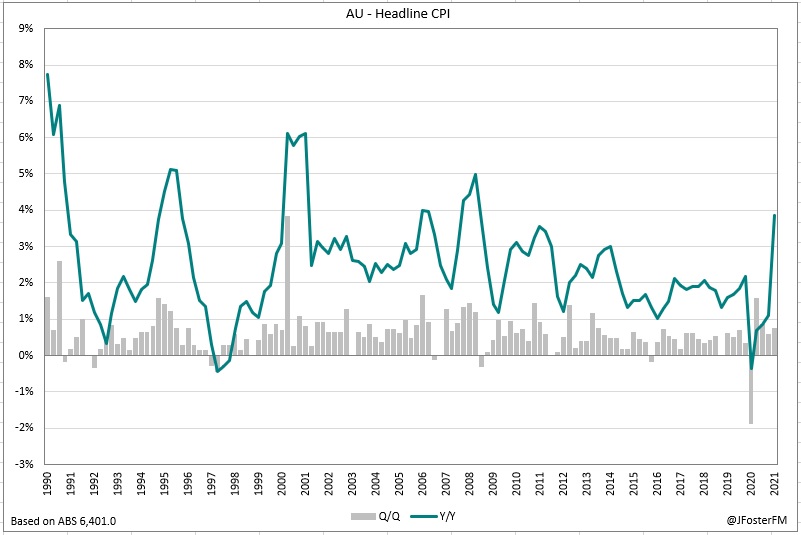

Australia's Consumer Price Index (CPI) accelerated to its fastest since 2008 at 3.8%Y/Y reflecting the reversal of many cost saving measures introduced by governments to support households through the onset of the pandemic. A rebound in fuel prices to above pre-pandemic levels were the other major contributing factor to the increase. But, despite this, the underlying measures of inflation remain below the RBA's target band.

Consumer Price Index — Q2 | By the numbers

- Headline CPI (not seasonally adjusted) printed at 0.8% in the June quarter, coming in ahead of the median estimate of 0.7% and up from 0.6% in Q1. Base effects accelerated annual CPI from 1.1% to 3.8% to be at its highest since Q3 2008. Seasonally adjusted CPI was 0.8%q/q, with the annual pace advancing to 3.7% from 0.9%.

- Details for the underlying measures (measures are seasonally adjusted);

- Trimmed mean came in close to expectations at 0.47%q/q, lifting the annual rate off a record low of 1.13% to 1.63%.

- Weighted median increased by 0.48%q/q as the pace through the year firmed to 1.67% from 1.29%.

Consumer Price Index — Q2 | The details

Australian headline inflation was a touch stronger than markets had anticipated rising by 0.8% in the June quarter and a touch firmer than the 0.6% increase in the previous quarter. Prior to the lockdowns either ongoing or just lifted in some of the nation's capital cities, the domestic economy was opening up more widely and was performing strongly. As a result, fuel prices had rebounded above pre-pandemic levels and many of the cost saving measures introduced by governments to support households through the national lockdown, including free child care services, rent reduction mechanisms and rebates on utilities, had reversed. Thus with price levels in a reopened economy being compared against the depths of the pandemic last year, this saw annual CPI accelerate sharply from 1.1% to 3.8% to be at its fastest in nearly 13 years.

Measures of underlying annual inflation also lifted due to base effects in the June quarter, but both the trimmed mean (1.63%) and weighted median (1.67%) measures remain subdued and are short of the bottom of the RBA's 2-3% target band. The broader CPI ex-volatiles measure lifted more sharply, from 1.36% to 3.11%, as this measure still picks up the effect of the reversal of free child care but removes the impact of higher prices for fuel and fruit and vegetables.

Overall, goods-related inflation (2.0%Y/Y) remained stronger than in services (1.5%Y/Y), though the spread had continued to narrow as consumption patterns were adjusting to the wider reopening.

Turning to analysis of the main CPI groups, the chart below shows the contribution of each of the groups to the quarterly CPI outcome of 0.8%. The largest contribution came from the transport group (0.35ppt), with higher fuel prices making up 0.26ppt of this to account for one-third of the rise in inflation in Q2. Other major influences boosting inflation in the quarter were from food and non-alcoholic beverages (0.11ppt) reflecting higher fruit and vegetable prices (0.14ppt) due to supply constraints from labour shortages and extreme weather events on the east coast. The contribution from the health group (0.12ppt) was driven by medical, dental and hospital services (0.13ppt) as private health insurance premiums increased on April 1. At the other end of the scale, the main item that weighed on quarterly CPI was meals out and takeaway food (-0.05ppt) (this is part of food and non-alcoholic beverages) due to the impact of voucher schemes that were implemented by state governments as a pandemic response measure to support restaurants and cafes in Sydney and Melbourne by subsidising meal costs. Domestic travel (part of recreation and culture) subtracted 0.04ppt from quarterly CPI reflecting the Federal Government's support package that subsidised airfares to selected destinations as well as increased completion from local tourism operators to attract business.

Quarterly and annual price changes (in % terms) for each of the major CPI groups are shown in the chart below.

In terms of annual growth, furnishings, household equipment and services (16.9%yr) was at the top of the pile, which mainly reflects the reversal of the Federal Government's decision to provide all families with free child care services during the national lockdown a year ago. As a result, the child care index was up an extraordinary 2,009% over the year. Meanwhile, strong demand for furniture and furnishings (and other durables) as a result of stay-at-home restrictions drove a 5% price increase for these items over the year.

The transport group lifted by 10.7%Y/Y as fuel prices lifted above pre-pandemic levels to be 27% higher than a year earlier. In Q2 alone, fuel prices were up 6.5% on the wider reopening of the Australian economy, and as highlighted above, this accounted for one-third of the increase in quarterly CPI. Strong demand for new vehicles amid the global semi-conductor shortage led to car prices rising by 7.4% over the year.

The key housing group (accounting for around 24% of the CPI) saw prices lift 0.3% in Q2 but were slightly lower (-0.2%) over the year. Rents nationally were flat in the quarter, while annual growth increased from -1.4% to a flat outcome. The lift in annual growth came as a sharp 1.3% fall in Q2 last year on the back of the introduction of rent reduction mechanisms rolled out of the calculation.

Conditions in rental markets have also varied considerably across the nation with declines in Sydney (-1.5%Y/Y) and Melbourne (-0.8%Y/Y) offset by gains in Perth (3.3%Y/Y), Hobart (2.8%Y/Y), Adelaide (1.8%Y/Y) and Brisbane (1.7%Y/Y).

New dwelling prices were reported as falling by 0.1% in Q2 due to the effect of the Federal Government's HomeBuilder grants, which are reflected as lowering the price of new homes. However, the ABS notes that if the HomeBuilder scheme is excluded, new dwelling prices would have lifted by 1.9% in each of the past two quarters due to higher materials and labour costs.

Meanwhile, household utilities prices were up 1.7% in Q2 as electricity prices lifted by 3.3%. This was driven by the unwinding of a government rebate on electricity in Perth. But rebates are in effect in other states, such that electricity prices would have fallen by 2% in the quarter if the unwind in Perth was excluded.

Inflation across food and non-alcoholic beverages (around 17% of the CPI) lifted by 0.5% in Q2 with the annual pace unchanged at 0.7%. The strongest price rises over the past year have been in beef and veal (13.5%) and fruit (6.0%) due to supply constraints affecting both categories. Higher meat prices are being driven by herds being rebuilt after the end of the drought in early 2020, while a lack of labour supply (pickers) and the impacts of flooding and cyclones lifted fruit prices.

In the recreation and culture group (around 9% of the CPI) prices declined in Q2 (-0.1%), though the annual pace moved up from 1.5% to a 7-year high of 2.5% on a combination of base and reopening effects. While domestic travel costs declined by 1.3% in Q2 reflecting the Federal Government's discounted airfare scheme, international travel was up by 8.6% in the quarter as the travel bubble (which is now suspended) with New Zealand opened up.

For the health group (6% of the CPI), Q2's rise of 1.5% lifted annual growth to 4.8% to its highest in 5½ years. The driving factor this quarter was a 2.4% lift in medical and hospital services that reflected private health insurance premiums rising from April 1.

Price increases across the rest of the CPI groups were subdued in Q2: alcohol and tobacco 0.4%, clothing and footwear 0.4%, financial and insurance services 0.3% and education 0.0%. Meanwhile, the communication group continued to fall (-0.6%) reflecting discounting for phone services.

Consumer Price Index — Q2 | Insights

The inflation data continue to be distorted by policy and pandemic-related factors, but the underlying measures remain short of the RBA's 2% lower target. Thus there is little reason to think that the surge in headline inflation is anything but transitory and will therefore be of little consequence to policymakers. Many economies offshore have seen price rises accentuated by supply constraints as they have reopened, though these pressures have been less prevalent in Australia.