As reopenings draw closer, the RBA remained upbeat on the outlook for the domestic economy at this week's meeting where all settings remained unchanged (reviewed here). Governor Philip Lowe's decision statement on Tuesday noted that many businesses are now preparing for reopenings and that the recovery should start to get back on track over the coming weeks. At the previous meeting in September, the RBA linked the path of its monetary policy to the recovery by extending bond-buying at the $4bn weekly run-rate through to "at least mid February". Firmly reiterating that rates will be on hold until sustainable 2-3% inflation is achieved — something not expected "before 2024" — the RBA retains a stance that sees it amongst the more patient and dovish group of its global counterparts.

With the period of a very low central bank policy rate set to extend, the RBA's latest semi-annual Financial Stability Review identified there had been a "build-up of systemic risks associated with high and rising household indebtedness". Expectations for housing prices to continue to rise could result in increased borrower risk-taking and would be accentuated if banks loosened lending standards, the RBA noted. In that context, banking regulator APRA this week announced an increase to the serviceability buffer lenders apply when assessing new loans. Accordingly, new borrowers will have their ability to service mortgage repayments tested at a minimum of 3ppts above the prevailing interest rate, up from a 2.5ppt buffer previously, placing a curb on borrowers' maximum loan sizes. Further measures could be in prospect with the Council of Financial Regulators indicating it will publish a paper later on in the year on the design and implementation of potential macroprudential policies.

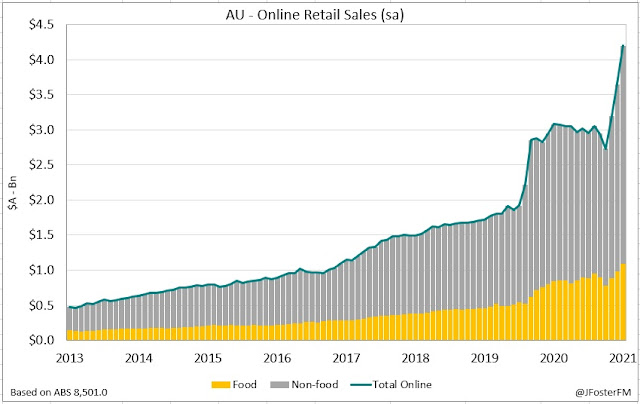

The data to hand through the week continued to reflect the effects of broad-based lockdowns. Retail sales contracted for a third consecutive month with a 1.7% fall posted in August, to be down by 6% since the Delta outbreaks (reviewed here). Over the 3-month period to May, closures and density restrictions have crunched non-food sales (-14.2%), while the stay-at-home mandates have boosted food spending (6.1%) and driven an extraordinary acceleration in online sales (53.5%) from previous highs (see chart below). The latest reading from the ABS's high-frequency payrolls data showed further deterioration in the labour market over the first half of September due to the lockdowns in New South Wales, Victoria and the ACT. As a result, expectations ahead of next week's Labour Force Survey are centered on a 120k fall in employment in September following the 146k contraction in August. In better news, the nation's monthly trade surplus surged through $15bn in August, resetting to a record high for the third month running (reviewed here). Despite a drag from iron ore as prices came off elevated levels, exports were supported by higher prices for other key commodities.

Chart of the week

— — —

The surge in global energy prices amid supply constraints and strong demand have added to the inflation concerns in the market, intensifying speculation over how policymakers may respond. This week, the RBNZ raised rates by 25bps to 0.5%, becoming the second of the G10 central banks to commence its hiking cycle following Norway's Norges Bank. With NZ inflation expected to rise above 4% due to capacity constraints and rising energy prices, the Committee assessed a reduction of stimulus was warranted.

At the Federal Reserve in the US, the question is whether the green light for a November tapering announcement remains on after a weaker-than-expected nonfarm payrolls report for September. Against a consensus of 500k, employment disappointed lifting by 194k in the month, though revisions added back 169k jobs over July and August. As the BLS noted, seasonal volatility played its part in the September report, attributed as the cause of a particularly large fall of 161k seen in state and local government schools that weighed heavily on the headline number. But with job openings sitting at a very elevated 10.9 million, it appears to be the supply side of the labour market holding back the recovery. The participation rate declined 0.1ppt to 61.7% and remains well below pre-pandemic levels at a little above 63%. Despite enhanced unemployment benefits recently expiring and the reopening of schools, people have not returned to the labour force as yet in the volumes many had expected them to. As highlighted in this week's ISM services survey, with labour supply insufficient to meet surging demand, the capacity constraints many businesses report are set to persist.

Shifting across to Europe, the account of the ECB's September policy meeting reiterated that high inflation was expected to be temporary, though there is more nuance emerging around this central view. Some concern was voiced that, with recent readings coming in hotter than forecast, the ECB's internal models may not be accurately reflecting the current inflation dynamics, and that that baseline projection for inflation in 2023 (1.5%) was too low. As noted by ECB Executive Board member Isabel Schnabel in a speech this week, the pandemic may "have altered or reinforced structural trends" and that could affect inflation for years to come. The Governing Council's decision at the September meeting to announce a "recalibration" of its PEPP purchases — moderately dialing back the pace of purchases but keeping the €1,850bn envelope intact — due to a firmer inflation outlook and improved financing conditions portends much more significant discussions in the coming months. With expectations that the PEPP will wind down as guided next March, reporting from Bloomberg indicated ECB officials were discussing introducing a separate program, complementing the existing APP but with greater flexibility, giving it the firepower to quell the risks of a widening in peripheral bond yield spreads.