The Australian economy remains resilient to global and domestic headwinds, but the momentum in growth has slowed to a subdued pace. Real GDP growth was 0.4% in the June quarter - unchanged from an upwardly revised outcome (0.2%) in the March quarter - expanding by 2.1% through the year (from 2.4%). Over the second half of 2022, economic growth was a solid 1.3%; however, the pace slowed to 0.7% for the first half of 2023 as the pressure on households from the higher cost of living and rising interest rates intensified.

Growth dynamics offshore have been similarly challenged in 2023. In the G7, growth has been held up to a large extent by a resilient US economy, attenuating weakness in the euro area and the UK. In China, growth slowed sharply in the June quarter as the reopening lost momentum.

Despite a very strong labour market, elevated inflation left Australian households significantly worse off as real incomes sustained a fall of historic magnitude over the past year. Associated with this, consumer sentiment has been at very weak levels for an extended period.

Moreover, the transmission of the RBA's tightening cycle continued, with the earlier hikes to the cash rate (4.1%) flowing through to mortgage payments and fixed-rate mortgages rolling over to higher variable rates. Interest payments on dwellings rose to a 6.6% share of disposable income in the quarter, an 11-year high.

In response to these headwinds, Australian household consumption growth slowed sharply over the first half of the year (0.4%), with discretionary consumption declining over the period (-0.7%). Nonetheless, aggregate consumption has still increased. Households appear to be drawing down on the large stock of excess savings accumulated during the Covid period to support consumption.

As household consumption has slowed, two overarching factors have contributed to the resilience of the Australian economy. Firstly, rapid post-pandemic population growth (2.4%) has underpinned the rise in output over the past year (2.1%); in per capita terms, real GDP has fallen 0.3%Y/Y.

Secondly, the reopening of the borders has facilitated the recovery of services exports, led by the tourism and education sectors. This has contributed more than 2ppts to GDP growth over the past year.

The growth slowdown reported in the June quarter National Accounts largely validates the decisions by the RBA Board to leave the cash rate on hold at its past 3 meetings. Although the Board retains its tightening bias given the risk of persistent inflationary pressures, an extended pause looks the likely path for monetary policy from here.

— — —

National Accounts — Q2 | Expenditure: GDP (E) 0.4%q/q, 2.5%Y/Y

Household consumption (0.1%q/q, 1.5%Y/Y) — The momentum in household consumption continued to slow due to cost-of-living pressures and higher interest rates. Household consumption nearly stalled at 0.1% in the quarter, increasing by a tepid 0.4% in the first half of 2023, well down from the 1.1% pace realised over the back half of 2022.

Very strong labour market conditions drove household incomes to their fastest increase since 2011 at 8% over the year to the June quarter. But that increase was eaten into substantially by mortgage interest payments that have more than doubled (106.9%Y/Y) due to RBA rate hikes and by a surge in income tax liabilities (15%Y/Y). Those factors left disposable income up by a modest 2.3%Y/Y. Then there is the effect of elevated inflation, which at 6.1%Y/Y on the household consumption deflator implies a historic fall in real incomes of around 3% over the past year. In that environment, households have been saving less and less of their disposable income in order to support consumption; the household saving ratio fell to a 15-year low in Q2 at 3.2%.

Although consumption has still risen, the real income squeeze has had a profound effect on demand patterns. Discretionary-related consumption surged coming out of the pandemic, but households have put the brakes on over recent quarters (-0.5%q/q, 0.6%Y/Y), resulting in essential goods and services (0.5%q/q, 2.1%Y/Y) taking up the running as the major impulse to household consumption.

That said, there are still areas of consumption that remain resilient, including in discretionary-related categories. Notably in the June quarter, new vehicle purchases surged (5.8%) - partly catching up from earlier delays across the ports - while the desire the travel and go out continued to support transport services (3.2%) and hotels, restaurants and cafes (0.2%). The largest pullback in Q2 was in furnishings and household goods (-2.5%), with the category continuing to normalise after surging during the pandemic lockdowns.

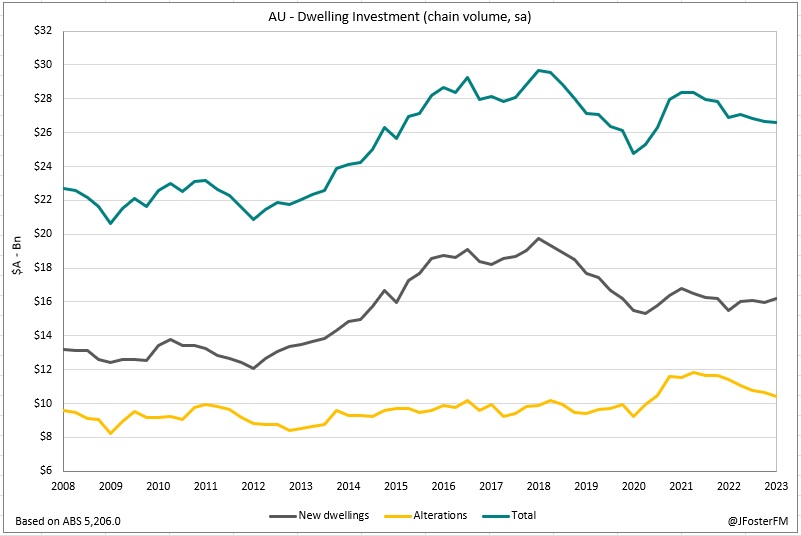

Dwelling investment (-0.2%q/q, -1.1%Y/Y) — Higher interest rates and capacity constraints have weighed on dwelling investment over the past year (-1.1%). In the June quarter, the decline was a relatively modest 0.2%. A welcome rise in new home building came through in the quarter (1.2%) driven by higher-density housing, with detached home building still under pressure from delays. Alterations (-2.4%) continued to unwind from their peaks reached in response to the stimulus measures that supported this activity during the pandemic.

Ownership transfer costs — fees associated with real estate transactions — lifted by 3.9% in the June quarter, its first rise since Q3 2021. This came amid a tight supply-demand balance driving an upturn in housing prices.

Business investment (2.1%q/q, 8.0%Y/Y) — A 2.1% rise in the June quarter saw business investment up by 8% through the year, an upturn that has defied the headwinds of slower global and domestic growth and tighter financing conditions.

Key factors in this resilience have been firms responding to capacity pressures that emerged through the Covid period and progress in the transition to renewable forms of energy. In addition, federal government tax incentives that expired at the end of the 2022/23 financial year brought forward spending, reflected in business investment rising by a sharp 5.7% over the first half of the year.

Machinery and equipment (4.3%) drove business investment in the quarter as global supply chain pressures eased. Intellectual property products (2.2%) posted the fastest quarterly rise in 2 years. Non-dwelling construction (0.3%) was subdued in Q2 but has risen materially over the past year (10.8%) as commercial and infrastructure projects have gathered pace.

Public demand (1.2%q/q, 2.7%Y/Y) — Public demand was a key support to growth in the quarter, adding 0.3ppt to real GDP. As a share of real GDP, public demand remains elevated averaging around 27.5% over the year to the June quarter, well above its pre-pandemic share of output. New investment accelerated by 5.2%q/q (9.4%Y/Y), reflecting progress on major transport, health and education projects across the nation. Government expenditure lifted 0.4%q/q (1.4%Y/Y).

Inventories (-1.1ppts in Q2, -1ppt yr) — A number of factors led to a large decline in non-farm inventories of $3.4bn (chain volume terms) in the quarter, subtracting a substantial 1.1ppts from output. The clearing of port delays facilitated the delivery of new vehicles and equipment. Disruptions that previously affected mining production eased, supporting the export of these commodities. Meanwhile, offshore grain shipments led to a decline in wholesale inventories.

Net exports (0.8ppt in Q2, 1.2ppt yr) — Made the largest contribution of all the expenditure components to GDP growth in Q2 (0.8ppt). Export volumes lifted 4.3%q/q (9.8%Y/Y), recovering to pre-pandemic levels. Reopened borders continued to facilitate the recovery of the domestic tourism and education sectors. This saw services exports advancing by a further 12.1%q/q to be up 50.9% through the year. A rebound in resources shipments (2.4%) also supported exports in Q2. Import volumes were up a modest 0.7% in the quarter, now 8.2% above pre-pandemic levels. Travel services (11.2%) were the major driver, reflecting many Australians travelling to the northern hemisphere for leisure.

— — —

National Accounts — Q2 | Incomes: GDP (I) 0.3%q/q, 2.1%Y/Y

Weaker global growth dynamics hit national income in the June quarter as the prices of Australia's major export commodities declined. In the quarter, export prices fell by 8.2% generating a 7.8% contraction in the terms of trade. This was the largest quarterly fall in 14 years and left the terms of trade down 12.7% on the record high from a year earlier.

Reflecting the terms of trade fall, nominal GDP contracted by 1.2%q/q, which saw growth through the year slowing from 9.5% to 3.6%. Falling nominal GDP was driven by a 1.5% decline in prices - influenced heavily by the fall in export prices - resulting in the real income estimate of GDP lifting 0.3% in the quarter (2.1% year-ended).

Household income continued to be bolstered by the very strong labour market. Robust labour demand led to increased hiring and hours worked, the latter advancing 2.5% across the economy in the quarter (and 2.2% in the market sector). These dynamics drove the compensation of employees measure to a 1.6% rise in Q2 to be up 9.6% through the year.

On an hourly basis, non-farm compensation was running at a 3.1% year-ended pace. But the underlying cost of labour for firms has increased at a materially stronger pace after accounting for productivity trends, which have been weak - a key concern highlighted by the RBA as it could sustain high inflation if firms respond by continuing to raise prices. Non-farm unit labour cost growth was 7.3%Y/Y and 4.9%Y/Y in real terms.

Amid a range of headwinds from falls in commodity prices, margin pressures and slowing demand, private sector (ex-financials) company profits fell 8.6% in the quarter, their largest quarterly decline since 1991. That outcome drove a swing in through-the-year profits from 15.1% to -6.8%.

Gross mixed income (small business and farming profits) was also hit, contracting by 2.7%q/q and 8.8%Y/Y. By contrast, financial company profits lifted 1.2%q/q to 7.2%Y/Y; more fixed-rate mortgages are rolling on to higher variable rates, while the RBA's tightening cycle has driven an expansion in net interest margins.

— — —

National Accounts — Q2 | Production: GDP (P) 0.4%q/q, 1.7%Y/Y

The GDP production approach estimate was 0.4% in the June quarter, in line with the outcomes for the expenditure approach and the headline figure. The year-ended growth rate moderated from 2.2% to 1.7%. Gross Value Added (GVA) increased at a similar pace for business services (0.6%) and household services (0.7%). By contrast, the goods sector was patchy: goods production advanced (0.5%) as goods distribution softened (-0.1%).

Business services (0.6%) saw broad-based strength across the sector. The upturn in housing prices led to increased activity for real estate services (2.7%). Administration advanced (1.8%) on stronger demand for travel services and labour hire. Professional services (-0.3%) was a point of weakness. Turning to household services (0.7%), increased demand for public health services (0.9%) was the main support. Inbound tourism boosted the accommodation and food services industry (0.4%).

GVA from goods production (0.5%) was led by construction (2.2%) and utilities (2.9%). Construction output was supported by increased sub-division activity and by progress on infrastructure projects. Cool weather in the lead-up to winter led to a lift in household electricity and gas consumption that drove utilities. This was moderated by a 1.3% fall in mining, reflecting disruptions to iron ore operations caused by Cyclone Ilsa. Goods distribution (-0.1%) was hit by weakness in retail demand and by an easing in grain trade, both weighing on the wholesale industry (-1.5%). This weakness was largely offset by the transport industry (1.1%) as demand for domestic and offshore travel remained strong.