The effects of the pandemic and government policy decisions to support households led to the sharpest quarterly fall in Australia's Consumer Price Index (CPI) on record with a 1.9% decline in the June quarter as the annual pace dropped to a 23-year low of -0.3%. Today's report for the September quarter will see some reversal of these effects through the return of out of pocket costs for childcare services in most states and higher petrol prices, though the data will continue to be affected by measurement issues due to the shutdown in Victoria and shifts in consumption patterns in response to continuing restrictions on activity.

As it stands | CPI

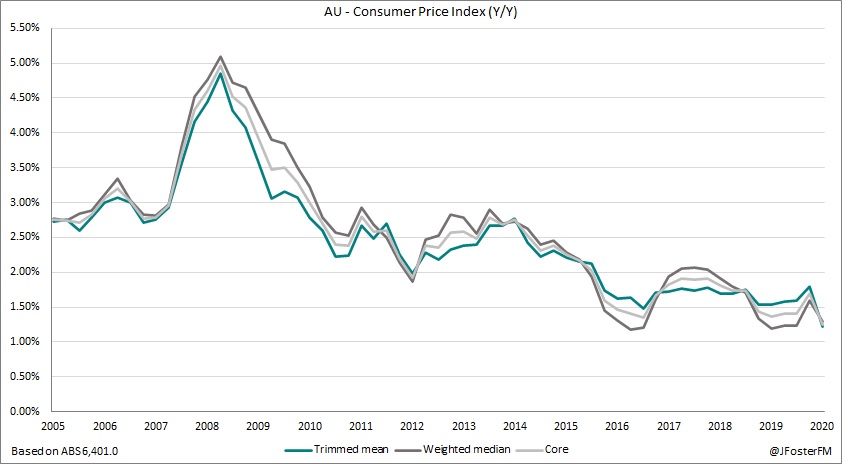

Headline CPI declined sharply in the June quarter by 1.9%, slowing the annual pace from 2.2% to a 23-year low at -0.3%. For the first time on record, quarterly underlying inflation based on the RBA's preferred trimmed mean went negative coming in at -0.2% as the annual pace slowed to 1.2% from 1.8%.

Market expectations | CPI

Today's report is unlikely to shift the markets all that significantly, not least because it is already fully expected that the RBA will ease its monetary stance at next week's Board meeting. For the headline measure, markets look for a 1.5% rebound in Q3 (range: 0.5% to 2.1%). The trimmed mean is forecast to lift by 0.3%q/q on the median estimate.

What to watch | CPI

Pandemic-related effects will continue to heavily impact the CPI data. The continuation of the shutdown in Victoria means that today's outcome will continue to be affected by measurement issues as discussed by the ABS here. Furthermore, the onset of the pandemic and the measures implemented to contain it have significantly shifted previous consumption patterns, and given that the CPI uses a fixed basket methodology it is not well placed to capture these effects as they occur. Given these crosscurrents, gauging current inflation trends from the CPI readings in isolation is not straightforward. For today's report, the most significant contributors adding to the CPI outcome will be the unwinding of free child care services (in all states outside of Victoria) that will largely reverse the 95% decline in price for those services in Q2 and the rebound in petrol prices. Weighing on inflation will be the impact of the Federal Government's HomeBuilder grants scheme that in effect lowers the purchase price of newly constructed houses (up to a limit of $750k).