Australian wages growth increased at a slower-than-expected pace in the December quarter but still reached a 10-year high at 3.3% over the year. Wage pressures have risen over the past year as the labour market has tightened and as inflation has elevated. However, the increase in wages growth has been kept in check by the nature of Australia's wage-setting processes and with labour force participation rising to record highs coming out of the pandemic.

Wage Price Index — Q4 | By the numbers

- The headline WPI (total hourly rates of pay ex-bonuses) increased by 0.8% in the quarter (vs 1% expected), easing back from Q3's 1.1% rise. Annual growth in the index firmed from 3.2% to 3.3% (vs 3.5%).

- Private sector wages lifted by 0.9% quarter-on-quarter to be 3.6% higher over the year, a decade high.

- Wages growth in the public sector increased by 0.7% for the quarter, lifting the annual pace from 2.4% to 2.5%.

Wage Price Index — Q4 | The details

Wages growth eased back to a 0.8% rise in the December quarter after much of the flow-through from the national minimum wage increase boosted the increase reported in Q3 (1.1%). However, the ABS noted in today's release that this was still the fastest rise in the WPI for a December quarter in the last decade.

The WPI that includes bonuses and other one-off payments moderated to a 0.8% rise after spiking in Q3 (1.4%) following end-of-financial year reviews. According to RBA liaison, many firms have turned to bonuses and other payments to retain staff as competition for labour has intensified and to assist with the rising cost of living rather than paying higher base wages. In year-ended terms, wages growth inclusive of bonuses (3.5%) is only slightly stronger than the headline measure (3.3%).

The private sector has been largely driving the rise in wage pressures. In the December quarter, private sector wages lifted by 0.8% to 3.6% over the year, its fastest since Q3 2012.

The ABS reported that 23% of private sector jobs received a pay rise in Q4, only slightly higher than in Q4 2021 (21%). However, the average pay increase for these jobs was now 4% compared to 2.8% a year ago, highlighting that labour has become more expensive as conditions in the labour market have tightened and as inflation has risen.

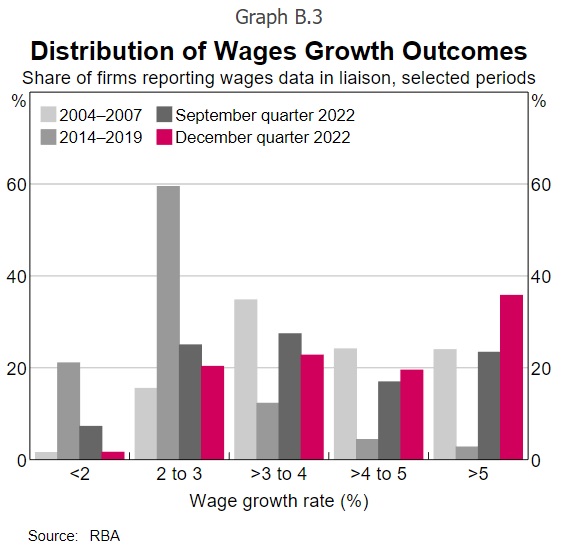

For comparison, the RBA's liaison program - seemingly an increasingly important input into the Board's monetary policy decisions - reports most firms are paying wage increases of between 2-3% and 4-5%, a broader distribution than in the years prior to the pandemic. Meanwhile, a much larger share of firms in the liaison program are paying wage increases above 5% compared to historical experiences.

Source: RBA February Statement on Monetary Policy

In the public sector, wages growth continues to move slowly (2.5%Y/Y) and remains no higher than it was in the pre-pandemic labour market. That being said, reviews of state government wage policies for higher pay increases should flow through over the coming quarters.

My updated estimates (using the industry-level data) have wages growth running strongest in the goods-related (3.8%) and business services (3.6%) sectors. The goods-related sector includes industries such as construction, manufacturing and transport (which includes travel) where labour shortages have been major constraints coming out of the pandemic. Wages growth in business services has risen amid strong competition for labour, with many people switching jobs over the past couple of years. In household services, wages growth has been more moderate (3%), though there have been stronger rises in the pandemic-affected industries including arts and recreation (4%), accommodation and food (3.5%) and other services (3.7%).

Wage Price Index — Q4 | Insights

Today's report comes in contrast to the recent step up in hawkish communication from the RBA. A 3.3% pace of wages growth is not inconsistent with the Bank's inflation target band of 2-3%. Clearly, the RBA is leaning on the side of caution given the strength in the labour market. However, even there, wages growth is much softer than historical experiences suggest it should be for the degree of tightness seen currently. Two factors are relevant here. Firstly, wages in Australia tend to adjust fairly slowly to changes in underlying labour market conditions due to annual minimum wage reviews and enterprise agreements that can be years long. Secondly, labour force participation lifted to record highs as the pandemic dissipated, which is a vastly different situation to what has occured in the US and UK for example, where a constrained labour supply has accelerated upward pressure on wages. Overall, wages growth does not look to be responding to the inflationary backdrop at an alarming pace that risks a deanchoring of inflation expectations.