Australian private sector capital expenditure came in softer than expected falling by 0.3% in the June quarter. Capex stalled over the first half of 2022, but forward looking investment plans were upgraded and point to the momentum being regained. This investment will be needed to help resolve the capacity pressures firms report.

CapEx — Q2 | By the numbers

- Private sector capex declined by 0.3% in the June quarter to $33.9bn (2.0%Y/Y), well below expectations for a 1% rise, though revisions saw capex in Q1 lifted to a 0.4% increase from -0.3% reported initially.

- Equipment, plant and machinery capex lifted by 2.1%q/q to $16.7bn, to be up by 3.2% through the year.

- Buildings and structures capex contracted by 2.5% in the quarter to $17.2bn, resulting in year-ended growth falling to 1% from 8.3% in Q1.

- Firms' 3rd estimate of capex plans for 2022/23 was upgraded by 11.7% to $146.4bn, on track for a 14.7% rise compared to 2021/22.

- Realised capex in 2021/22 came in at $142.4bn, an increase of 13.3% on capex in 2020/21.

CapEx — Q2 | The details

June quarter capital expenditure (chain volume terms) was soft declining by 0.3% to be broadly flat (0.1%) over the first half of the year. The economic recovery from the pandemic generated an upswing in capex, but this momentum has stalled, potentially due to supply constraints and inflationary pressures while uncertainty around global developments such as the war in Ukraine and China's Covid response could also be contributing.

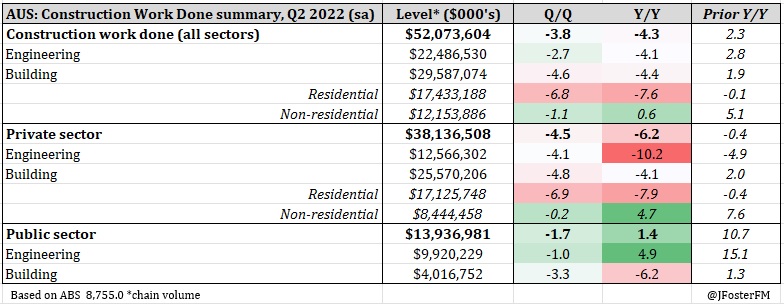

Equipment spending advanced by 2.1%, its strongest quarterly rise since the start of 2021 on the back of increases in the non-mining (1.2%) and mining sectors (6.2%). This was offset by a 2.5% fall in building and structures capex, detail that is in line with the weak construction activity data reported yesterday (see here). Capacity pressures in the construction sector and wet weather likely drove this decline, with weakness coming through in both the non-mining (-2.2%) and mining sectors (-2.9%).

Capex by the non-mining sector has stalled over recent quarters after earlier recovering to pre-pandemic levels of investment. That recovery was driven by equipment spending, currently 6.9% higher than at Q4 2019, on the back of federal government tax concessions, accommodative financing conditions and the broader economic momentum. Lagging well behind has been building and structures investment (-6.9% vs Q4 2019). Projects that were deferred during the pandemic appear to remain on the backburner, not helped by the supply pressures and cost increases in the construction sector.

Mining sector capex is around 10% higher than a year ago, though despite very elevated commodity prices, reporting suggests that much of this has been to sustain rather than increase output.

Turning to investment intentions, firms lifted their 3rd estimate of capex plans for 2022/23 to $146.4bn from $131.1bn forecast 3 months ago. That represents an upgrade of 11.7%, a little stronger than the historical average increase between estimates 2 and 3. Compared to estimate 3 last year, the current figure implies capex is on track to rise by around 15% year to year, though note these are nominal estimates and hence include inflationary effects. Overall, the 3rd estimate was its highest since 2014/15.

Non-mining sector capex plans were upgraded by 14.4% vs estimate 2 to $101.7bn, pointing to a 15.8% year-to-year rise. Spending intentions on equipment (18.9%) and buildings and structures (10.6%) have lifted from 3 months ago. A smaller upgrade of 5.9% was nominated by the mining sector for estimate 3 to $44.7bn, running 12.4% higher year-to-year.

CapEx — Q2 | Insights

A disappointing outcome from quarterly capex confirming that momentum stalled over the first half of 2022. Firms are facing significant capacity pressures, not only from labour shortages but also following a period of underinvestment through the pandemic. Capex did rebound in line with the economic recovery, but more will be needed if these capacity pressures are to be remedied. Upgrades to forward-looking investment plans for 2022/23 are a positive in that respect, though the reported strength is partly boosted by inflation. The question is whether this intended (and needed) investment holds up given a deteriorating global economic outlook.