Australian construction activity declined against expectations in the December quarter and was weak over the second half of 2021 as lockdowns and capacity constraints disrupted the upswing established in the recovery from the Covid recession. Elevated residential and public sector construction pipelines should support the resumption of the upswing in 2022.

Construction Work Done — Q4 | By the numbers

- Construction work done was much weaker than expected falling by 0.4% in Q4 to $53.5bn (chain volume, seasonally adjusted), though growth through the year was steady at 2.9%. The market consensus was for a 2.5% increase in the quarter, with the lowest estimate looking for a 1% rise. In addition, the contraction reported in Q3 was revised down, from -0.3% to -1.2%.

- Across the categories;

- Engineering work +0.7%q/q to $23.1bn (+4.2%Y/Y)

- Building work -1.3%q/q to $30.4bn (+2.0%Y/Y), which includes;

- Residential work -2.9% to $18.3bn (+0.6%Y/Y)

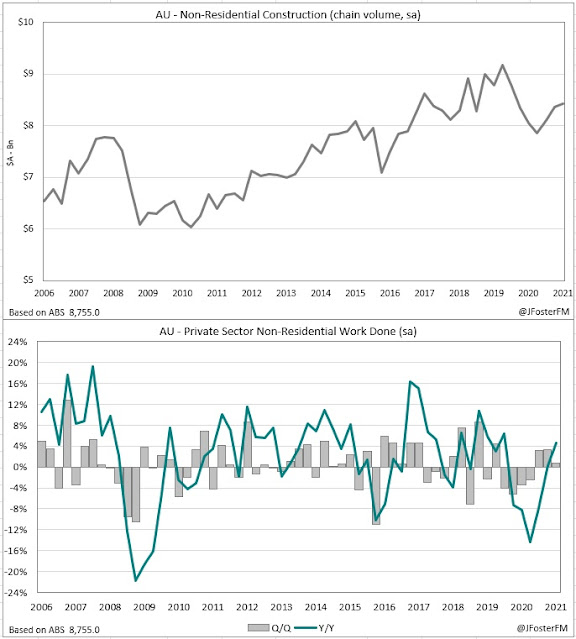

- Non-residential work 1.3%q/q to $12.1bn (4.1%Y/Y)

Construction Work Done — Q4 | The details

Following a strong first half in 2021, the upswing in Australia's construction cycle stalled over the back half of the year. Construction work done had accelerated by 4.6% in the first half of the year reflecting the effects of the HomeBuilder scheme and other policy stimulus but subsequently contracted by 1.6% over the second half as lockdowns and materials and labour shortages held back progress.

Construction activity rebounded in New South Wales in Q4 (5%) after output was hit hard in Q3 (-7.4%) due to the industry being temporarily shut down during the Delta lockdown. Similar restrictions on construction eventually applied in Victoria, which was late in Q3 by that stage. The associated hit to activity looks to have shown up in today's report, with work done in the state declining by 5.5% in Q4. But aside from lockdowns, the momentum was soft with falls in the quarter seen in other states including Queensland (-2.6%), Western Australia (-2.4%) and Tasmania (-0.6%).

At the national level, the key dynamic has been the weakness in private sector construction over the second half of the year (-3.1%), with activity in Q4 down 2.4%. This was driven mainly by the residential segment, with the 3% decline in Q4 taking the fall over the second half to 3.7%. Private residential work surged by 4.5% in the first half of 2021 following policy stimulus from the HomeBuilder grants, other government incentives and low rates; however, lockdowns and materials and labour shortages were headwinds over the second half. New home building fell further in Q4 (-1.9%) while alterations retraced (-8.7%) from very elevated levels.

In contrast to the residential segment, non-residential work accelerated over the second half of the year, with Q4's 0.8% increase resulting in a 4.1% rise over the period. Non-residential work lifted by only 0.6% in the first half. This is broadly reflective of business investment picking up as the economic recovery from the Covid recession gathered momentum. However, private engineering work weakened sharply over the second half of the year (-6.5%).

In the public sector, work done lifted by 7.7% over the second half as governments accelerated the rollout of infrastructure projects as part of their pandemic recovery response. In Q4, engineering work lifted by 6.8% and building work advanced by 1.1%.

Construction Work Done — Q4 | Insights

Lockdowns and capacity constraints disrupted the upswing in Australia's construction cycle over the second half of 2021. Activity in residential construction weakened sharply on these effects, though policy stimulus measures have led to a very large pipeline in the segment that will add to economic growth as it is worked through in 2022. An acceleration in public sector work provided some offset over the second half, and there is much more to come reflecting the focus of governments in recent budgets to invest in infrastructure.