The Ukrainian crisis left markets stuck between geopolitical turmoil and hawkish central bank expectations this week. The effect of economic sanctions on Russia will need to be worked through, as will the implications of surging energy prices when inflation is already high.

Australian wages growth was only slightly stronger in Q4...

The pace of wages growth remained contained in the December quarter rising by 0.7% to be 2.3% higher over the year. A material tightening in the labour market post the Delta lockdowns contributed to a more broad-based lift in wages growth than in the previous quarter, though not enough pressure has built up to prompt the RBA to pivot away from its patient stance on rates at next week's meeting.

Reopening effects and labour shortages helped lift wages growth in goods-related and household services industries, but the pace moderated in business services industries. As the labour market has tightened, upward pressure on wages is mainly coming through in the private sector (2.4%), and in particular where individual agreements are used. Increased churn caused by the pandemic, seeing many workers move between roles and industries, has pushed up incentives as firms look to retain staff. Private sector wages including bonuses advanced from 2.2% to 3%, its fastest since Q3 2019. Public sector wages growth lifted to 2.1% but remains below its pre-pandemic pace, held back by wage caps despite some easing in Q4. A full review of the Q4 Wage Price Index release is available here

Construction activity and business investment were softer than expected...

Inputs for construction activity and business investment ahead of next week's Q4 GDP data disappointed to the downside this week. However, resurgent household spending is expected to see the Australian economy rebound by around 3% in the quarter (previewed here).

Construction work done declined by 0.4% in the quarter, defying expectations for a 2.5% rise (reviewed here). Pandemic-related restrictions on the sector in Victoria led to a sharp fall in activity there (-5.5%), while softness in some other states also weighed. Private sector residential construction declined by 3% in the quarter as restrictions and capacity constraints weighed on new home building (-1.9%) and alterations (-8.7%), holding up progress in working through what is a very large stimulus-boosted pipeline.

Indicators of business investment were patchy. The construction activity data showed weakness in private engineering work (-3.5%), which looks mainly attributable to the restrictions in Victoria, though non-residential construction provided some offset (0.8%). Private sector capital expenditure broadly reversed Q3's lockdown-induced fall but the rebound was softer than expected at 1.1% in Q4 (reviewed here). The internals of the report showed that weakness in equipment spending (-0.1%) weighed, due to residual lockdowns effects and global supply chain constraints. Looking beyond the pandemic, firms' forward-looking investment plans were upgraded and look constructive. Expected capex spending in 2021/22 was lifted by 1.6% to $140.7bn, while the initial estimate of spending in 2022/23 was nominated at $116.7bn, its highest level since 2014/15.

Fed narrative is largely unchanged...

For the Fed, communications and the price action indicate little has changed for the US central bank despite the events of the past week. Inflation on the Fed's preferred core PCE deflator pushed higher in January, rising from 4.9% to 5.1%yr. Goods continued to be the main driver of price pressures (8.8%yr); however, services inflation had also picked up (4.6%yr). Prior to the release, the Fed's Governor Waller said high inflation would keep a 50bps hike on the table at the March meeting; going on to express the view that a total of 100bps of hikes were needed "over the next several months".

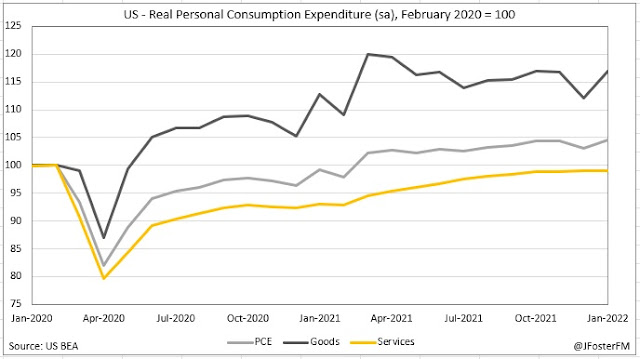

Data this week reaffirmed the strength of US consumer demand. Real personal spending rebounded from a fall in December with a stronger-than-expected 1.5% rise in January (5.4%yr). Underlying the rise was the sharpest month-on-month increase in real good spending (4.3%) since March 2021. With real services spending flat (0.1%m/m), it appears rotational effects in spending patterns were in play as Omicron surged early in the year.

Inflation pressures continue in Europe...

January's annual headline inflation rate was confirmed at 5.1% in the euro area, while the core rate eased to 2.3%. Survey data indicates inflation pressures continued in February, even though supply constraints showed signs of easing. Rising wages in a tightening labour market and elevated energy prices have forced many firms to push these increases through to consumer prices, resulting in a large rise in average goods and services prices in February according to IHS Markit. The flash estimate of euro area activity lifted to a 5-month high as Omicron effects eased, with the composite PMI printing at a 55.8 reading. But, clearly, the geopolitical crisis in the region has clouded the outlook significantly. The ECB's Schnabel said in such a time of uncertainty, the central bank would "need to be a source of confidence and a reliable anchor for the economy". From a monetary policy perspective, and in light of inflation pressures, this meant maintaining its stated sequencing for normalisation. Schnabel said the 3 guideposts to this process were: forward guidance on the conditions needed to justify higher rates, a commitment to ending asset purchases before hiking rates, and to continue reinvesting maturing bonds for an "extended period" after the first hike.

BoE tells markets not to get carried away...

Bank of England officials appeared before the Treasury Committee this week, with Governor Bailey warning markets "not to get carried away" with aggressive rate hike expectations, highlighting there were downside risks to inflation if energy prices fell in line with futures pricing next year. Markets have at least 5 more hikes priced in for the rest of 2022: a path that would see an output gap starting to widen in 2024 according to Bank forecasts.

Accordingly, a speech from MPC member Tenreyro outlined that monetary policy would need to balance the trade-off between containing high inflation and the risk of slowing the economy below its potential, and did not see the process of balance sheet reduction as having a large effect on the scale of tightening that will be required through this cycle. MPC member Ramsden, one of 4 members who voted for a larger 50bps rate hike earlier in the month, said it was important monetary policy acted to prevent second-round effects on inflation from the surge in energy prices.

RBNZ's hawkishness leads to more tightening...

New Zealand's central bank this week reaffirmed its status as the most hawkish of its G10 peers, with the MPC not only announcing a 25bps rate hike (its third in succession) but also raising the projection for the policy rate to peak above 3% from around 2.5% previously and signalling its intention to conduct sales of its bond holdings from July. The Bank's latest Monetary Policy Statement noted that the increase in its policy rate projection was warranted in light of the risk of the upward drift in inflation expectations becoming entrenched into prices.

RBNZ Chart (accessed here)