A busy week of RBA communications led to a sizeable upgrade in Australia's economic outlook, but this has not shifted the Board's tone on policy settings. At its May meeting, the RBA Board left all policy settings as they were and maintained its forward guidance stating the conditions to prompt rate hikes were not expected "until 2024 at the earliest" (see here). But there are more pressing policy deliberations upcoming around the maturity of the 3-year yield target and bond purchase program, and Governor Philip Lowe outlined in his decision statement that announcements on the way forward with both tools will be made at the July meeting. The May Statement on Monetary Policy recalibrated the Bank's forecasts to the stronger-than-expected pace of the recovery that has ensued from the strong health and economic response to the pandemic. As a result, GDP growth in 2021 was revised up to 4.75% from 3.5% previously, reflecting stronger growth in household consumption, business investment and residential construction. For 2022, the pace of growth in the economy moderates but remains well above trend at 3.5% in an unchanged forecast.

The much stronger growth forecast this year has largely attenuated concerns around the impact of the recent withdrawal of the JobKeeper wage subsidy on the labour market. Forecast unemployment in 2021 was lowered significantly to 5% from 6%, though improvement thereafter is much more gradual declining to 4.5% by mid-2023. But the key is the implications for wages growth and inflation. The RBA has repeatedly stated that full employment is needed to generate wages growth of around 3% so that inflation holds sustainably within its 2-3% target band. On these new forecasts, by mid-2023 wages growth is at 2.25% (2% previously) and underlying inflation at 2.0% (1.75% previously). Thus with the economy expected to fall short of meeting the RBA's full employment and inflation objectives, it remains my view that at the July meeting the Board will extend the maturity of the 3-year yield target policy from the April 2024 bond to the November 2024 bond, as well as announcing a further $100bn of bond purchases.

Domestic data out this week remained consistent with the strong tape of releases seen throughout the recovery to date. Strength in conditions in the residential property market were again highlighted as housing finance commitments regained momentum rising by 5.5% in March after the upswing paused temporarily in the month prior (see here). Commitments to investors led in March and in Q1 overall, but activity in the owner-occupier segment remains very strong. With stimulatory policy driving demand, house prices continue to advance with CoreLogic's monthly index posting a 1.8% in April coming off the back of a record increase in March of 2.8%. Notable again was the outperformance of detached houses where price gains to date in 2021 are running at 8.6%, which is twice the pace of that for units (4.3%) reflecting a pandemic-related shift away from higher-density housing. Similarly, while the higher-density segment drove a much stronger-than-expected rise of 17.4% in total dwelling approvals in March, detached house approvals over Q1 (10.7%) were significantly stronger than for units (3.2%) with policy stimulus from the HomeBuilder scheme and state government subsidies a key factor (see here). Surprising to the downside this week and coming amid the surge in global commodity prices, the nation's trade surplus pulled back to $5.6bn in March from $7.6bn, defying expectations for it to widen to $8.2bn (see here). Driving the result was a 4.3% rise in imports in the month, indicative of the strength of domestic demand that is leading the recovery.

— — —

Switching to offshore where it was the large downside miss on expectations in the latest US employment data that was the main development of the week. In a result completely counter to the reports of strong labour demand — including in this week's ISM surveys — employment on non-farm payrolls came in at 266k in April missing the consensus estimate of 1 million (see chart, below). Hopes were that the very strong growth in payrolls seen in March would carry on, but some of the gloss was taken off that report as revisions cut the 916k rise in employment to 770k. Meanwhile, headline unemployment lifted to 6.1% from 6.0% whereas it was forecast to fall to 5.8%. Adding to the confusion was that labour supply lifted in the month, with participation edging up to 61.7%, and underemployment declined further to 10.4%. While the weakness in April's report may prove temporary, given the Federal Reserve's patient stance on policy, expectations for a potential near-term tapering of asset purchases have most certainly taken a hit. Despite inflation expectations moving higher, a flatter US yield curve through the week suggests markets may be closer to coming to terms with the Fed's reaction function.

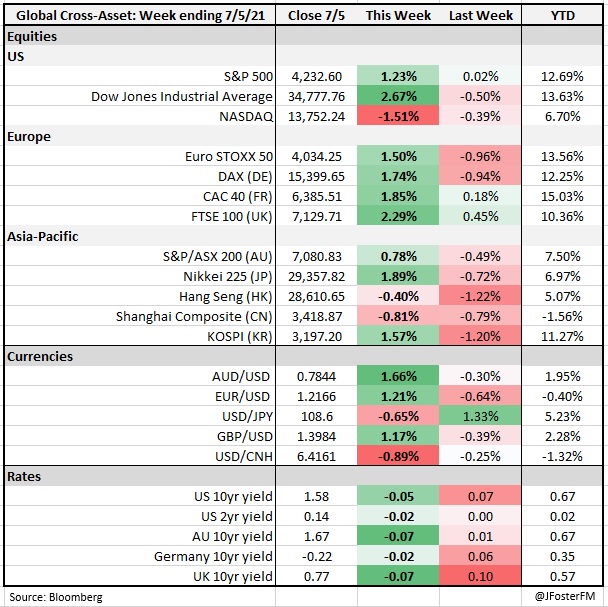

Chart of the week

Over in the UK, the Bank of England left all monetary policy settings unchanged at this week's meeting amid a much-improved outlook for the economy due to the fast vaccine rollout curbing transmissions and generating optimism for a wider reopening in the summer. As outlined in the Bank's May Monetary Policy Report, the return to national lockdown at the turn of the year is thought to have led to the economic recovery backsliding in the order of 1.5% over Q1, leaving GDP around 9% below its pre-pandemic level. But with restrictions easing a stronger rebound is now expected. Growth is forecast to rise by around 4.25% in the current quarter and with the momentum sustained, GDP returns to pre-pandemic levels by the end of this year, occurring some 3 months earlier than previously expected. Relatedly, and with the cover of the extension in the government's furlough scheme through September, unemployment is now seen peaking much lower around the middle of the year at just under 5.5% compared with 7.75% forecast back in February. On inflation, the Bank's central scenario is that near-term inflation pressures will prove transitory with CPI peaking at around 2.5%, mainly reflecting a rebound in energy prices, before easing back towards the 2% target in 2022 and 2023.

At this stage, the policy implications appear limited. While an announcement was made that the weekly pace of asset purchases in the current program would slow from £4.4bn to £3.4bn, Governor Andrew Bailey emphasised in the post-meeting press conference that this should not be seen as tapering, as neither the stock of purchases (£150bn) or its specified end date (end 2021) had changed. In any case, 10-year Gilt yields ended the week much lower at 0.77%. At the higher pace, purchases had been frontloaded to quell market volatility arising from an earlier upsurge in virus infections and were on track to conclude ahead of its end date. The Bank's Monetary Policy Committee voted for this week's decisions in an 8-1 analysis, with the one dissenting voice, Chief Economist Andy Haldane, arguing the improved economic outlook justified an earlier finish to asset purchases in August, lowering the targeted stock of the program by £50bn. In Europe, there was a notable upside result on retail sales in March, rising by 2.7% against expectations of 1.6%, while sales in February were revised higher to 4.2% from 3.0%. This outturn helped to reaffirm optimism building in markets for the strength of the rebound in Europe likely to be coming over the summer as restrictions are eased more widely.