Australia's December quarter national accounts are scheduled to be published by the ABS at 11:30am (AEDT) today. Following a large contraction in activity associated with the Delta lockdowns, the Australian economy rebounded strongly in Q4 as the affected states reopened. Restrictions started easing early in the quarter after vaccination rates met key thresholds, setting the recovery back on track. Fiscal stimulus played a key role during the lockdowns by supporting incomes and boosting savings, enabling household spending to drive the recovery on reopening. Estimates are for GDP to have rebounded by more than 3% in Q4.

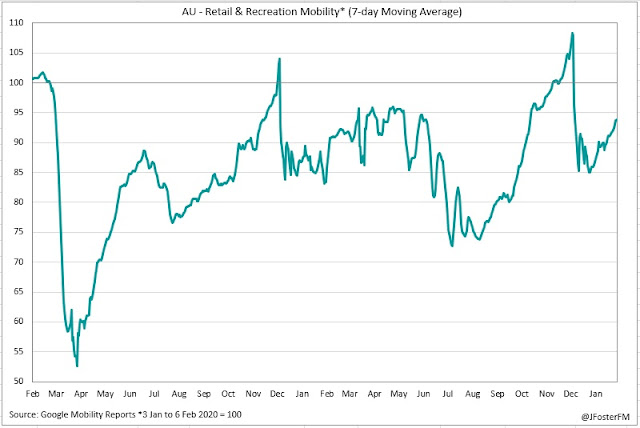

Reflecting the effect of eased restrictions in Sydney and Melbourne, mobility indicators in the nation's two major capital cities recovered to higher levels than before the lockdowns. Meanwhile, average mobility across the other capitals was running well above pre-covid levels by the end of the year.

With people able to get out and about more and consumer sentiment at strong levels bolstered by the vaccine rollout, visits to retail and recreational venues surged nationally in the lead-up to Christmas, reaching higher levels than 12 months earlier.

This flowed through to a robust rebound in household discretionary spending, driving the economic recovery. Retail sales volumes increased at a record pace in Q4, with the strongest rebounds seen in clothing and footwear, department stores and cafes and restaurants.

Strong sentiment, pent up demand and a high level of accumulated savings underpinned the rebound in household spending, while a tightening labour market was also key support. The national unemployment rate fell to a 13-year low in December at 4.2% and occured alongside a recovery in labour force participation to around record highs. Overall, both employment and hours worked rebounded above their pre-pandemic levels after a weak Q3.

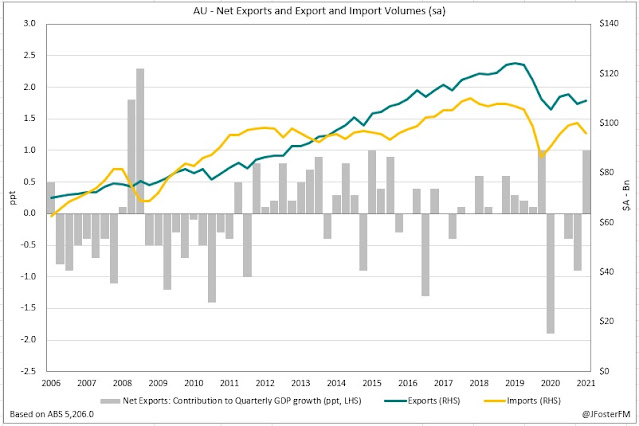

Activity in the Sydney and Melbourne housing markets rebounded in the quarter after being weighed by restrictions during the lockdowns; however, the pace of price gains slowed in both cities. Policy stimulus from the HomeBuilder scheme, government incentives and low rates had led to an elevated residential construction pipeline, though disruptions from lockdowns and capacity constraints had slowed the pace of activity over the second half of the year. Business investment rebounded from a weak Q3 but was patchy, with non-residential construction rising as equipment spending was soft. Net exports look likely to unwind their sizeable contribution to GDP in Q3. The economic recovery supported import spending, though global supply chain constraints remained a headwind. Exports earnings were boosted by rising LNG and Coal prices, even as the iron ore price retraced from elevated levels.

As it stands | National Accounts — GDP

The return of lockdowns across large parts of the nation following the emergence of the Delta variant led to a 1.9% contraction in Australian GDP in the September quarter. The economy transitioned from the recovery to the expansion phase over the first half of the year, but the Delta setback saw GDP falling back below its pre-pandemic level.

Offshore, the Delta variant was also a headwind, slowing quarterly GDP growth in OECD economies from 1.7% to 1.1% in Q3. The US economy slowed sharply to 0.6% in Q3 as household spending was weighed by rising virus caseloads, a fading fiscal impulse and supply chain pressures. Across the Atlantic, the euro area economy showed resilience to Delta as GDP firmed to 2.3% in the quarter, while in the UK output moderated to 1.1% after an easing in restrictions boosted Q2 GDP (5.4%). In Asia, regulatory measures to curb leverage and activity restrictions led to a slowdown in China's economy (0.7%), while in Japan GDP contracted (-0.9%) following a resurgence in the virus.

In Australia, lockdowns were in place in New South Wales, Victoria and the ACT for much of Q3, driving a large fall in household consumption (-4.8%). Hardest hit by the restrictions were the services (-5.8%) and discretionary (-11.3%) categories, though goods consumption also contracted (-3.3%) as in-store retail in the affected states was largely shuttered.

Alongside the decline in consumption, government income support measures were ramped up to similar levels seen at the outset of the pandemic, leading to a surge in the household saving ratio, from 11.8% to 19.8%.

The strong upswing underway in private investment was disrupted by the lockdowns, falling by 0.3% in Q3. Residential construction stalled (0.1%), with materials and labour shortages an additional constraint. Restrictions associated with the lockdowns temporarily weighed on activity in Australia's major housing markets in Sydney and Melbourne, with listings falling and price gains slowing. New business investment contracted by 1.1% in the quarter as many firms delayed spending on equipment and machinery (-3.1%).

Both public demand and net exports contributed strongly to quarterly GDP, helping to attenuate some of the weakness in domestic demand conditions. Public spending (3.6%) was boosted by the pandemic response from governments as the rollout of the vaccine was accelerated. Meanwhile, resources exports rebounded from weather-related disruptions, driving a 1ppt contribution to growth from net exports, its largest contribution in 6 years. Import volumes fell in response to the lockdowns and global supply chain pressures, with the latter also causing inventories to be drawn down substantially in the quarter.

Key dynamics in Q4 | National Accounts — GDP

Household consumption — Reopening from lockdowns and the increase in accumulated savings drove a sharp rebound in household spending. Accordingly, retail sales volumes rebounded by 8.2%, the strongest quarterly rise on record as discretionary demand for goods and services snapped back. Consumer sentiment was at strong levels over the quarter, reflecting confidence in the vaccine to mitigate the pandemic, increasing household wealth and the strength in the labour market.

Dwelling investment — The upswing in the residential construction cycle lost momentum over the second half of the year, disrupted by lockdowns and materials and labour shortages. Private sector residential construction work contracted by 3% in Q4, with new home building down by 1.9% and alterations falling by 8.7%.

Business investment — Private sector capex rebounded by 1.1% in Q4 but was held back by weakness in equipment spending (-0.1%) on residual lockdown effects and global supply chain constraints.

Public demand — A 0.4% contraction in Q4 will see public demand weighing modestly on GDP. Government spending stabilised in the quarter (0.1%) and remained at a high level, supported by the pandemic response. Underlying public investment declined in the quarter (-2.2%) but is bolstered by a large pipeline of projects.

Inventories — Some improvement in global supply chain pressures assisted businesses in restocking inventories over the quarter from low levels. Inventories likely added around 1ppt to quarterly GDP.

Net exports — Export volumes fell by 1.5% in Q4, weighed by a contraction in resources shipments. Global supply chain constraints remained a headwind to imports (-0.9%). Overall, net exports will subtract 0.2ppt from quarterly GDP.