Australian private sector capital expenditure softened against expectations in the March quarter, easing back from a reopening driven boost in the final quarter of 2021. Forward-looking investment plans for 2022/23 were upgraded sharply to $131bn, showing resilience amid an uncertain outlook.

CapEx — Q1 | By the numbers

- Private sector capex declined by 0.3% in the March quarter to $33.6bn (4.5%Y/Y), disappointing expectations for a 1.3% rise, though the prior quarter's increase was revised higher, from 1.1% to 2.3%.

- Equipment, plant and machinery capex posted a 1.2%q/q rise to $16.2bn (1.8%) on the back of strength in the mining sector.

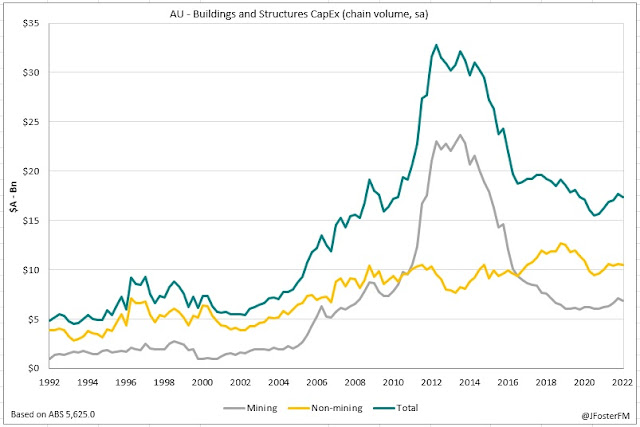

- Buildings and structures capex declined by 1.7%q/q to come in at $17.3bn, up 7.1% through the year.

- Firms' 6th estimate of capex plans in 2021/22 was upgraded by 1.4% to $142.8bn, in line with expectations and pointing to a year-to-year rise of 15.5%.

- The 2nd estimate of year-ahead plans for 2022/23 was robust, upgraded by 11.8% to $131bn (vs my estimate of $125bn), its highest since 2014/15.

CapEx — Q1 | The details

Capex softened in the March quarter (-0.3%) as the reopening rebound from the previous quarter (2.3%) was cycled. This eased capex to $33.6bn, up 2.9% on its subdued pre-Covid level.

Total equipment investment expanded by 1.2% in the quarter, though this came entirely from the mining sector (7.7%) as equipment spending in the non-mining sector was broadly unchanged (-0.1%). Equipment investment has expanded at a strong pace over the Covid period, now 6.3% above its pre-pandemic level, supported by accommodative financing conditions and the tax incentives introduced by the federal government, with firms needing to invest to meet the increase in demand generated by the economic recovery.

Q1's weakness in non-mining equipment investment was centred in household services (-9.8%), coming after the reopening boost in Q4 last year (6.5%). This reversal played out in the hospitality (-12.3%) and health care industries (-8.8%).

Investment in buildings and structures was lower in the quarter (-1.7%), likely held back by the capacity constraints highlighted in yesterday's construction activity data (see here). Declines were seen in both the mining (-3.3%) and non-mining sectors (-0.6%). The recovery in investment in buildings and structures in the non-mining sector has been slow, still more than 8% down on its pre-Covid level. This period of underinvestment will need to be corrected, though rising construction costs due to materials and labour shortages is likely to restrict the pace at which this occurs. Spending on building and structures in the mining sector remains around its level from recent years, despite surging commodity prices.

Turning to the investment plans component in the report, firms lifted their 6th estimate of plans for 2021/22 from $141bn to $143bn, a broadly expected outcome. This puts capex on track to rise by 15.5% compared to 2020/21. On current estimates, capex will lift by around 15% in the non-mining sector and by 17% in the mining sector on a year-to-year basis.

Firms were also surveyed by the ABS (between April and May) for their 2nd estimate of investment plans for 2022/23. Encouragingly, despite the uncertainty around global growth prospects from rising interest rates, the war in Ukraine and China's lockdowns, the 2nd estimate was a strong result, rising to $131bn from $117bn in the first estimate, an upgrade of 11.8% and also up 15% from the equivalent estimate in 2021/22. At $131bn, this was the highest 2nd estimate of year-ahead investment plans since 2014/15.

Investment plans in the non-mining sector for 2022/23 were lifted to $89bn (+13.3% vs est 1), with plans for both equipment and buildings and structures investment increased by around 13% (vs est 1). Mining investment plans were upgraded by 8.7% on estimate 1 to around $42bn. This included upgrades to both equipment (8%) and buildings and structures (9%) plans.

CapEx — Q1 | Insights

A soft result for quarterly capex, particularly in non-mining sector equipment investment (-0.1%). However, the implications look broadly neutral for Q1 GDP. The positive was the strong upgrade to 2022/23 investment plans. The key is whether this can hold up as global and domestic growth slows and with inflation still high, in part due to factors that have already been a headwind for business investment from product and labour shortages.