Australian housing finance commitments rose for the third month in succession lifting by a stronger-than-expected 5.4% (vs 1.1%) in October ($26.7bn). Commitments are now 17.5% above the cycle low in February ($22.8bn) as supply-demand imbalances have led to an upturn in housing prices, despite further RBA rate increases through the year. CoreLogic has clocked this upturn at around a 10% rise in the median capital city house price since January.

October's 5.4% rise was the sharpest month-on-month lift in commitments since May. This gain came after the RBA held rates unchanged between July and October. It will be interesting to assess how the resumption of the tightening cycle in November may have impacted this momentum.

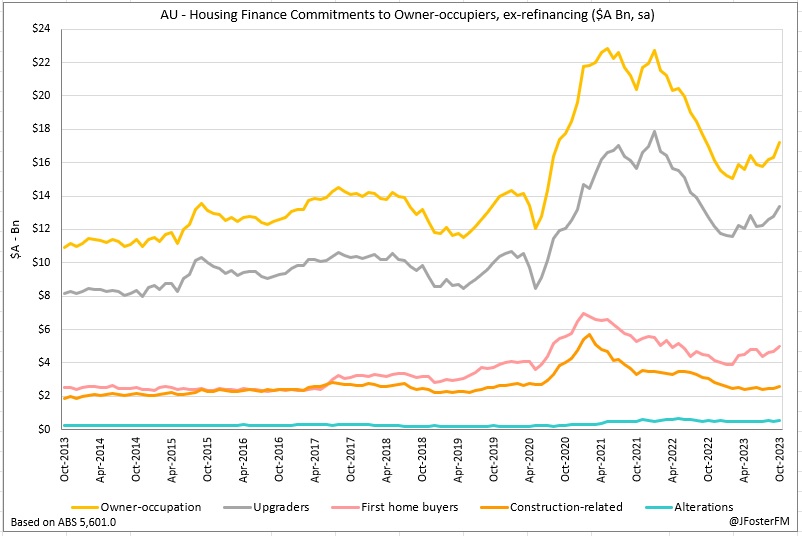

Commitments to the owner-occupier segment posted a 5.6% lift - its sharpest rise going back to November 2021. At $17.2bn, commitments to the segment are up 14.2% on their trough in February ($15.1bn). Of note this month, construction-related lending accelerated 6.3% to $2.6bn, a high to the start of the year. Commitments to upgraders increased by 4.6% to $13.4bn, a 14-month high. There was also participation from first home buyers, with the value of commitments up 6.2% ($5bn) and loan volumes rising by 5.1% (9.8k).

In the investor segment, new commitments lifted by 5% to touch a 16-month high at $9.5bn. These commitments have increased for 8 months on end to stand 23.9% above their cycle low ($7.7bn). Very low capital city vacancy rates, strong rent inflation and rising house prices have clearly been attractive fundamentals for many investors.

Refinancing fell by 7% ($17.4bn), declining sharply for the third month running. Over this period, the value of refinancing has fallen by 19.5% (-21.6% in the owner-occupier segment and -15.2% for investors). Refinancing activity is clearly moderating after rising very sharply through the past couple of years as many borrowers rolled off fixed-rate periods onto higher variable rates. The RBA pausing rate hikes may have accelerated the decline.