Australia's December quarter national accounts are due to be published by the ABS today (3/3) at 11:30am (AEDT), with GDP growth expected to have advanced by 2.5% in Q4. The economic recovery from the covid-19 recession started at pace in the September quarter with real GDP rebounding by 3.3%, moderating the contraction through the year to -3.8% from -6.4%. However, with the state of Victoria enduring a second shutdown after a surge in virus cases over the winter this weighed considerably on national output in the quarter.

Over the December quarter, low virus case numbers led to Victoria's reopening and more restrictions being rolled back across the nation, ensuring a continuation in the momentum of the recovery. Reflecting this and a reduction in precautionary behaviour, indicators of mobility improved to their highest levels since the initial phase of the pandemic earlier in the year.

The recovery in the labour market had also gathered pace, with employment ending the year 0.7% below its pre-pandemic level after it collapsed by 6.7% at the peak of the crisis, while hours worked had rebounded sharply from its 8.8% contraction through the first half of the year rising by 7.3% over the second half. Notably, the reopening in Victoria has enabled it to catch up with the progress achieved in the other states.

The wider reopening, improving labour market conditions, strengthened balance sheets from fiscal and monetary policy stimulus measures and rising sentiment all contributed to ensuring household spending continued to drive the economic recovery in the quarter.

Momentum was also building in the housing market, with policy support from low rates and the Federal Government's HomeBuilder scheme driving approvals for detached house construction to record high levels and lifting approvals for alteration work sharply. Established housing market conditions were also strengthening with national property prices now rising again after several months of modest declines during the middle of the year.

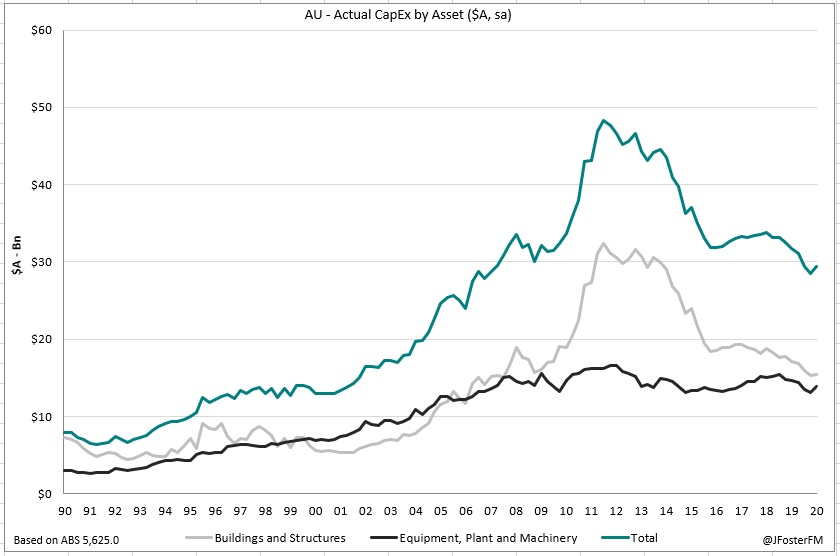

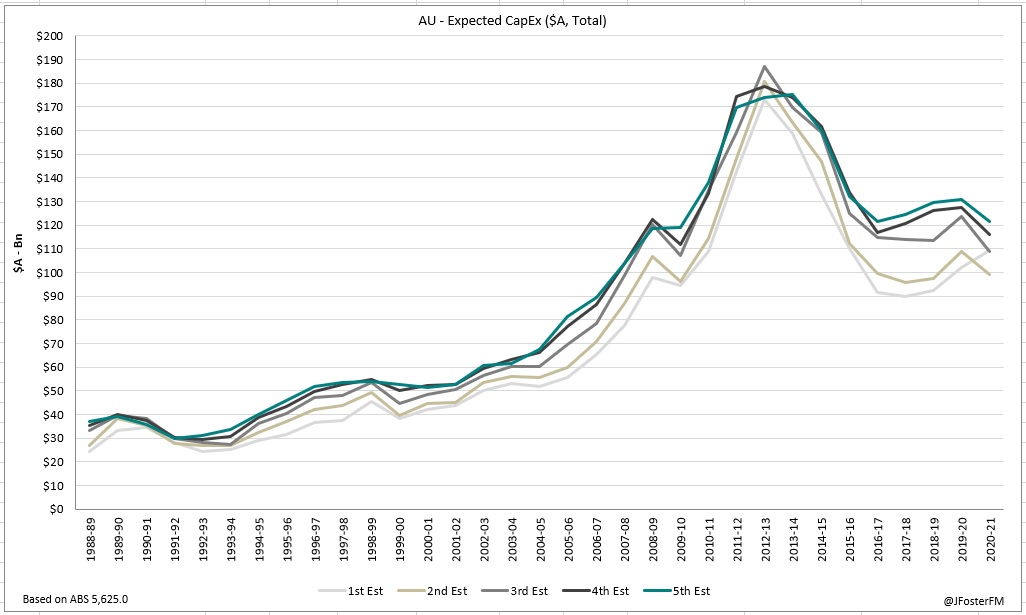

Uncertainty and a focus on preserving liquidity has continued to weigh on business investment, though forward-looking capital expenditure plans are now more constructive than earlier in the pandemic. Reflective of reopening dynamics, import volumes lifted sharply in the quarter on higher demand for consumption and capital goods, but services trade remained heavily restricted by the international border controls.

As it stands | National Accounts — GDP

The reopening of the Australian economy enabled the recovery to start taking shape in the September quarter with real GDP rebounding by 3.3% after contracting by 7.3% over the first half of the year, though this still left Australian GDP 4.2% lower than its pre-pandemic level. In economies offshore, global activity was being switched on again after earlier shutdowns, in turn generating tailwinds for the domestic recovery, most notably through elevated commodity prices. In the September quarter, GDP across OECD economies surged back by 9.2%, but despite very strong rebounds in the US (7.5%), euro area (12.4%) and UK (16.0%), most economies remained well short of their end 2019 levels. A notable exception has been China with GDP growth in Q3 (3.0%) extending its reopening-driven surge from the previous quarter (11.6%).

With the easing of restrictions enabling a much broader range of opportunities to engage in activity and spend, a consumption-led recovery drove the Australian economy in the September quarter. After collapsing by 13.6% over the first half of the year, household consumption saw a robust but partial rebound rising by 7.9% in Q3, with Victoria's return to shutdown preventing a stronger outturn. Services consumption led the way lifting by 9.8%q/q reflecting the reopening of hospitality venues and the resumption of participation in sports and leisure activities. Meanwhile, goods consumption advanced by 5.2%, elevating it above its pre-pandemic level as spending in areas still affected by restrictions (such as overseas travel) was diverted into in-home spending, clothing and footwear and new vehicles. With real disposable incomes rising by 3.3% in the quarter, this rebound in consumption was partly funded by a drawdown in the saving rate, which declined modestly from 22.1% to a still very elevated 18.9%.

Activity in residential construction posted its first quarterly rise in more than 2 years (0.6%) as alteration worked lifted sharply (5.1%) in response to the Federal Government's HomeBuilder scheme, overcoming a 2.1% contraction in new home building. Business investment continued to be scaled back, falling a further 4.1% in Q3 with pandemic-related uncertainty limiting the visibility over the outlook for demand. Net exports weighed significantly on activity in the quarter subtracting 1.9ppts from real GDP growth. Imports lifted sharply (6.5%) as domestic demand conditions strengthened in response to the reopening, though exports (-3.2%) were weighed by weakness in the global economy and the closure of the international border hitting the tourism, education and transports sectors.

Key dynamics in Q4 | National Accounts — GDP

Household consumption — Australian households continued to drive the recovery forward over the quarter as the state of Victoria emerged from its shutdown; retail sales elevated very sharply in November corresponding with the Black Friday promotional period. The strength in household spending reflects eased social distancing and mobility restrictions, a broadening recovery in the labour market, improved consumer sentiment and the effects of fiscal and monetary stimulus that have supported incomes and bolstered balance sheets.

Dwelling investment — Entrenched weakness in the residential construction cycle prior to the pandemic has turned higher on the tailwinds from a range of policy stimulus measures, most notably the Federal Government's HomeBuilder scheme. Residential construction activity posted its strongest quarterly outturn in 2½ years (2.7%) as alteration work advanced by a further 3.6% and new home building lifted 2.6%, led by the detached segment (3.4%).

Business investment — Firms' investment plans have been crunched under the weight of the uncertainty associated with the pandemic and an earlier focus on capital preservation. But some bright spots came through in Q4 with private sector capital expenditure rising by 3.0%, led by equipment spending (5.7%) in response to measures included in last year's Federal Budget that have enhanced tax incentives for firms to bring forward investment.

Public demand — Consumption spending advanced by 0.8% in Q4 on continued pandemic-related measures. This combined with a rise in underlying investment of 2.3% in the quarter to drive public demand up by 1.1% and contribute 0.3ppt to activity in Q4.

Inventories — After subtracting substantially from activity over the first half of 2020, inventories stabilised over the second half. Inventories may add slightly to GDP growth contributing 0.1ppt in Q4.

Net exports — Import volumes lifted by 4.9% in Q4 on strength in consumption and capital goods as demand conditions rebounded on the reopening, outpacing a 3.8% rise exports that was led by the rural sector. Net exports will subtract 0.1ppt from Q4 GDP growth.