Labour Force Survey — October | By the numbers

- Employment on net fell by 19.0k in seasonally adjusted terms in October going completely against market expectations for a 16.0k increase. September's initially reported increase of 14.7k was revised down to 12.5k.

- The national unemployment rate lifted against expectations rising from 5.2% to 5.3%, to reverse the 0.1ppt fall from September.

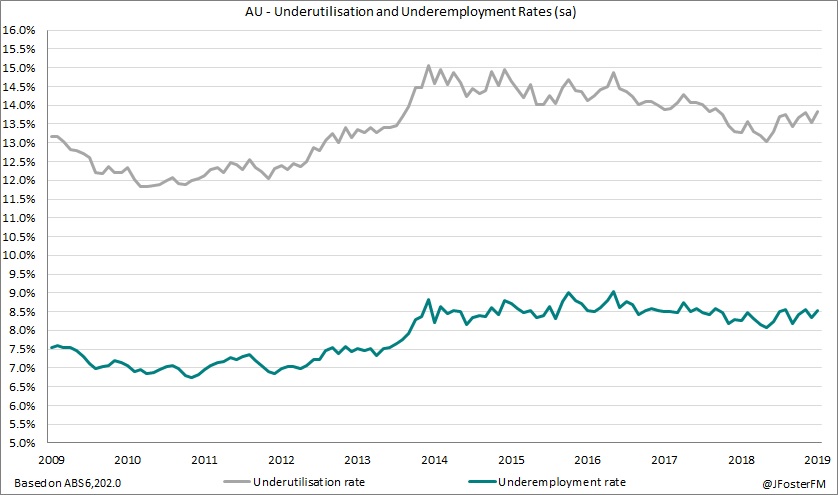

- Underutilisation lifted from 13.5% to 13.8% and underemployment increased from 8.3% to 8.5%, with both measures handing back their declines from September.

- The workforce participation rate fell by 0.1ppt 66.0% (exp: 66.1%).

- Aggregate hours worked declined by 0.2% in October (prior 0.2%) to 1.78bn hours, while the annual pace slowed from 1.9% to 1.4%.

Labour Force Survey — October | The details

Australia's unemployment rate lifted to its highest level in 16 months when taken at 2 decimal places after rising from 5.20% to 5.32% in October. The workforce participation rate decreased for the second consecutive month, easing by 0.1ppt to 66.0%; the last time participation recorded back-to-back falls was in February and March 2018. In absolute terms, this equated to a 1.9k decline in the workforce, and with employment falling by 19.0k the total of unemployed increased by 17.1k.

The 19.0k fall in net employment in October was the weakest outcome since August 2016 and was the first monthly fall in 17 months. There were declines from full-time (-10.3k) and part-time (-8.7k) work this month; the last instance of both segments falling in a month was in August 2016. These weak employment outcomes also saw underemployment (includes workers who want additional hours) and underutilisation (includes the underemployed and unemployed) rise to 8.5% and 13.8% respectively.

Total employment growth in annual terms fell from 2.5% to 2.0%, though this includes a sizeable base effect (employment increased by 39.9k in October 2018). Growth in full-time work slowed from 2.2% to 1.6% over the year; in the first half of 2019 full-time was averaging increases of 19.7k jobs per month but this has decreased to just 8.3k so far for the second half. The pace of growth in part-time work was little changed at 2.9% from 3.0% last month.

Labour Force Survey — October | Insights

Today's report was a surprise and the details were much weaker than expected. Some perspective is required, though, considering that employment outcomes have outperformed market expectations by an aggregate of around 58k so far in 2019. Certainly, the forward-looking indicators have been pointing to a slowdown in employment growth for some time, which if this materialises will bring it closer towards growth in the working age population, thus making it more difficult for policymakers to lower the spare capacity that exists in the labour market. Not surprisingly, expectations for further RBA easing have firmed following this report, with another RBA rate cut looking likely in early 2020.

Australia's unemployment rate lifted to its highest level in 16 months when taken at 2 decimal places after rising from 5.20% to 5.32% in October. The workforce participation rate decreased for the second consecutive month, easing by 0.1ppt to 66.0%; the last time participation recorded back-to-back falls was in February and March 2018. In absolute terms, this equated to a 1.9k decline in the workforce, and with employment falling by 19.0k the total of unemployed increased by 17.1k.

The 19.0k fall in net employment in October was the weakest outcome since August 2016 and was the first monthly fall in 17 months. There were declines from full-time (-10.3k) and part-time (-8.7k) work this month; the last instance of both segments falling in a month was in August 2016. These weak employment outcomes also saw underemployment (includes workers who want additional hours) and underutilisation (includes the underemployed and unemployed) rise to 8.5% and 13.8% respectively.

Aggregate hours work fell by 0.2% in October to 1.784bn hours, as annual growth eased from 1.9% to 1.4%. Making the adjustments to account for the decline in employment in the month, average hours worked per employee held steady at 138.1 hours (-0.6%Y/Y).

Turning to the states, New South Wales' unemployment rate lifted from 4.5% to a 15-month high of 4.8%. Victoria's unemployment rate also stands at 4.8% after a 0.1ppt rise this month. Elsewhere, unemployment in Queensland (6.5%) and Western Australia (5.7%) held steady, while it fell from 6.3% to 6.2% in South Australia and from 6.2% to 5.9% in Tasmania.

Employment growth has pulled back noticeably in New South Wales in recent months and is now neck and neck with Queensland for second place in terms of their year-ended contributions to national employment. Conditions in Victoria have been resilient to this slowdown, with the state accounting for around half of national employment growth so far in 2019. The details for October were; New South Wales -10.3k, Victoria +2.9k, Queensland -14.0k, South Australia -6.5k, Western Australia +6.3k and Tasmania +0.6k.

Today's report was a surprise and the details were much weaker than expected. Some perspective is required, though, considering that employment outcomes have outperformed market expectations by an aggregate of around 58k so far in 2019. Certainly, the forward-looking indicators have been pointing to a slowdown in employment growth for some time, which if this materialises will bring it closer towards growth in the working age population, thus making it more difficult for policymakers to lower the spare capacity that exists in the labour market. Not surprisingly, expectations for further RBA easing have firmed following this report, with another RBA rate cut looking likely in early 2020.