Australian wages growth returned to its pre-pandemic pace at a little above 2%Y/Y in the September quarter as the proportion of jobs receiving wage increases was more in line with historical patterns. However, the pace of wages growth remains slow and labour shortages look to be driving up wages in only a small number of industries, mainly construction and professional services.

- The headline WPI (total hourly rates of pay ex-bonuses) matched expectations in Q3 coming in at 0.6%q/q and 2.2% over the year. This was a rise in the pace from Q2 at 0.4%q/q and 1.7%Y/Y.

- Private sector WPI increased by 0.6% in the quarter to be up 2.4% through the year; its fastest since Q1 2019.

- Public sector WPI was stronger in Q3 rising by 0.5%, lifting annual growth off a record low to 1.7%.

Wage Price Index — Q3 | The details

In the September quarter, wage-setting patterns appeared to be returning towards pre-pandemic norms. ABS analysis finds that the proportion of jobs recording a pay rise in the quarter was in the historical range for this time of year (35-40%). The Covid shock had seen that figure fall to just 20% a year ago, reflecting the implementation of wage cuts and freezes as firms focused on making it to the other side of the lockdowns. In the quarters since, these measures have gradually been unwound leading to a recovery in wages growth. This remained a factor in Q3 as the low point for wages growth last year fell out of the annual calculation. As a result annual WPI growth lifted from 1.7% to 2.2%, to be around its pre-pandemic pace.

The main driver of wages growth in Q3 came from individual agreements, which is a reflection of the pockets of the labour market where shortages are driving upward pressure on wages. The contribution to wages growth from enterprise agreements was the strongest it has been for two years and is reflecting the end of wage freezes. The lift in the national minimum wage added only modestly to wages growth. This reflects the earlier decision by the Fair Work Commission to stagger the implementation of the increase in the industries hit hardest by the pandemic.

Rather than turning to wage increases in an attempt to retain or attract new staff, many firms have been using other incentives such as sign-on or retention bonuses or offering more attractive conditions to workers. The increase in the WPI inclusive of bonuses measure was 0.8% in Q3, only a little stronger than the headline increase (0.6%).

At the industry level, the fastest pace of wages growth is being recorded in business services. This is being driven by strong demand for labour in professional services, with that industry recording the fastest rise in wages in the quarter (1.3%) and over the year (3.4%). Off the back of this, wages in admin and support have also rebounded to their pre-pandemic pace. Wages growth in rental, hiring and real estate services look to be rebounding on the strength of the residential property market.

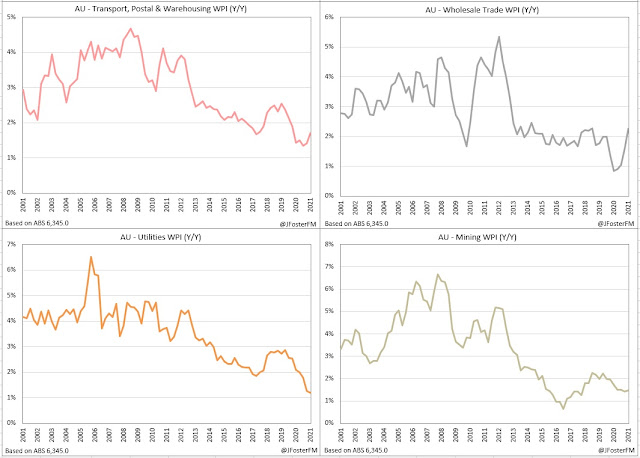

In the goods-related sector, the main development is the acceleration seen in wages growth in the construction industry. Very strong demand for construction from stimulus measures and rising housing prices is creating competition for labour and this has pushed up wages growth in construction to a 7-year high at 2.6%Y/Y, though that is a modest pace in a historical context. Wages growth in manufacturing, retail and wholesale trade has recovered to around their pre-pandemic rates.

In the household services sector the effects of the pandemic are continuing to play out. Wages growth in health care, education and training and arts and recreation is yet to retrace their pandemic induced slowdown. This is to be expected given the widespread lockdowns that were in place in large parts of the nation in Q3 and the public sector wage policies that would be applying to health care and education industries in particular. On aggregate, wages growth in accommodation and food services is now a little above its pace in the years prior to the pandemic. This may be reflecting shortages for hospitality workers in the states that were not affected by lockdowns in Q3.

Wage Price Index — Q3 | Insights

There are signs in today's report that wages growth in Australia is moving back towards pre-pandemic norms, but the pace remains low and is well short of what the RBA assesses would be consistent with an economy generating sustainable 2-3% inflation. There remains an absence of broad-based pressure on wages, though labour shortages look to be having a clear effect on wages growth in professional services and in construction. The "inertia" to which RBA Governor Philip Lowe referred to in yesterday's speech is likely to hold back wages growth stemming from enterprise agreements and changes in award rates. The area to watch is wages growth coming from individual agreements that can be more responsive to the labour market recovery.