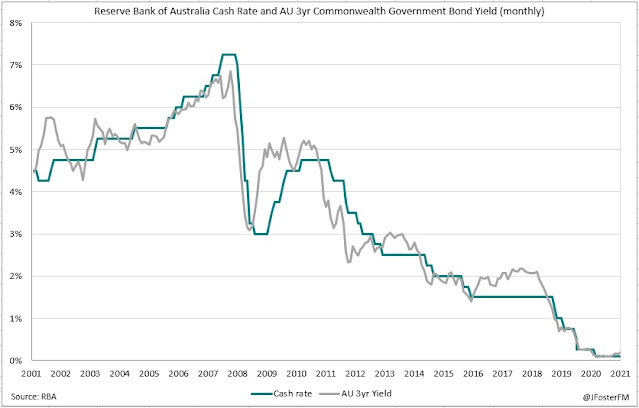

As expected, the RBA left all monetary policy settings (0.1% targets on the cash rate and 3-year government bond yield and QE purchases of $4bn/wk) unchanged at a low key meeting on Tuesday, with the Board intent on maintaining its accommodative stance as it awaits the reopenings of states to get the economic recovery back on track.

Amid all the talk around the path to policy normalisation by central banks across the globe, the RBA continues to remain at the more dovish end of the line. While true that, since the September meeting, QE purchases have been accumulating at the slightly tapered $4bn weekly run rate (from $5bn previously), the deferral of the next review from November "until at least mid February 2022" sets up a slower path to normalisation in Australia following a significant Deltra-driven setback to the economy in Q3. Furthermore, forecasts for subdued wage and inflation dynamics continue to have the Board asserting through its forward guidance and 3-year yield target that rate hikes are not expected "before 2024".

In today's decision statement, RBA Governor Philip Lowe highlighted the effects of the current lockdowns on the economy noting that GDP is anticipated to have "declined materially" in Q3, with the disruptions causing a 4% fall in hours worked in August alone. But the RBA remains optimistic that it is a recovery delayed, not derailed, citing observations from its liaison program where businesses have reported calling back or hiring (or at least attempting to) new staff in preparation for reopenings, and confidence levels that have "held up reasonably well".

However, Governor Lowe pointed out that it was unlikely to be smooth sailing, with the strength of the rebound "likely to be slower" than seen from earlier lockdowns and much uncertainty surrounding the degree and speed at which restrictions will be eased. The latter point is particularly relevant given the varying approaches of states to reopenings. Another factor that could weigh on the recovery are the global supply chain constraints, though Governor Lowe said their effect on Australian inflation "remains limited" for the time being. Broadly, the RBA agrees with the transitory inflation narrative, with today's statement noting that the underlying inflation rate in Australia is 1.75% (its target band is 2-3%) and wages growth is running at a similar pace.

In regards to the housing market, Governor Lowe largely reiterated the message contained in the recent statement by the Council of Financial Regulators that macroprudential measures to curb the pace of credit growth were being discussed. Ahead of Friday's RBA Financial Stability Review, the importance of lending standards being maintained and "appropriate" loan buffers were emphasised during this period of a very low RBA cash rate.

All in all, today's RBA meeting reaffirms its dovish patience at a time when many central banks offshore are moving towards reducing support. RBA watchers can probably take it easy over the summer with policy unlikely to be tweaked until the recovery from the Delta setback is well underway.