Australian wages growth firmed in line with estimates in the December quarter, remaining around its pre-pandemic pace. A tightening labour market saw a broader-based lift in wages growth than in the previous quarter, boosted by the reopening from the Delta lockdowns. Although more wage inflation looks to be ahead, the RBA is likely to retain its patience stance with regards to raising rates for now.

- The headline WPI (total hourly rates of pay ex-bonuses) came in around expectations at 0.7% in the quarter and 2.3% over the year. This was slightly firmer than the pace seen in Q3 at 0.6%q/q and 2.2%Y/Y.

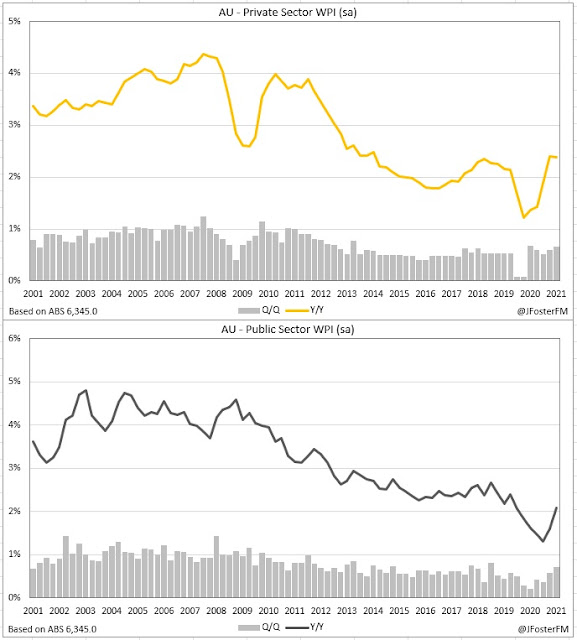

- Private sector WPI increased by 0.7% in the quarter (prior: 0.6%q/q), maintaining the annual pace at 2.4%.

- Public sector WPI also lifted by 0.7%q/q (prior: 0.6%q/q), lifting growth over the year from 1.6% to 2.1%.

Wage Price Index — Q4 | The details

In the release, the ABS noted that individual agreements were continuing to drive growth in the WPI. A strong labour market and demand for skilled workers meant a larger number of employers had conducted wage reviews than usually seen at this time of year. Public sector wage freezes in New South Wales and Queensland started to thaw in Q4, leading to a larger 4th quarter contribution to wages growth from enterprise agreements than in recent years. Meanwhile, the phase-in of the 2020/21 minimum wage decision was continuing to contribute to wages growth in Q4. Normally, the bulk of minimum wage increases occur in Q3, but this was altered by the Fair Work Commission in light of the pandemic, delaying the increase in the most affected industries.

Aside from wage reviews and with employers keen to retain staff, many were turning to other incentives such as sign-on or retention bonuses or offering more attractive conditions to assist in that effort. The WPI inclusive of bonuses lifted by 1.1% in Q4, its strongest quarterly rise since Q3 2019, leaving annual growth up at 2.8% and in line with its pace just ahead of the pandemic. As the chart shows, this is being driven by private sector employers.

At the industry level, annual wages growth had firmed in household services, from 2% to 2.4%, and in the goods-related sector (ex-mining), from 2.1% to 2.3%, as businesses were looking to hire staff back following the Delta wave lockdowns. Wages growth in business services was clearly outpacing these other two sectors in Q3 but the pace moderated in Q4, from 2.6% to 2.4%.

In household services, the main development is the surge in wages growth in accommodation and food services; the industry hit hardest by the pandemic has been left with staff shortages as venues have reopened, with many switching jobs to work in other less contact intensive industries, while border closures have been an additional constraint. In the other industries in the sector, wages growth is for the most part yet to return to pre-pandemic rates.

In business services, the rebound seen over the past year lost some momentum in Q4. Over the period, many businesses have been ending temporary wage freezes or cuts implemented at the outset of the pandemic and this has boosted measured wages growth. Strong demand has been another factor behind the rebound. As it currently stands, annual wages growth in professional services (2.5%), finance and insurance (2.3%) and administration (2%) is around pre-pandemic rates. However, rental, hiring and real estate (2.5%) and information media and telecommunications (2.2%) is now seeing wages growth running above their pre-Covid rates and materially so in the latter.

Developments in the goods-related sector are being driven by reopening effects, with annual wages growth in retail (2.6%), manufacturing (2.5%) and wholesale trade (2.4%) continuing their push higher from pre-pandemic rates. Wages growth in the construction sector moderated (2.4%), which is somewhat surprising after the surge in building work due to construction stimulus measures led to capacity constraints. In the transport industry, wages growth remained constrained (1.8%) but could lift higher now that travel restrictions have eased with airlines needing to rehire staff.

Wage Price Index — Q4 | Insights

All in all, with the labour market tightening post the Delta lockdowns, there was a broader-based rise in wages growth than seen in the previous quarter. However, aggregate wages growth is only around its pre-pandemic pace. Given the tightening seen in the labour market, with overall underutilisation falling to a 13-year low, historical relationships suggest wages growth should be significantly higher (the latest observation is circled). As highlighted earlier, the WPI is a slow-moving indicator and the churn in the labour market caused by the pandemic, with many switching jobs and moving between industries and often receiving higher pay in the process, likely means we will see wage inflation rising over the quarters ahead. But until that hits the data, the RBA will retain its patient stance on interest rates.