Momentum in the Australian economy slowed materially in 2023. With the recovery from the pandemic having run its course, household consumption - the largest component of the economy - was left increasingly exposed to cost-of-living pressures and higher interest rates as the year progressed. Real GDP growth was 0.2% in the December quarter, slowing from 2.1% to 1.5% through the year. The slowdown intensified in the back half of the year; GDP increased by 0.5% in the period - the softest half-year outturn excluding the Covid period since 2008 following the global financial crisis.

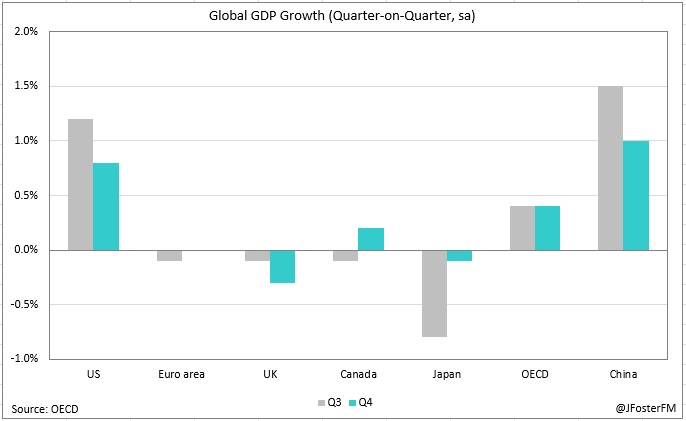

Similar trends were seen offshore. Although growth in the US economy remained strong, most other advanced economies slowed sharply in the second half of the year. In China, consumption growth eased with the pandemic recovery winding down.

In Australia, domestic demand (0.1%q/q, 2.3%Y/Y) has been bolstered by the public sector (0.4%q/q, 4.7%Y/Y). This has helped to offset weakening private demand (0%q/q, 1.3%Y/Y) as household consumption slowed to the point of stalling and dwelling investment contracted; however, business investment was resilient, contributing strongly to output growth.

The December quarter GDP outcomes were in line with RBA expectations. Notwithstanding this, the RBA's assertion of the economy operating in excess demand looks harder to sustain. Economic growth is now at a subdued pace (and -1%Y/Y in per capita terms); inflation slowed sharply into year-end; and the labour market - while still robust - has eased from cycle tights.

Declining inflation improved real income dynamics in the quarter, but households are continuing to feel the effects of pressures on their budgets. In 2023, mortgage interest payments and income tax accounted for more than a 21% share of disposable income.

Some relief is on the way via the upcoming stage 3 tax cuts, while the case for the RBA to ease restrictive monetary policy settings from its 4.35% cash rate will build if the incoming data continues to suggest that momentum in the economy is weak.

— — —

National Accounts — Q4 | Expenditure: GDP (E) 0.4%q/q, 1.6%Y/Y

Household consumption (0.1%q/q, 0.1%Y/Y) — The accumulation of pressures from the higher cost of living and RBA rate hikes effectively brought household consumption to a standstill in the December quarter. Consumption went backwards in categories including new vehicles (-3.6%), hotels and cafes (-2.8%) and clothing and footwear (-2.5%), reflective of a broad-based rotation away from discretionary-related consumption over the past year (-1.6%) to essential goods and services (1.2%).

The news around real incomes saw some welcome developments. Real disposable income lifted by 1.5% in the quarter - its best result since Q3 2021 - turning positive in annual terms (0.3%) for the first time since mid-2022. This came as nominal income increased by 2.3%q/q - underpinned by rising wages growth in a still-robust labour market (1.4%), social assistance payments (5.9%) and interest income (6.7%) - and inflation (on the household consumption deflator) eased to 0.8%q/q.

As a result, the improvements to real income dynamics supported a rise in the household saving ratio to 3.2%, lifting from a 15-year low in Q3 (1.9%). Although this remains well below pre-pandemic levels of around 5-6%, households still, on aggregate, retain a substantial stock of excess savings accumulated during the Covid period.

Dwelling investment (-3.8%q/q, -3.1%Y/Y) — Residential construction activity slumped into year-end contracting by 3.8% in Q4 to be down 3.1% through the year. The effects of higher interest rates, weak sentiment and supply and labour constraints - legacies of the pandemic - are all weighing on the sector. Declines in Q4 were sizeable in both new home building (-3.5%) and alterations (4.2%), the latter contracting for the 9th time in the past 10 quarters, unwinding from its stimulus-driven peaks seen during the pandemic.

Business investment (0.7%q/q, 8.3%Y/Y) — A frontloading of business investment into the first half of the year (6.7%) ahead of the withdrawal of tax incentives led to an inevitable easing of momentum in the second half (1.5%). Overall, business investment lifted sharply through the past year (8.3%), contributing 1ppt to the 1.5% increase in real GDP over the period. In the most recent quarter, business investment lifted 0.7%. The major driver was non-dwelling construction (2.5%q/q) - up a robust 9.3%Y/Y - as machinery and equipment investment saw a pullback (-1.3%q/q).

Public demand (0.4%q/q, 4.7%Y/Y) — Despite moderating in Q4 (0.4%), public demand was still up by a solid 4.7% through the year. This has delivered a key offset to the economy alongside the slowdown in private demand. In Q4, public expenditure increased by 0.6%, led by assistance payments to households and the staging of the Aboriginal and Torres Strait Islander Voice Referendum held in October. Underlying investment was surprisingly soft in the quarter (-0.2%) but has risen significantly over the past year (13.7%) as progress on the substantial pipeline of public infrastructure projects has ramped up.

Inventories (-0.3ppt in Q4, -0.9ppt yr) — Subtracted from growth in Q4 (-0.3ppt) and over the past year (-0.9ppt). Inventories declined in the December quarter as earlier disruptions that affected production and transportation in the resources sector cleared, amid strong demand for Australia's bulk commodities offshore. This was moderated by a sizeable increase in public authorities inventories.

Net exports (0.6ppt in Q4, 0.3ppt yr) — Contributed 0.6ppt to GDP in Q4 but added only modestly to growth over the past year (0.3ppt). Export volumes declined by 0.3% in the quarter, rounding out a soft second half in 2023 (-0.5%); goods trade (-2.2%) was weighed by disruptions to resources shipments and the recovery in the services sector (mainly tourism and education) moderated (8.3%). Overall, exports are still 3.2% short of recovering to pre-Covid levels. By contrast, imports remain substantially above pre-Covid levels (+6.2%); however, a sharp decline of 3.4% in Q4 reflects the weakness seen in domestic demand into year-end. Notable contractions came in consumption (-5.4%) and capital goods (-3.4%) as well as in travel services (-9%).

— — —

National Accounts — Q4 | Incomes: GDP (I) 0.2%q/q, 1.4%Y/Y

A 2.3% rise in the terms of trade - coming after declines of 7% in Q2 and 2.1% in Q3 - supported Australian national income in the final quarter of the year. This was driven by a 3.1% acceleration in export prices as commodity prices increased, outpacing a 0.8% rise in import prices alongside a weaker Australian dollar. Notwithstanding this, the terms of trade fell by 3.9% through the year to be down almost 12% from its record high in mid-2022.

The increase in the terms of trade underpinned rising nominal GDP, up 1.4%q/q to 4.4%Y/Y. A year earlier, nominal GDP had expanded at 12.1%Y/Y pace, with declines in commodity prices driving the slowdown.

Higher commodity prices flowed through to mining company profits, reflected in non-financial corporations operating surplus rising by 2.9%, partially rebounding from material declines in Q2 (-7.5%) and Q3 (-3.9%). Financial corporations operating surplus posted a 1.6%q/q rise to be up 6.3% through the year, with rising interest rates boosting net interest margins for banks. By contrast, margin pressures are weighing on small company and farming profits, with gross mixed income falling 4.1% q/q and 8.6%Y/Y.

Growth in wage incomes moderated to 1.4% in Q4 (8.4%Y/Y) after receiving a large boost in the previous quarter (2.8%) from increases to the minmium wage and award rates. In Q4, wages were supported by mandated increases that flowed through to workers in the aged care sector and by hiring associated with the Voice Referendum.

Due to hours worked in the economy falling over the past couple of quarters (-0.7% in Q3 and -0.3% in Q4), growth in hourly earnings (non-farm wages) has picked up to be running at a 6%Y/Y pace. But this has not translated to an associated rise in unit labour costs; this is because measured productivity outcomes increased in Q3 (1.5%) and Q4 (0.5%), the result of economic growth rising as hours worked declined.

— — —

National Accounts — Q4 | Production: GDP (P) 0.1%q/q, 1.6%Y/Y

The GDP production estimate was 0.1% in the December quarter, easing from 1.9% to 1.6% at an annual pace. Gross Value Added to the economy rose at the same pace for goods-related (0.3%) as services-based industries (0.3%) in the quarter. Public administration (1%) was a notable contributor to growth, driven by activity associated with the Voice Referendum.

In the goods-related sector, goods production (0.5%) more than offset weakness in goods distribution (-0.2%). Goods production saw a rise on the back of increased output in the mining industry (1%) and in utilities (0.9%) as warm weather increased demand for electricity. The fall in goods distribution reflected declines from wholesalers (-0.6%) - associated with a reduction in grain exports - and transport (-0.3%) as demand for postal services eased and imports weakened.

Turning to the services sectors, household services stalled (0%) as consumption rotated away from discretionary-related areas to essential services. Accordingly, weakening demand led to declines in accommodation and food services (-3.2%) and in arts and recreation (-0.8%). This contrasts with gains across health (0.5%) and education services (0.4%). Business services advanced 0.5% overall in Q4. Professional services (1.2%) led the way on increased demand for engineering services.