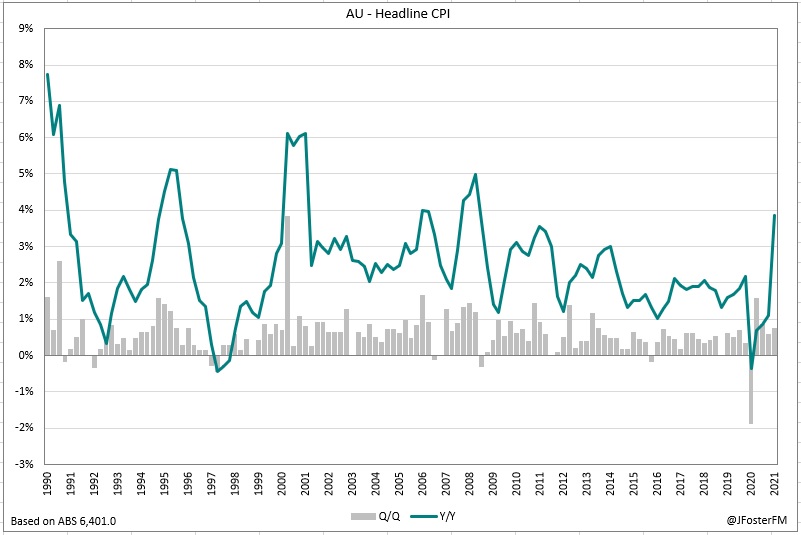

Australian inflation printed a touch stronger than expected this week with the headline CPI measure rising by 0.8% in the June quarter (vs 0.7% expected). Reflecting the reversal of many cost-saving measures introduced by governments to support households at the onset of the COVID — free child care being the big-ticket item — and fuel prices rebounding to above pre-pandemic levels, annual CPI lifted by 2.7ppts to 3.8% to be at its highest since 2008 (reviewed here). Added to these base effects were a range of temporary factors. The chart below shows the top ten contributors to Q2's CPI outcome, which includes private health insurance premium rises; supply-side constraints leading to higher prices for fruit, vegetables and meat; strong demand and limited supply driving vehicle prices higher; as well as the unwinding of an electricity rebate in Perth.

Chart of the week

Supporting the view that the rise in headline inflation has a transitory nature, measures of underlying CPI that remove the most volatile price changes, were only modestly higher and remained below the bottom of the RBA's 2-3% target band. Trimmed mean CPI was 0.5% higher in Q2 taking the annual rate off its record low of 1.1% to 1.6%; the weighted median also increased by 0.5%q/q as the year-on-year pace firmed to 1.7% from 1.3%. Overall, the tension between headline inflation at 3.8%Y/Y and underlying inflation at around 1.6%Y/Y will give the RBA confidence that its assessment of the inflation dynamics is correct, meaning that this week's report should have few implications for policy ahead of next week's meeting, particularly with the pandemic situation being far more pressing.

With Sydney's lockdown being tightened and extended until at least the end of August, the RBA's GDP growth forecast for 2021 of 4.75% is likely to take an even larger downgrade in its updated quarterly statement than was the case just a week ago. The path for the unemployment rate will be recalibrated to reflect its faster-than-expected decline, though the GDP downgrade will temper expectations around the outlook. It shapes as increasingly likely that the RBA will have to defer its guidance to commence tapering its QE purchases from early September. As covered last week, another option for the RBA would be to scale up the pace of its purchases, to $6bn/wk from $5bn, though my sense is that the Board will be more likely to land on delaying tapering at this stage. Given the signal announced at the July meeting was that purchases would reduce to $4bn/wk once the second $100bn tranche had been completed, reversing that guidance would in effect ease the overall monetary policy stance as purchases would stay at $5bn beyond early September. But in the current situation, the key anchor of support comes from fiscal policy, making this week's announcements from the federal and NSW state government to increase and expand support for workers and businesses welcome developments.

— — —

Switching the focus offshore, in the mix was increasing risks to the global economic recovery due to the delta strain, the latest Federal Reserve meeting, some key data points and a regulatory crackdown on education and tech names that unsettled Asian equities. While the IMF kept its GDP growth forecasts for this year and next unchanged at 6.0% and 4.9% respectively, the group made offsetting revisions with the outlook for 2021 in advanced economies revised up (to 5.6% from 5.1%) but marked down in emerging and developing economies (from 6.7% to 6.3%) due to increased fiscal stimulus and higher vaccination coverage driving the divergence. As noted by the IMF in its July World Economic Outlook update, the risks to growth prospects were to the downside due to slow vaccination roll-outs in many nations that leave them vulnerable to further outbreaks and mutations of the virus. Another key risk mentioned by the IMF resides around high inflation remaining more persistent than anticipated, which could prompt a tightening in financial conditions if the outlook for monetary policy is abruptly revised by markets.

At the meeting of the Fed's FOMC this week, all policy settings were left unchanged as Chair Jerome Powell continued to deliver a familiar message that still suggests the start of QE tapering remains a little way off. Key to that process is conditions in the labour market, with the FOMC needing to see "substantial further progress" in the recovery before it considers lowering purchase from the current pace of $120bn per month. In the post-meeting press conference, Chair Powell said that there while there were signs that the labour market was "making progress" there was still "some ground to cover" in terms of moving closer towards its maximum employment objective. On the Committee's transitory definition of inflation, Chair Powell said that there had been few signs that price rises driven by supply chain bottlenecks were becoming embedded in forward-looking inflation expectations and as such were unlikely to be permanent. There were, however, signs that these factors are weighing on activity as June quarter real GDP growth missed estimates coming in at 1.6%q/q. On a side note, this outcome now sees US GDP slightly higher than pre-pandemic levels (+0.8%). While the consumption side of the economy remains strong — growth in personal spending lifted by 1.0% in June driven by an increasing rotation back towards services-related areas (1.2%m/m) on the widening reopening — both inventories and residential construction subtracted from output during the quarter, with rising materials costs and labour shortages particular constraints in the latter. This combination of strong consumer demand and supply chain pressures saw the Fed's preferred core PCE inflation measure a little firmer in June at 3.5%Y/Y from 3.4%.

In Europe, data this week confirmed the encouraging progress reported in the soft indicators that the recovery in the continent is back on track from the virus-driven setback it endured over the past two quarters. Growth in real GDP came in stronger than expected advancing by 2.0%q/q (vs 1.5% forecast), though this still left activity around 3% down on pre-pandemic levels. Across the major economies in the bloc, growth in Spain (2.8%q/q) and Italy (2.7%q/q) led the way to more moderate rebounds in Germany (1.5%q/q) and France (0.9%q/q). But with economies now opening up more widely, there aren't the same extent of supply-side pressures as in the US. July's preliminary inflation reading for the euro area moved up from 1.9% to 2.2%Y/Y (vs 2.0% expected), though the core rate slowed from 0.9% to 0.7%Y/Y (as expected). Rounding out the week, further signs that the reopening is taking shape was was seen with the fall in euro area unemployment from 8.0% to 7.7% (vs 7.9% expected).