The Australian National Accounts for the December quarter are due next week (5/3). Growth in the domestic economy has slowed materially over the past couple of years as headwinds from offshore, higher interest rates and cost-of-living pressures have all impacted. These themes were broadly evident again in the final quarter of 2024; however, some more encouraging signs around households are emerging. Early estimates point to quarterly GDP growth of around 0.3% ahead of more key inputs on public demand, inventories and trade.

A recap: Subdued growth continues

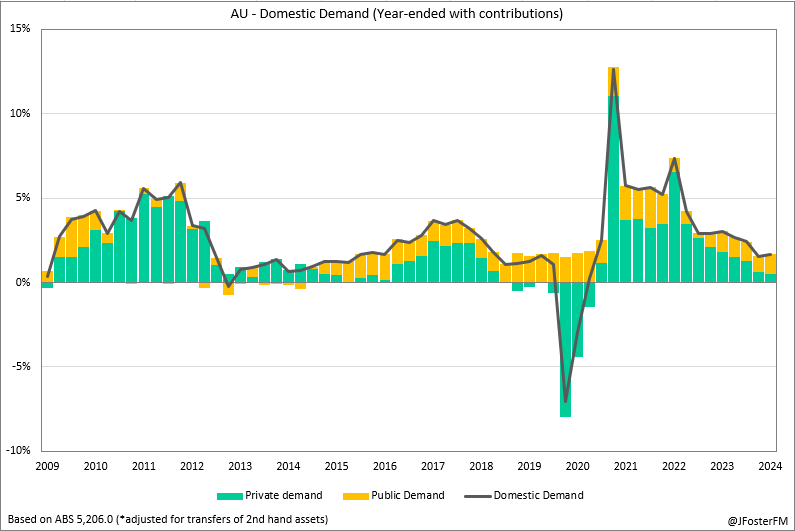

The Australian economy remained subdued in the September quarter. Real GDP expanded by just 0.3% in the quarter, slowing from 1.0% to 0.8% through the year - its weakest pace in 3 decades. Meanwhile, growth in per capita terms remained weak contracting for the 7th quarter in succession (-0.3%).

After declining in the previous quarter (-0.3%), household consumption only managed to stabilise in Q3 (0%), indicating that fiscal support measures had yet to provide a meaningful breakthrough to the malaise caused by higher interest rates and cost-of-living pressures.

Dwelling investment lifted by 1.2% in the quarter but had been weak over the past year (-0.5%) as the cumulative effects of rate hikes and capacity pressures weighed on activity. Meanwhile, weakness in non-dwelling construction drove business investment to its first quarterly decline in 4 years (-0.2%), reducing year-ended growth to 1.5% - down sharply from a 7.5% pace a year earlier.

Amid the overall weakness in private demand (0.1%q/q, 0.7%Y/Y), robust public sector demand (2.2%q/q, 4.1%Y/Y) had become an increasingly significant driver of GDP growth. Government expenditure lifted strongly (1.4%q/q, 4.7%Y/Y) on the back of cost-of-living support measures as well as spending across the health and aged care portfolios. Public investment (6.1%q/q, 2.0%Y/Y) was also contributing to growth via an elevated pipeline of infrastructure projects and spending on defence equipment.

Q4 preview: Households find momentum

Headwinds from offshore persisted into year-end as growth slowed and uncertainty increased in the lead up to the US election. Growth in the OECD eased from a 0.5% pace to 0.3% in the December quarter, with mixed outcomes across countries. While growth remained solid in the US and picked up in Japan, it was broadly flat in the UK and contracted in parts of Europe post the Paris Olympics. In China, growth accelerated in Q4 - due partly to earlier stimulus measures and a frontloading of export orders to avoid tariffs touted by an incoming Trump administration - dynamics that supported an uplift in commodity prices.

Domestically, momentum in household consumption lifted during the Black Friday and Cyber Monday sales events. Price discounting, rising real incomes - bolstered by slowing inflation and fiscal support - and continued strength in the labour market were key factors that drove a sharp increase in quarterly retail sales volumes. The ABS's gauge of household spending also indicated that services spending increased more strongly than in recent quarters.

Improving signs of momentum were also seen in the residential construction sector. Dwelling approvals rose through the middle of the year, and this looked to translate into increased housing starts in Q4. By contrast, non-residential construction activity continued to decline, weighing heavily on business investment in the quarter.

Public demand looks to have again remained the key driver of growth. Support measures to ease cost-of-living pressures as well as spending relating to the provision of government services continues to drive growth in public expenditure. Spending on infrastructure projects and defence are underpinning public investment.

Summary of key dynamics in Q4

Household consumption — The stage 3 tax cuts and electricity rebates appeared to be gaining traction as households turned out strongly for the Black Friday and Cyber Monday sales. Slowing inflation was also a key factor as retail sales volumes increased at their fastest quarterly pace since early 2022.

Dwelling investment — Despite the headwinds from higher interest rates, momentum in residential construction activity improved throughout the course of 2024. In Q4, both new home building and alteration work lifted.

Business investment — Possibly contracted in the quarter based on weak details from partial indicators. Private sector capital expenditure declined by 0.2% quarter-on-quarter, driven by a decline in investment spending (-0.8%). Non-residential construction activity remained weak (-5.4%).

Public demand — Details to be confirmed ahead of the National Accounts release, but public spending and investment are expected to have continued to drive growth in the quarter.

Inventories — International trade data indicates goods import volumes rose in Q4, consistent with a rebuilding of inventories. In the previous two quarters inventories have deducted from growth. Further details are due early next week.

Net exports — Weighed heavily on growth over the past year but have been a modestly positive contributor in the past two quarters. Partial data indicates net exports deducted from growth in the quarter, but key data on services is yet to come to hand.