Australian housing finance commitments contracted by 1.4% in September, posting back-to-back declines for the first time since the outset of the pandemic. Victoria's lockdown weighed heavily on owner-occupier commitments, which nationally were down 2.7%m/m. In a repeat of what was seen in August, investor commitments were resilient to the broader weakness rising by 1.4%m/m. After surging to a record high level earlier in the year, housing finance commitments are now retracing as stimulus measures have expired or are getting close to running their course, while affordability concerns due to rising house prices and some modest tightening of policy settings will also have their say.

Housing Finance — September | By the numbers

- Housing finance commitments ($ value, ex-refinancing) were down 1.4% for the month in September to $30.3bn, coming off the back of August's 4.3% fall. Annual growth slowed further, from 47.4% to 35.5%.

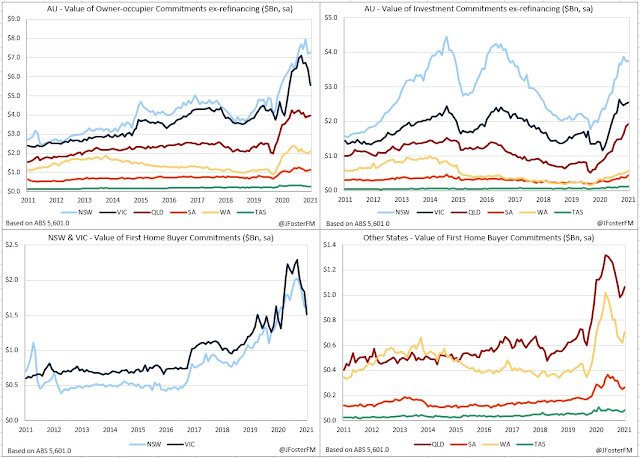

- Owner-occupier commitments declined by 2.7%m/m (prior: -6.6%m/m) to $20.7bn (20.8%yr from 33.5%)

- Investment commitments increased by 1.4%m/m (prior: 1.5%m/m) to $9.6bn, with annual growth standing at 83.2% from 92.2% previously.

- Total refinancing activity contracted sharply, down 9.1% for the month (prior: 3.2%m/m) for its largest decline since last November, to around $16.2bn. That lowered annual growth to 24.7% from 58.1%.

Housing Finance — September | The details

Owner-occupier commitments were down 2.7% for the month, a more moderate decline than seen in August (-6.6%). This was driven by a 12.7% fall in Victoria while Tasmania saw a small decline (-1.3%). Within the segment, there were broad-based falls: upgraders -2.4%, first home buyers -1.9% and from the construction-related area -5.4% with the earlier boost from the HomeBuilder scheme continuing to unwind.

The weakness in commitments was also reflected in the approvals data, shown in the charts below. Construction-related approvals are falling at a faster rate than for upgraders with the HomeBuilder effect passing through. First home buyer approvals have retraced to mid-2020 levels on the withdrawal of incentives to that group, with affordability concerns likely also a contributor.

Lending to the investor segment defied the broader weakness, lifting by 1.4% in the month. While still expanding, the pace has slowed markedly over the past 4 months from the surge seen earlier in the year.

Refinancing activity fell sharply in the month, down 9.1% on an aggregated basis for its steepest decline since November 2020. But it must be said that refinancing hit a record high in the prior month and is still at very elevated levels. Refinancing to owner-occupiers fell 9.6%m/m and was down by 8.4%m/m to investors.

Stepping back, the quarterly picture showed a sharp divergence between owner-occupiers and investors, though the effects of the lockdowns are a complicating factor in trying to reach conclusions. Total commitments were down by 2.6% in Q3, weighed by the owner-occupier segment contracting by 6.6%. Aside from the lockdowns, the end of the HomeBuilder scheme and the withdrawal of incentives to first home buyers was also occurring, with commitments to that group down 15.2% on the quarter. Investor commitments posted a 7.9% lift in Q3, with the tightening in some rental markets (outside Sydney and Melbourne) and rising house prices positive fundamentals for the segment.

Housing Finance — September | Insights

An overall mixed picture in September as the lockdown in Victoria had an outsized impact on the headline result. Owner-occupier commitments were generally flat to higher across most of the other states and are at very elevated levels. Investor commitments remain on the rise but the momentum has slowed. Looking ahead, the reversal of stimulus measures still has further to run, while the effect of house prices — shown to have risen by more than 20% nationally over the year in the latest release from CoreLogic — on affordability are headwinds. There is also the recent announcement from APRA on the increase to serviceability buffers and speculation of further macroprudential measures. If interest rates are to rise sooner than currently expected by the RBA, that could also slow conditions more rapidly.