Australia's March quarter national accounts are scheduled for release at 11:30am (AEST) today. A strong rebound following reopenings from the Delta lockdowns put the economic expansion back on track in the December quarter and output is expected to have increased further in the March quarter. The median estimate is for real GDP to expand by 0.7% in Q1, which would be a resilient outcome amid the headwinds from the Omicron wave, the east coast floods and rising inflation pressures.

The spread of the Omicron variant led to virus caseloads surging early in 2022. High levels of vaccination prevented the authorities from implementing the lockdowns and associated restrictions seen in earlier waves of the pandemic; however, isolation requirements and precautionary behaviour more generally weighed on economic activity. The severe wet weather events in New South Wales and Queensland, including major flooding, were another headwind. Accordingly, mobility indicators showed a slower recovery than in 2021 from their seasonal fall over the Christmas and new year period.

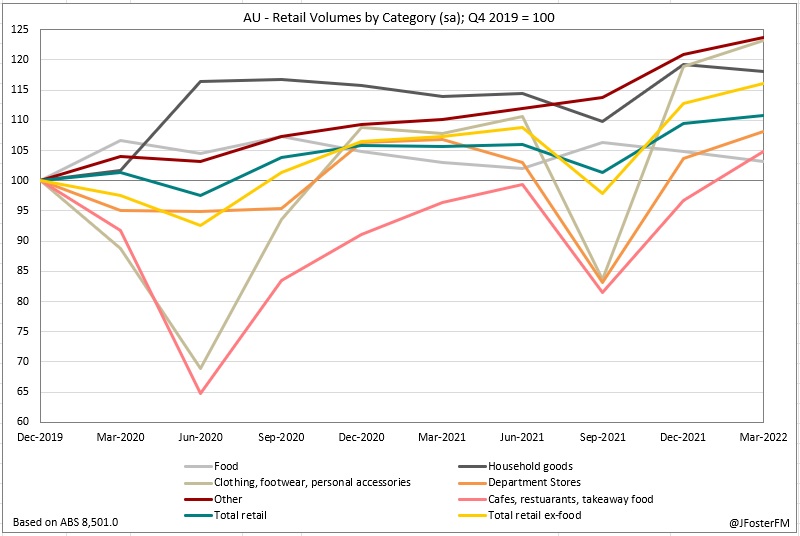

Household spending proved resilient over the March quarter to sharply rising retail prices and weakening sentiment. Key factors supporting spending were the high level of accumulated savings held by households and rising labour incomes generated by a tightening labour market that has seen the unemployment rate falling below 4% for the first time since the 1970s.

Retail sales volumes rose at a solid pace in the quarter (1.2%), driven by strong growth in the discretionary categories (2.9%). The ongoing reopening of states and the easing of border restrictions had supported services-related spending, with dining out consumption surging (8.3%), while strong rises in clothing and footwear (3.6%) and department stores (4.3%) indicated goods-related demand remained robust.

National housing price gains moderated over the quarter to a little above 2% from around 4% in the December quarter. This was driven by a cooling of gains in the Sydney and Melbourne markets, though prices were still rising at a strong pace in some smaller capital city markets, including Brisbane and Adelaide. Residential construction ran up against further delays from wet weather and Omicron in addition to trade and materials shortages.

Business investment softened in the quarter and was yet to regain the momentum it had generated ahead of the Delta lockdowns. Net exports subtracted heavily from activity in the quarter. Resources exports were affected by adverse weather conditions, though export earnings accelerated as key commodity prices surged following the Ukraine war. Import volumes lifted sharply despite higher prices, consistent with the strength in domestic demand. The easing of travel restrictions during the quarter enabled services trade to commence its recovery.

As it stands | National Accounts — GDP

The reopenings of states from lockdowns during the Delta wave led to the economic expansion regaining momentum, with real GDP rising by 3.4% in the December quarter. This lifted Australian GDP to 3.4% above its pre-pandemic level at the end of 2019.

In the global economy, activity lifted at a solid pace in the final quarter of 2021 despite the emergence of the Omicron variant. Rising household consumption was driving the recovery of economies supported by accommodative monetary policy, accumulated savings and tightening labour markets. Goods consumption remained substantially more elevated than services consumption and was adding to inflation pressures given ongoing constraints in global supply chains. In the quarter, GDP growth advanced by 1.2% in the OECD as output lifted pace in the US (1.7%), UK (1.3%) and Japan (1.1%). Growth in the euro area slowed (0.3%) after eased restrictions had boosted activity in Q3. Meanwhile, in China, output gained pace in Q4 (1.5%) after slowing in the prior quarter.

December quarter GDP growth in Australia was driven by a resurgence in household consumption (6.3%) as New South Wales, Victoria and the ACT reopened from extended lockdowns. Services consumption rebounded by 6.3% as entertainment venues, restaurants and licensed premises reopened and some domestic travel resumed. Goods consumption also lifted by 6.3% as non-essential retailers resumed in-store trading. Although real disposable income fell in the quarter, households had built up savings during the lockdowns, which were partially drawn on to fund spending during the reopening phase. The household saving ratio fell from 19.8% to 13.6% as a result but was still at a high level going into 2022.

Private investment was weak during the quarter falling by 1.2%. Residential construction activity (-2.2%) was held back by materials and labour shortages, delaying progress in completing the large pipeline of work. Business investment softened further (-0.3%) following Q3's contraction, with the lockdowns and supply chain pressures pausing the upswing seen during the first half of the year.

Public demand, a strong support to the economy over the Covid period, weakened in Q4 (-0.4%) as investment slowed. Inventories rebounded to contribute 0.9ppt to quarterly growth; the restocking needed to meet the post-lockdown recovery in demand. Net exports subtracted 0.2ppt from Q4 GDP, with exports (-1.5%) held back by constraints in the resources sector and imports falling (-0.9%) in response to supply chain pressures.

Key dynamics in Q1 | National Accounts — GDP

Household consumption — Supported by a further easing of restrictions, accumulated savings and a tightening labour market, household consumption lifted at a solid pace in the quarter. Households spending was resilient amid Omicron, floods and rising inflation, with discretionary demand robust despite weakening sentiment.

Dwelling investment — Disruptions in the residential construction sector intensified in Q1 as the wet weather on the east coast and Omicron added to delays stemming from capacity constraints. Private sector residential work contracted by 1% in the quarter, with new home building down by 1.6%q/q. A partial rebound in the alterations segment (2.1%) provided some offset.

Business investment — Private sector capex softened by 0.3% in the quarter, reflecting weakness in non-mining equipment investment (-0.1%) and capacity constraints holding back progress in the construction of new buildings and structures (-1.7%).

Public demand — Rebounded from a weak Q4 to rise by 2.5% in Q1. Both expenditure (2.7%) and investment (1.6%) advanced, bolstering the economy amid the disruptions to activity in the quarter.

Inventories — An easing of global supply chain pressures supported a rebuilding of inventories back to pre-Covid levels. May add up to 1ppt to quarterly GDP.

Net exports — Set to subtract 1.7ppts from Q1 GDP. Export volumes contracted by 0.9%q/q as both resource and rural goods production was affected by the severe wet weather events. Imports regained momentum accelerating by 8.1%q/q. Input shortages eased, boosting vehicle, electrical goods and machinery imports.