Conflicting headlines around Russia-Ukraine tensions dictated sentiment this week, with uncertainty over developments weighing on equities and helping to put a floor under the US dollar amid more insights on policy tightening from the Fed. The overall dynamics kept flattening pressure on yield curves.

Australia's labour market was heavily disrupted by Omicron early in the year...

As the Omicron variant spread and caseloads surged, around 5.6% of employed Australians were unable to go to work, either through illness or from being a close contact, in early January. With another 39% of workers on leave during the peak summer period, this week's labour force survey reported the impact from staff shortages on the economy was an 8.8% collapse in total hours worked in January. A fall of that magnitude has been exceeded only once and that was in April 2020 (-9.6%) when the nation went into lockdown at the outset of the pandemic. After building up strong momentum through the recovery from the Delta wave, hours worked in January had fallen to be 6% below their pre-Covid level.

but underlying conditions were much more resilient than in earlier waves...

Reflecting the resilience the Australian economy has established to the pandemic from each successive wave, underlying conditions in the labour market held up in January. Employment lifted modestly by 12.9k but came in above expectations for a flat outcome. This was broadly sufficient to cover an uptick in the participation rate to 66.2%, keeping the unemployment rate at 13-year lows (4.2%). After tightening considerably in December, underemployment (6.7%) and overall underutilisation in the labour market (10.9%) increased slightly but were still at their lowest levels since 2008. The overall takeaway was that in a tight labour market, businesses are keen to retain staff and despite the uncertainty around Omicron, labour demand continues to rise. Online job vacancies were reported this week to have risen by 4.4% in January to stand 54% above their pre-Covid level, indicating there is scope for the labour market to tighten further. A full review of January's Labour Force Survey can be accessed here

and policymakers are keen to press for more progress towards full employment

Accordingly, Australia's fiscal and monetary authorities are focused on the push towards full employment despite underlying inflation rising to 7-year highs. Treasury Secretary and RBA Board member Dr. Steven Kennedy told the Senate's Economics Committee this week that while fiscal stimulus is gradually tapering as unemployment declines, support should not be withdrawn early based on historical estimates of full employment. In a tightening labour market, Dr Kennedy highlighted that wage gains linked to productivity growth would be key to containing inflation. There was a complimentary tone in the RBA's February meeting minutes, which reaffirmed maintaining highly accommodative monetary policy to support the return to full employment. That said, higher inflation has prompted the Board to emphasise the need for greater optionality, leading to the early withdrawal of QE and signaling that rate hikes this year were plausible. But there remains some reluctance to the idea of raising rates when inflation is being primarily driven by pandemic-related supply issues and wages growth is only around pre-pandemic rates.

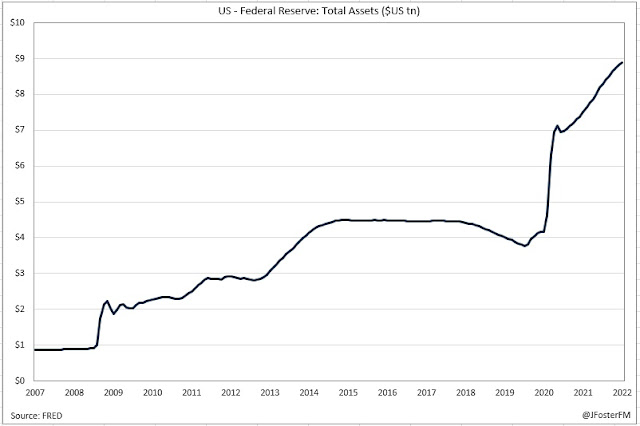

In the US, the Fed could begin balance sheet runoff earlier...

The minutes from the Fed's meeting in late January provided some new insight into how the FOMC sees the process of balance sheet reduction taking place. Boosted by emergency asset purchases over the course of the pandemic, the Fed's balance sheet has expanded from a pre-virus level of around $4tn to around $9tn currently, and the general view of the FOMC is that a "significant reduction" is now appropriate. In light of the strength of the labour market and high inflation, the minutes noted a faster pace of runoff was likely than seen in the previous episode in 2017-2019. The implication is that the timing between liftoff in the policy rate, set to take place in March, and the start of balance sheet runoff will be much shorter in this tightening cycle. The FOMC was also of the view that the strength of the economic outlook likely warranted a more front-loaded increase in its policy rate than during the post-2015 hiking cycle; whether or not that equates to a larger 50bps hike to start with remains a strongly debated issue in markets.

Household spending rebounded sharply early in the year...

Despite the fall in US consumer sentiment to decade lows being linked to high inflation and residual pandemic effects, household spending rebounded strongly in January. Headline retail sales came in at 3.8%m/m (vs 2% expected) after falling by a downwardly revised 2.5% in December. Excluding the categories that have seen prices rise sharply (such as fuel, cars and building materials), control group sales surprised strongly to the upside with a 4.8% surge (vs 1.3% expected), more than reversing December's 4% fall.

In Europe, comments from ECB officials remain key...

Aside from geopolitical tensions in the region, messaging around the policy outlook from ECB officials has been key for markets. ECB President Christine Lagarde was before the European Parliament this week outlining to lawmakers that the current high rate of inflation was likely to persist for longer than previously anticipated, necessitating a more flexible outlook to policy. President Lagarde reaffirmed the Governing Council's December announcements: net purchases in its pandemic asset purchase program would cease in March and to the plan for tapering purchases in its other QE program over the course of the year (though this is to be reviewed at the March meeting). ECB Chief Economist Philip Lane meanwhile has continued to emphasise that with the outlook for inflation over the medium-term expected to stabilise around the 2% target, steps to remove policy accommodation could occur in a gradual manner. There was also pushback from ECB Executive Board member Isabel Schnabel to aggressive expectations for 2022 rate hikes, noting that market pricing factored in term premia and was therefore likely to be providing a somewhat misleading signal with regards to the start of the hiking cycle. In any case, Schnabel reiterated that the ECB's forward guidance required asset purchases to have ended before rates start rising.

UK data were consistent with further BoE rate hikes...

Although UK employment fell by 38k over the 3-month period to December, this was less severe than expected (vs -58k) as Omicron emerged and the unemployment rate held steady around pre-Covid levels at 4.1%. With employment estimated to be down by 588k on its pre-pandemic level there is tightness in the labour market, confirmed by a further elevation in job vacancies to a new record high. All this is putting upward pressure on wages, with annualised pay rates in the final quarter of the year rising from 3.8% to 4.3% (vs 4.2% expected), adding to concerns over inflation, which in January came in above expectations. 12-month headline inflation edged up from 5.4% to 5.5%, while the core rate was up at 4.4% from 4.2%. Due mainly to upcoming increases in household energy prices, inflation is expected to keep rising to be pressing 7% by April. The light remains green for further BoE rate hikes, though it is debatable the MPC will deliver on the 6 additional hikes factored into market pricing over the remainder of the year.