related price effects. As such, the ECB retains a subdued profile for the inflation outlook. For 2021, the forecast has lifted to 1.5% from 1.0%, though that still leaves it well short of the ECB's target of below, but close to, 2%, and it is then expected to ease back to 1.2% in 2022 (+0.1ppt) before ending 2023 at 1.4% (unchanged).