The ABS is scheduled to publish Australia's national accounts for the December quarter today at 11:30am (AEDT). Estimates indicate the Australian economy expanded by around 0.8% in the quarter and 2.7% through the year.

Offshore, the economic backdrop remained a challenging one into year-end. Inflation was still printing at elevated rates, though it was likely past the peaks following falls in energy and goods prices. Growth had been resilient throughout much of 2022 to headwinds from cost-of-living pressures, rising interest rates and weak sentiment but had slowed further in many economies in the final quarter of the year. The return of Covid restrictions hampered growth in China.

In Australia, with headline inflation picking up to its highest since 1990 at 7.8% over the year to Q4, the RBA continued to hike rates. Rising cost-of-living pressures and rate hikes weighed heavily on consumer sentiment, which fell back to the lows at the outset of the pandemic.

While household spending has slowed, it was still broadly resilient as incomes were being supported by a very strong labour market. Strong employment growth in the quarter drove the unemployment rate down to 3.4%, its lowest since the 1970s, while a broader measure of underutilisation in the labour market declined to a 40-year low.

Under the weight of rising prices and with consumption rotating back to services, retail volumes contracted (-0.2%) in the quarter. However, retail sales had risen strongly in November as households brought forward their Christmas spending to take advantage of Black Friday discounting. Spending on services remained solid, continuing to be supported by the post-pandemic reopening of the sector.

The RBA's tightening cycle was having a major effect on the housing market. Housing prices nationwide were down by around 9% from their peak in April 2022; the Sydney market driving the correction where the peak-to-trough fall has been around 14%. Residential construction was rebounding from a disrupted first half in 2022, though capacity constraints were still contributing to lengthy building times.

Services trade remained robust responding to the reopening of the international borders earlier in the year. A rising inflow of tourists and students into Australia was boosting export earnings, while overseas travel and related spending had driven a very strong rebound in imports. National income continued to be supported by elevated commodity prices, though they had declined from their peaks in the middle of the year.

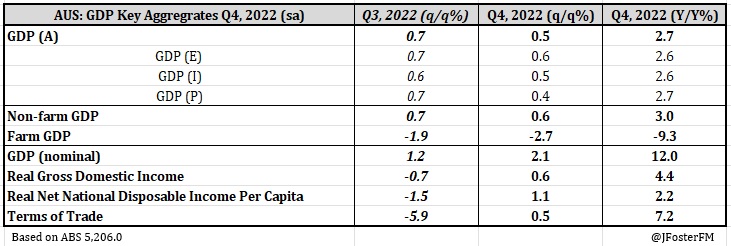

As it stands | National Accounts — GDP

In the September quarter, the Australian economy expanded by 0.6% as growth over the year lifted from 3.2% to 5.9%. Real GDP was now more than 6% above its pre-pandemic level at the end of 2019.

The ongoing rebound in services spending from the pandemic supported a solid rise in household consumption (1.1%), driving overall economic growth in the quarter. Spending patterns were continuing to rotate from goods (0.3%) to services (1.7%) as the effects of the pandemic were dissipating, led by discretionary services in tourism, hospitality and entertainment. Consumption continued to be robust despite household real incomes falling over the past year due to cost-of-living pressures. As a result, there was a further reduction in the household saving ratio in Q3 to 6.9%, falling from 12.9% at the end of 2021.

An easing of materials and labour shortages in the construction sector and fewer weather-related disruptions in Q3 supported a rebound in home building and non-residential construction activity. Imports continued to rise reflecting strong domestic demand conditions, the rebound in overseas travel and the gradual resolution of pressures that have hampered global supply chains. Inventory rebuilding had occured alongside this, adding strongly to growth over the past year.

Exports still remained below their pre-pandemic level but had picked up over the past two quarters as the volume of international tourists and students arriving in Australia continued to recover. Commodity prices declined from their highs earlier in the year but still remained at elevated levels. This saw the terms of trade easing from record highs in Q3.

Key dynamics in Q4 | National Accounts — GDP

Household consumption — Remained resilient to the headwinds faced by households from falling real incomes and weak sentiment as the post-Covid rebound in services spending continued. Retail sales contracted in the quarter, though demand was very robust over the Black Friday sales period.

Dwelling investment — Private sector home building advanced further in the quarter, rebounding from weather-related and supply constraints in the first half of the year. Alterations continued to decline as the large pipeline of renovations was being worked through.

Business investment — Non-residential construction appears to have rebounded in the second half of 2022 as delays caused by adverse weather and capacity constraints eased up. However, equipment spending slowed compared to the first half of the year.

Public demand — Was little more than flat in Q4 rising by 0.3%. Government spending advanced (0.6%) but investment declined (-1%).

Inventories — Weighed on activity in the quarter as inventory levels declined following a strong rebuild over the past year coming out of the pandemic.

Net exports — Set to contribute 1.1ppts to quarterly GDP. Export volumes lifted by 1.1% on the back of the post-pandemic recovery in services. Imports fell by 4.3% indicating domestic demand conditions may have softened.

.jpg)