Australian inflation surprised to the upside of expectations in the December quarter, likely confirming another rate hike from the RBA on its return in February. Surging costs for travel during the peak holiday period, unaffected by restrictions for the first time since the pandemic, and the unwinding of electricity rebates offset easing price pressures in new home building and groceries. The drivers of inflation continued to rotate and a disinflationary pulse from goods will help to lower inflation through 2023, but services inflation is likely to remain more persistent.

Consumer Price Index — Q4 | By the numbers

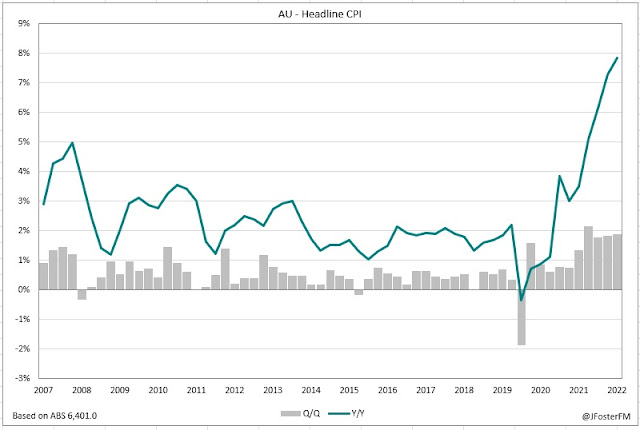

- Headline CPI printed at 1.9% in the December quarter, stronger than expected by markets (1.6%) and up slightly from Q3's 1.8% rise. Annual inflation lifted from 7.3% to 7.8%.

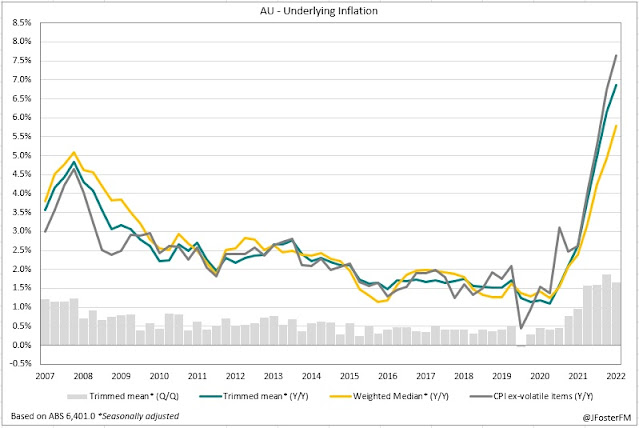

- The average of the three underlying CPI measures was 1.8%q/q, unchanged from Q3, though base effects saw the annual pace increase to 6.8% from 5.9%.

- Trimmed mean was 1.7%q/q — above the 1.5% rise expected but slightly down from Q3 (revised up to 1.9%) — rising to 6.9% over the year from 6.1% (vs 6.5% expected).

- Weighted median firmed to 1.6%q/q (from 1.4%) to be up by 5.8% over the year

- CPI excluding 'volatile items' increased by 2% in the quarter, a touch softer than in Q3 (2.1%), though the annual rate accelerated to 7.6% from 6.7%.

Consumer Price Index — Q4 | The details

Inflation printed at new highs dating back to 1990 as the headline CPI lifted to 7.8% while the trimmed mean (or core rate) moved up 6.9%, a 34-year high. Those outcomes are up substantially from 12 months ago (3.5% headline and 2.6% trimmed mean) as pandemic-related and supply disruptions alongside very robust post-lockdown household spending have caused prices to rise rapidly in Australia and across the globe.

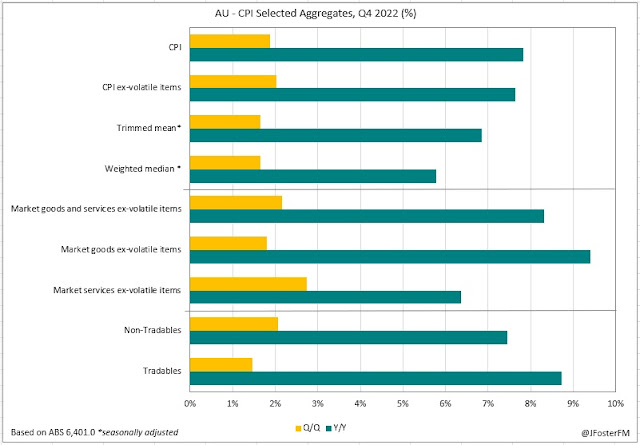

In the December quarter, although there was a notable weakening in new home building costs and grocery prices - both major drivers of inflation over the past year - that was offset by price rises in other ares. Holiday travel costs surged by 10.9% overall in the quarter (13.3% for domestic and 7.6% for international), adding 0.6ppt to the inflation rate alone, reflecting very strong demand over the Christmas/new year period, unaffected by border restrictions for the first time since 2019. Associated demand for dining out and higher overhead costs saw restaurant meals rising another 2.1%q/q. Electricity prices were up by 8.6% in the quarter, contributing 0.25ppt to quarterly inflation as state government rebates applied in the previous quarter unwound.

As has occured in other economies across the globe, there is now a switching in the inflation drivers underway from goods (1.6%q/q) to services (2.1%q/q). The easing of supply disruptions over the course of the pandemic and spending rotating back to services has seen goods inflation slow over recent quarters. This will work to bring down the annual rate, which is only now at the peaks, and in the process help lower the overall inflation rate through 2023.

Services inflation, however, is still rising due to price increases in areas such as rents, utilities and many everyday household services. Rents (4%) and utilities (10.4%) saw their fastest annual rises since 2012 and 2013 respectively. The pace of the rise in household services costs in Q4 (2.9%) has previously only been seen during the reopenings from lockdowns over the past couple of decades.

A specific area worth highlighting is new home building costs. At the peaks in Q3, new home building costs had surged by almost 21% over the year, with a record volume of houses under construction running into supply constraints for materials and labour. Over 2022, this component added more than 1.5ppts to inflation. But the unwind is now underway. Supply pressures are easing and the interest rate sensitivity of the sector has led to the demand for financing to weaken substantially over recent months.

Consumer Price Index — Q4 | Insights

Today's inflation outcomes are stronger than forecast by markets but close to RBA estimates for the headline (8%) and core rate (6.5%). The upshot is that a 25bps rate hike in February looks likely and diminishes the momentum that was building for a pause. Headline CPI on both a 3-month (7.7%) and 6-month annualised basis (7.6%) suggest Q4 is likely to be the peak for inflation. The degree to which inflation slows will largely depend on how the disinflationary pulse coming through in goods prices and other areas such as new home building plays out with price pressures in services components.