The Mid-Year Economic and Fiscal Outlook (MYEFO) update to the 2021/22 Federal Budget was presented by the Australian Government today. After coming through the recent Delta lockdowns, the Australian economy is recovering sharply, with the Budget deficit for 2021/22 forecast to narrow by $7.4bn and by $2.3bn over the next 4 years. Much of the increase in forecast Government revenue is offset by new policy spending.

MYEFO 2021/22 | Budget Profile

On Budget night back in May, the deficit for 2021/22 was forecast to come in at $106.6bn (5% of GDP). Despite the significant setback to the economy from the Delta lockdowns with real GDP contracting by 1.9% in the September quarter, the deficit is now forecast to narrow by $7.4bn to $99.2bn (4.5% of GDP). The deficit is then projected to reduce over the out years to 2.3% of GDP by 2024/25. Compared to the May Budget, this leaves the nation's finances modestly better off, by $2.3bn, over the forward estimates.

The profile for net debt has improved relative to May. Previously, net debt was projected to rise from 34.2% of GDP in 2021/22 to 40.9% in 2024/25. This has been revised to 30.6% of GDP in 2021/22, while the peak is now lower at 37.4% of GDP in 2024/25. A lower borrowing requirement due to a narrower deficit and valuation effects from higher bond yields are the driving factors.

MYEFO 2021/22 | Overview

Since May, Government receipts (revenue) have been revised up by $50.1bn for 2021/22 and by $109.1bn through to 2024/25. Driving these upgrades are a stronger-than-expected recovery in the labour market and high commodity and asset prices, boosting the tax in-take. Receipts as a share of GDP now track an upgraded profile relative to that forecast in May, reaching 24.2% by 2024/25.

Government payments are now seen coming in $42.7bn higher for 2021/22 than in May, rising to $106.8bn over the 4 years. The key factors in this are increased spending associated with the pandemic during the Delta lockdowns and spending on essential services, notably the NDIS, aged care and childcare. As a result, payments as a share of GDP have lifted since May, though they remain on a downward trajectory from 28.7% in 2021/22 to 26.5% by 2024/25.

As highlighted in the previous section, since Budget night, the projected deficit in 2021/22 has narrowed by $7.4bn. The Delta outbreaks led to the Government ramping up income support for households and businesses, and this drove a $30.7bn increase in policy spending this financial year. The net cost of new policy through to 2024/25 is $44.8bn. Coming ahead of next year's federal election, this figure has $16bn of policy spending 'not yet announced' baked into it.

The cost of new policy is more than offset by stronger economic conditions than previously anticipated, generating a projected windfall. In 2021/22, this boosts the Budget by $38.7bn and by $47.1bn over the forward estimates.

MYEFO 2021/22 | Forecasts

In the near term, the growth outlook for 2021/22 has been downgraded from 4.25% to 3.75% after the trajectory of Australia's expansion was disrupted by the Delta lockdowns. However, growth is still well above trend this financial year and the forecast for 2022/23 has been increased to 3.5%.

A strong pace of growth and negative net overseas migration due to the border restrictions has seen the unemployment rate forecast falling from 5% to 4.5% this financial year. The labour market is projected to gradually tighten thereafter, with a low unemployment rate resulting in wages growth (3%) and inflation (2.5%) reaching the levels seen by the RBA as consistent with full employment in 2023/24.

Treasury retained the assumption that the iron ore price will retrace to US$55/t (by Q2 2022). From their current elevated level, this sees the terms of trade holding flat in 2021/22 ahead of a correction in 2022/23 (-18%). This weighs on the outlook for nominal GDP growth over the out years.

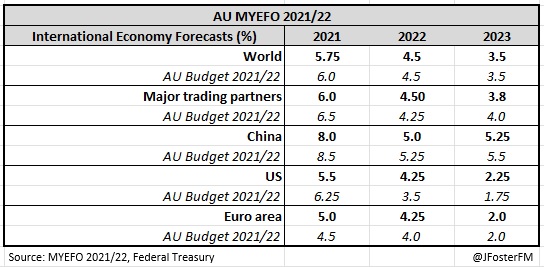

Global activity provides a supportive outlook for the Australian economy. The recovery from the pandemic is well underway in many economies offshore and robust rates of growth are seen over the next couple of years. Delta was a headwind in 2021, but growth has been upgraded in 2022 for Australia's major trading partners to 4.5%.

MYEFO 2021/22 | Summary

The resilience of the Australian economy is highlighted by the narrower deficit in 2021/22 despite the significant contraction to GDP seen in the September quarter. Higher Government revenue generated by the stronger-than-anticipated recovery will continue to support spending over the next 4 years, with a further $44.8bn of new measures in the pipeline.