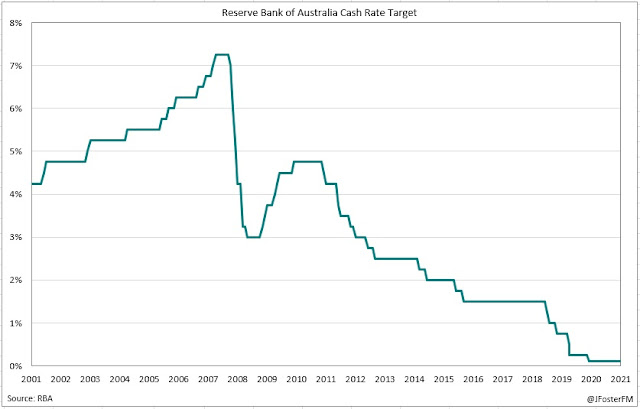

The RBA Board delivered an upbeat assessment of conditions ahead of its summer break with the recovery from the Delta lockdowns gathering pace while also reiterating its patient approach to policy going into 2022. All settings (cash rate target 0.1% and QE at $4bn/wk) were left unchanged at today's meeting.

In his decision statement, Bank Governor Philip Lowe noted the indicators on household spending and the labour market had confirmed the economy was now rebounding strongly from the winter lockdowns that saw Q3 GDP contract by 1.9%. This momentum should see the economy back on its pre-Delta track by the first half of 2022. While the emergence of Omicron is characterised as "a new source of uncertainty" it is not expected to get in the way of the recovery.

Governor Lowe pointed to some signs of a tightening labour market, including the high level of job vacancies and instances of labour shortages, however; wages growth remained around the lows seen prior to Covid. The responsiveness of wages to a tightening labour market is key to the inflation outlook but is a major area of uncertainty for the RBA given Australia's limited history with an unemployment rate in the low 4s, which is the range the Bank expects it will get down to by the end of next year.

On inflation, the Governor points to pandemic-related price pressures the Board is prepared to look through, including petrol prices, new housing costs with subsidies rolling off and from global supply chains. Policy will react to the underlying CPI measure, and that is not seen reaching the midpoint of the 2-3% target band until the end of 2023 in the Bank's central scenario.

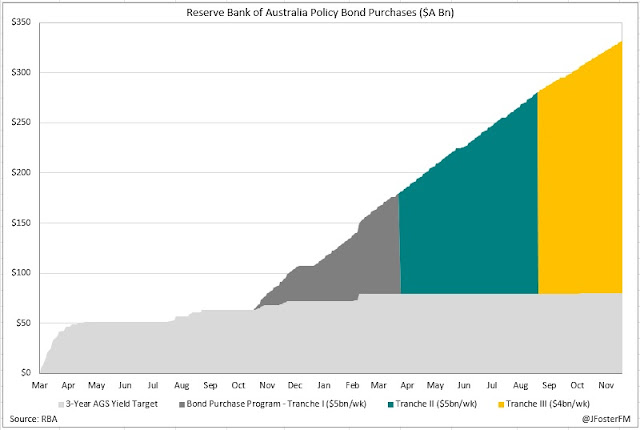

In line with the previous commitment given by the Board to review the QE program in February, little new insight was provided today. The one addition to the statement that might be of note was that the Governor stated the stock of purchases will reach $350bn by February. Central banks across the globe are in a transitional phase with their QE programs, with the focus turning away from new purchases to maintaining the stock accumulated throughout the pandemic as a means of providing ongoing accommodation.

This is worth pointing out given that the actions of other central banks are noted by the Governor as one of the Board's considerations when it reviews QE in February. The Fed is expected to soon accelerate its taper process; net purchases under the ECB's PEPP are guided to conclude in March and the BoE is close to reaching its targeted level of purchases. The RBA already commenced tapering in September and will also factor into its February review a new set of economic forecasts and overall functioning in the domestic bond market.

Overall, the RBA retains a significantly more dovish outlook on policy compared to markets where futures pricing has around 75bps of hikes discounted in 2022. Necessary pre-conditions to the hiking cycle are the RBA delivering sustainable 2-3% inflation, backed by a tight labour market and "materially higher" wages growth, all of which are some way off yet. However, the chances of a February conclusion to the QE program appear to be rising.