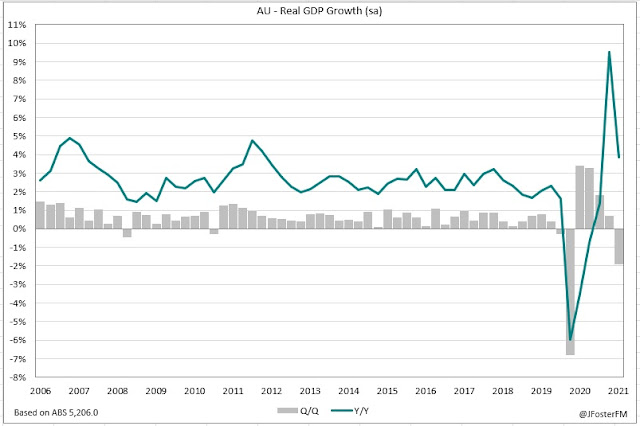

In this year's final piece, I take a look at how Australia's economic recovery from the Delta lockdowns is tracking and what it might mean for the RBA's QE program. With much of the nation locked down due to the Delta wave, the Australian economy contracted by 1.9% in the September quarter. But the ensuing recovery has been incredibly robust and by some measures has been more rapid than the rebound from the national 2020 lockdown.

Mobility indicators — closely aligned with economic activity — in Sydney and Melbourne have surged following reopenings and are higher than before the Delta lockdowns. On average, mobility has also accelerated across the other capitals despite these cities mostly avoiding harsh 2021 restrictions. Whereas earlier lockdowns were eased only after caseloads fell to very low levels, the authorities pivoted in the Delta wave focusing on vaccination targets as the threshold for the reopenings. Confidence in the vaccination program has likely been key in offsetting concern about the circulation of the virus and this is consistent with the higher levels of mobility.

Omicron is now seeing cases accelerate again, though, to date, there is limited evidence of people voluntarily restricting movement. As seen last year, mobility starts rolling over in the lead-up to Christmas as people head for their summer holidays, so while Covid could be a factor in the emerging dip, its overall effect is likely to have been minimal so far.

Driving the recovery has been surging household spending. Since hitting their Delta low in August, Australian retail sales have risen by 6.3% for the period to October as non-food sales have soared (13.1%). Eased restrictions enabling people to get out and about has supported very strong spending on clothing and footwear (35.2%) and at cafes and restaurants (25.9%).

Key to the rebound has been the run-up of savings that households accumulated during the lockdowns. With spending opportunities limited and incomes being supported by fiscal measures, the household saving ratio lifted by 8ppts in Q3 to 19.8% and is just off the peaks seen last year. This has been working to support consumption following reopenings.

Beyond the period of the official statistics, indications from high-frequency data sources are that spending has then accelerated through November and into December. National retail and recreational visits are at the highs seen 12 months earlier and patronage at restaurants has rebounded to be at elevated levels.

When it all washes through, it is quite likely that retail sales volumes will have risen at a record pace in the December quarter, surpassing the 6.3% reopening rebound after the 2020 national lockdown. Bear in mind that Q4 retail volumes will be coming off a larger fall (-4.4% in Q3) than was seen during the national lockdown (-3.5%).

In the labour market, the recovery has exceeded expectations with both employment and hours worked rebounding back above pre-pandemic levels in November. Employment surged by a record 366.1k and in a single month more than recovered the fall sustained during the lockdowns (-359.5k). Hours worked lifted 4.5%m/m and were just off the highs seen prior to the Delta wave.

The rapid rebound in employment and hours worked has seen the labour market tighten considerably. The unemployment rate has fallen to 4.6% from a Delta peak of 5.2%, while broader measures of underutilisation have reversed their increases recorded over the past few months. Importantly, these outcomes have occured alongside a rebound in labour force participation to pre-Delta levels.

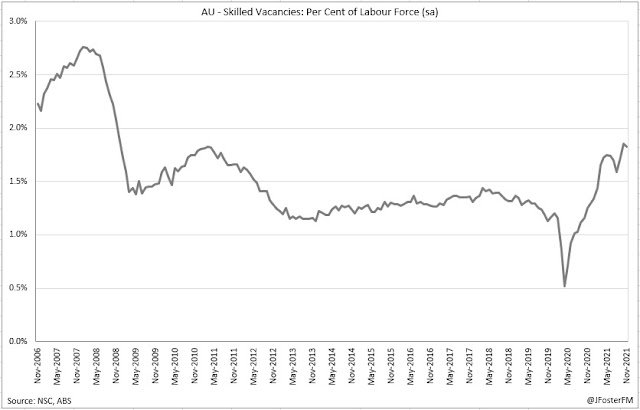

Signs are that the strength in the labour market has further to run, with the ABS's payroll jobs index lifting further over the second half of November, remaining sharply above pre-Delta levels. Meanwhile, labour demand measured through job vacancies are at their highest as a share of the labour force in a decade.

When the RBA returns from its summer break in 2022, it will review its QE program. Since the pandemic, the RBA has added around $340bn of Australian and state and territory government bonds to its balance sheet, with around $260bn of this accumulated in the QE program and around $80bn acquired in support of its now-discontinued 3-year yield target.

QE program purchases are running at a $4bn weekly pace after being tapered from $5bn in September. RBA Governor Philip Lowe recently said the Board was keeping its options open but its base case was that there would be a further taper in February ahead of ceasing new purchases by May. This largely reflects the RBA wanting to see a faster pace of wages growth to give it confidence it can deliver sustainable inflation in the 2-3% target band. Currently, wage and price pressures are much more subdued in Australia than in other major economies.

The RBA has also mentioned it could end new purchases in February, with the strength of the recovery discussed and the accelerated taper schedule recently announced by the Fed in particular potentially tilting the balance that way. This is the option I see as more likely at this stage, however; it will probably require the RBA to upgrade its 2022 forecasts for unemployment (4.25%) and inflation (2.25%) in February, with December's labour force report (due 20/1) and the Q4 CPI data (25/1) to be highly influential here. The Board will also be assessing the headwind of Omicron over the summer, but the Australian economy has shown its resilience over 2021 and this is a recovery that has a lot of momentum.

---

All the best for the holidays and, as always, thanks for reading.