Sentiment remained upbeat in markets this week on the expectation that the end is in sight for rising interest rates despite the Federal Reserve, European Central Bank and the Bank of England all retaining hawkish messaging at their respective policy meetings. Headline inflation rates are easing but central banks remain cautious with underlying price pressures yet to abate. The improvement in global growth prospects that has been a key factor driving markets so far in 2023 was reflected in the IMF's latest outlook.

Fed tightening nears the end of the line

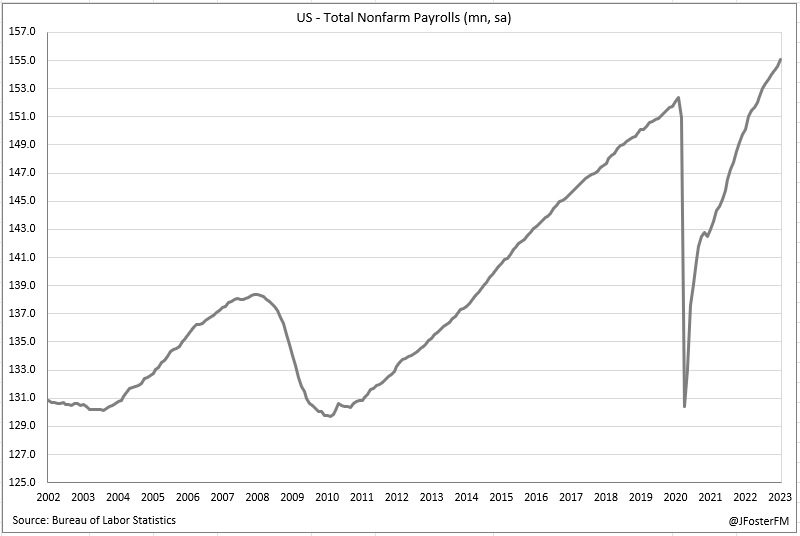

The Federal Reserve's policy-setting committee is approaching the latter stages of tightening monetary policy in the US, downshifting the pace of its latest rate hike to a conventional 25bps increase at this week's meeting. The fed funds target now stands in the 4.5 to 4.75% range, a level close to being "sufficiently restrictive" to lower inflation but still requiring "ongoing increases" to reach that endpoint. In the post-meeting press conference, Fed Chair Powell said that positive real rates across the yield curve indicated settings were already restrictive and it was now a matter of judgment regarding the extent of further tightening that is appropriate. A stunning update on the labour market that saw 517k added to nonfarm payrolls in January topped all estimates by a large margin and led to market pricing coming into alignment with the Fed's guidance for a peak rate above 5%.

Beyond the near term, there remains a divergence of views for the policy outlook between the Fed (signaling it intends to maintain rates at restrictive levels) and markets (expecting rate cuts later in the year), due to differing assessments of inflation stickiness. The market view has led to eased financial conditions - seemingly at odds with the Fed's policy ambitions - though Chair Powell instead highlighted that financial conditions had tightened "very significantly" since early 2022.

Ultimately, it will be inflation developments that determine the path for Fed interest rates. Chair Powell said a disinflationary pulse was beginning to turn the tide on inflation, though it had mainly been concentrated in the goods sector as supply chain pressures had been resolved. The Committee anticipates housing-related inflation to unwind over the course of the year reflecting leading indicators on rents. However, Chair Powell said inflation in the services sector was yet to show signs of abating, which warranted keeping rates restrictive "for some time".

Wage pressures are a key driver of services inflation, though the Fed would have taken some comfort from a softening in both the Employment Cost Index in Q4 (1%) and in average hourly earnings growth in January (4.4%yr). Chair Powell said there were ways in which wage pressures could ease aside from rising unemployment. In that sense, an uplift in labour force participation (62.4%) alongside a decline in the unemployment rate to 3.4% (its lowest since 1969) was a very welcome development.

ECB signals more hikes ahead leaving markets unconvinced

Aggressive tightening from the European Central Bank continued this week as the Governing Council hiked the key rates by 50bps and signalled its intent to press on from there. The plan to commence reducing the balance sheet in March was also reaffirmed. The meeting statement noted the intention is to hike by 50bps again in March but to then "evaluate the subsequent path" for rates based on revised growth and inflation forecasts. In the post-meeting press conference, President Lagarde said underlying inflation pressures left the ECB with more work to do to reach "sufficiently restrictive" levels. That came as January's preliminary inflation estimates showed a cooling in the euro area headline rate from 9.2% to 8.5%yr but the underlying rate holding steady at 5.2%yr.

Markets were left unconvinced by the ECB's hawkish messaging, honing in on references to data dependency in the statement and throughout the press conference. The rates guidance also appeared to clash with the ECB's assessment that the inflation outlook was now "more balanced" than in December due to falling energy prices. From a growth perspective, the euro area economy proved resilient over the back half of the year - the initial estimate for Q4 GDP growth held up at 0.1% - and PMIs have returned to expansionary territory in early 2023. However, the impact of rate hikes is gaining momentum as the ECB's Bank Lending Survey reported a further substantial tightening of credit standards for households and firms. Meanwhile, the war in Ukraine continued to pose a "significant downside risk" to growth prospects.

BoE softens hawkish guidance as inflation turns the corner

The Bank of England's Monetary Policy Committee (MPC) voted 7-2 to hike rates by 50bps to 4.0% but gave indications that the tightening cycle is nearing its conclusion. The newly published Monetary Policy Report contained revised forecasts that now project a much shallower downturn in the economy in the year ahead (-0.7% from -2%) and a faster decline in inflation due largely to falling energy prices. Inflation is now expected to fall back below the 2% target in Q2 next year, brought forward from Q4 2024 previously.

Source: Bank of England February Monetary Policy Report

In the post-meeting press conference, Governor Bailey said while there were encouraging signs that inflation had "turned the corner", the MPC was still guarding against the risk of inflation not converging to this more rapid path back to target. That reasoning justified the 50bps rate hike; however, two key changes made to the MPC's meeting statement signal a softer approach ahead. The guidance for both "further increases" in rates and the pledge to "respond forcefully" was removed and replaced with a line that "...evidence of more persistent pressures" on inflation stemming from the labour market and the services sector would require "further tightening in monetary policy". Markets have interpreted this to mean that rates are close to their peak and expect the size of any further hikes to slow to the more conventional pace of 25bps.

RBA set to hike by 25bps as data deteriorates

The RBA returns from its summer break next week where a 25bps rate hike to 3.35% is widely expected. Markets anticipate the peak rate is approaching and will look to the RBA's updated growth and inflation forecasts for validation. Rates have risen by 300bps since last April and the effects continue to play out in the housing market. Housing prices continued to unwind from their Covid peak in January, while housing finance commitments (see here) and dwelling approvals (see here) have fallen sharply over the year. But it was retail sales that surprised this week as December sales were jolted 3.9% lower (see here). This reflects an unwind in discretionary spending after a Black Friday-boosted rise in November and similar declines were seen in December 2020 and 2021. However, this could also be signalling a slowing in the momentum of household spending.