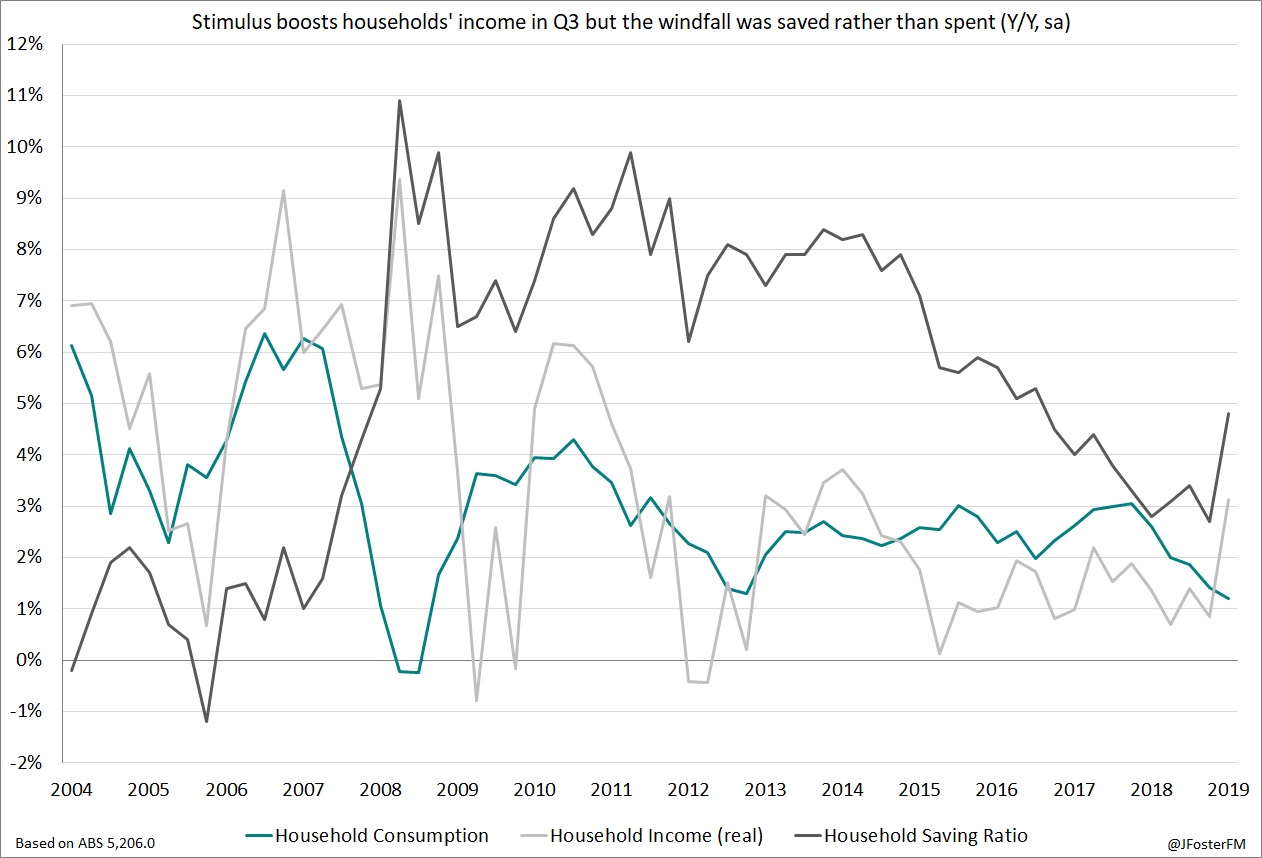

Household consumption growth lifted by just 0.1% in Q3 — its softest quarterly outcome since Q4 2008 — while in annual terms, the momentum slowed from 1.4% to 1.2% to be at its weakest pace in the post-GFC period. In context, household consumption growth was running at a 2.6% annual pace a year ago. Factors that have driven this slowdown include subdued confidence due to concerns over the economic outlook, uncertainty in the lead-up to May's federal election and from developments offshore as global growth has slowed, a correction in house prices and low wages growth. In the quarter, the benefits from the RBA's rate cuts in June and July and the Federal government's tax cuts began to flow. As a result, in nominal terms, tax payments fell by 6.8% and interest payments were down by 2.5%. Adjusting for inflation, real household disposable incomes accelerated by 2.1% in Q3 to an annual pace of 3.1%, which is a 5-year high. However, this income boost was largely saved by consumers as the household saving ratio surged up by 2.1ppts to 4.8% to a 2½-year high and helps to explain the soft outcome for household consumption in Q3 (see chart of the week, below)

Chart of the week

The National Accounts also continued to highlight that residential construction and business investment remain areas of concern in the domestic economy. The downturn in the residential construction cycle intensified in Q3 as activity contracted by 1.7% to be down by 9.6% over the past year, which is its sharpest rate of decline in 7 years. Activity in new home building is even weaker at -11.0% through the year and is contracting at its fastest rate in 18 years. With dwelling approvals showing renewed weakness in October with an 8.1% fall (-23.6%yr), the downturn in activity is likely to persist throughout 2020 (see here). Private sector business investment fell by 2.0% in Q3 and -1.7% for the year, with the annual pace remaining in contraction for the 5th straight quarter. Mining investment took a final step lower as major projects reached completion to be down by 7.8% in the quarter and -11.2% for the year, though the outlook is for a rise of around 16% in 2019/20, based on the recent ABS Capital Expenditure Survey. Non-mining investment was up by 1.2% in Q3 and 2.2% through the year, but as covered in last week's review, plans for 2019/20 are looking less constructive, with uncertainty from offshore and weak domestic demand conditions headwinds for the investment climate.

In contrast to weak private sector demand, robust growth in public demand remained in train over Q3 with a 1.5% rise to be up by 4.9% in annual terms. This has been supported by spending associated with public healthcare initiatives and investment in infrastructure in response to strong population growth. The other leading contributor to activity over the past year has been net exports (1.1ppts). Export volumes were up by 0.7% in Q3 to 3.3% in annual terms, driven by a ramp-up in production from the resources sector and strong demand for services associated with tourism and education. Meanwhile, weakness in exports (-0.2%q/q, -1.5%yr) reflects declining investment in capital goods and the impact of a lower Australian dollar. This profile ensured the current account remained in surplus for the second consecutive quarter in Q3 (see here), though the trade surplus subsequently pulled back by $2.3bn in October to $4.5bn as iron ore prices corrected from their mid-year peaks (see here).

— — —

In offshore developments this week, conflicting trade headlines saw markets swing between gains and losses. To start the week, US President Trump announced he would restore steel and aluminum import tariffs on Argentina and Brazil on the basis that these two countries had been "presiding over a massive devaluation of their currencies, which is not good for our farmers". Later on in the week, President Trump said that he was in no haste to complete the phase one trade deal with China, though the planned 15% tariff on a $160bn tranche of Chinese imports would go ahead on December 15 if the status quo remained. The latest US activity data produced contrasting results this week, with manufacturing conditions according to the ISM survey remaining in contraction after falling from 48.3 to 48.1 in November as the new orders and employment sub-indexes declined, though in the more broadly-based Markit Purchasing Managers' Index (PMI) the sector is in expansion as conditions improved over the month from 51.3 to 52.6 on gains in new orders and employment. Similarly, the ISM non-manufacturing survey indicated conditions in the services sector slowed from 54.7 to 53.9 driven by a sharp fall in business activity, while Markit's services PMI firmed from 50.6 to 51.6 on renewed strength in new business after a fall in the previous month. The overall state of conditions was perhaps best summarised by Markit's Composite PMI, which firmed from 50.9 to 52.0 to indicate private sector business activity across the US was increasing modestly at a below-average pace.

The consumer continues to hold the key to growth in the US and that is not surprising given the strength of the labour market. On Friday, the latest employment data for November was much stronger than expected; even allowing for 48k GM workers returning from strike, as non-farm payrolls added 266k jobs in the month compared to the 180k expected. An easing in the participation rate to 63.2% enabled the unemployment rate to reverse its increase in October and return to its equal-lowest in 50 years at 3.5%. Wages growth was solid at 3.1% over the year but is relatively well contained considering how tight the labour market is. As a result, consumers are feeling more optimistic as sentiment according to the University of Michigan's index lifted by a robust 2.5% in December to a 7-month high at 99.2 driven by a more upbeat assessment of current economic conditions.

Turning to Europe, GDP growth in the bloc in the September quarter was confirmed at 0.2% and the annual pace held steady at 1.2%. Overall, domestic demand remains supportive of activity, but weakness in the global economy and uncertainty associated with trade and geopolitical tensions has weighed heavily on net exports and inventories. So far in Q4, activity remains soft according to Markit's composite PMI, which was unchanged at 50.6 in November and indicated the economy was close to stalling. The weakness remains centred on the manufacturing sector, which is currently mired in its deepest downturn in 7 years despite an improvement in Markit's manufacturing PMI from 45.9 to 46.9 in November. Conditions in Germany are of key concern, with industrial output contracting by its fastest pace in a decade at -5.3% over the year to October. Meanwhile, the more domestically-focused services sector remains in an expansionary phase but activity is slowing as Markit's services PMI fell from a reading of 52.2 to 51.9 in November.