The latest data on prices in the US helped spark a modest relief rally at the front end of the yield curve; however, soft Treasury auctions were influential in driving the curve steeper over the week - a headwind to equities. In Australia, stronger-than-expected inflation data reinvigorated pricing for an extended RBA hold, lifting domestic bond yields and supporting the AUD.

Key US inflation data was in line with expectations in April, avoiding an upside surprise but still leaving the Fed well adrift from its 2% target. The core PCE deflator lifted 0.2% month-on-month (the slowest increase since December) as the annual pace printed at an unchanged 2.8%. This was an improved reading compared to recent months that reflected inflationary pressures regaining momentum in the early part of the year. Accordingly, the 3-month (3.5%) and 6-month (3.2%) annualised rates are elevated to the annual pace, suggesting the Fed will need to wait for more reports similar to April before it will gain the confidence it needs to start cutting rates.

Preliminary inflation estimates for May in the euro area surprised on the upside of expectations ahead of next week's ECB meeting. The ECB has effectively pre-committed to a rate cut, so the messaging around the policy outlook will be the main focus in light of the latest inflation data with markets pricing in 2-3 rate cuts by year-end. Headline inflation increased from 2.4% to 2.6%yr (vs 2.5% expected) and the core rate was also firmer at 2.9%yr (vs 2.7%) from 2.7% in April. Higher inflation readings were driven by a lift in services inflation (3.7% to 4.1%yr), and this could form the basis of a cautious tone from the ECB regarding rate cuts beyond June.

An uptick in Australian CPI inflation to 3.6% in April from 3.5% in March defied expectations for a softer reading (3.4%). This was accompanied by a firming in the trimmed mean (or core) measure from 4% to 4.1% (see here for a full review of the CPI report). Rates markets repriced on the release to reflect expectations for a lengthy hold from the RBA until the second half of next year. However, there is scope for a dovish reappraisal next week with the Q1 GDP growth figures due on Wednesday. My detailed preview of the National Accounts (see here) outlines that a continuation of subdued growth in early 2024 is likely as households remain under pressure from the cost of living and increased mortgage repayments. Those dynamics were reaffirmed by a weaker-than-expected 0.1% rise in retail sales in April (see here).

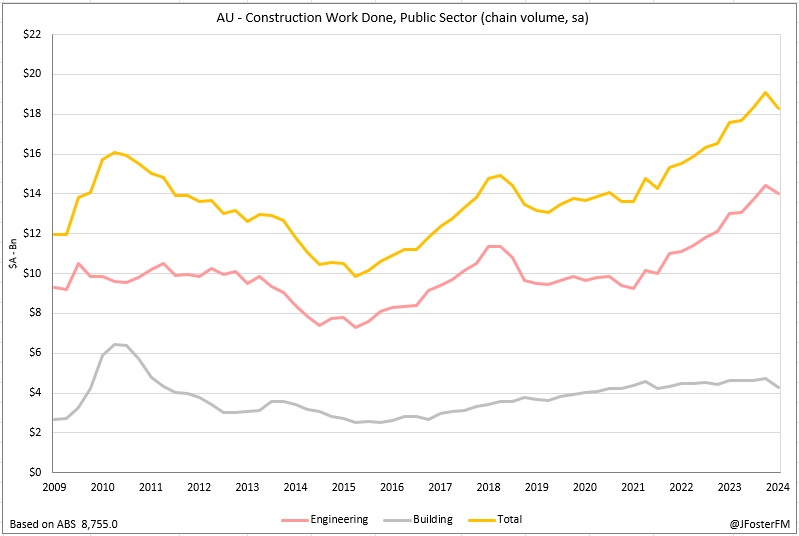

Construction activity data contracted by 2.9% in Q1 (see here) as the detail indicated home building weighed further on economic growth. Engineering activity, mostly related to infrastructure, (-2.7%) and non-residential building (-7%) - components that have bolstered growth in recent quarters - saw output slow in Q1. Remaining on the construction theme, dwelling approvals held around 12-year lows on the back of a modest (-0.3%) decline in April (see here). At this stage, business investment shapes as the main driver of growth in Q1. Strength in equipment investment (3.3%) led private sector capital expenditure to advance by 1% in the March quarter (see here). Firms' forward-looking capex plans appeared broadly consistent with a constructive outlook for investment. Plans for 2024/25 were upgraded by 6.8% to $155bn, an 11-year high.